Education technology produced one of the largest deals of the past year when Coursera and Udemy agreed to combine in an all-stock transaction with an implied equity value of roughly $2.5 billion. That single announcement tells you a lot about edtech business valuation in 2026: capital is moving, buyers are paying real money for learning assets, and the gap between well-prepared businesses and everyone else has never been wider.

If you own an edtech company, the question is no longer whether buyers exist. They do, at every size band from six-figure course platforms to billion-dollar enterprise learning suites. The question is what your specific business is worth, which method a buyer will use to price it, and which numbers in your dashboard will move that price up or down.

This guide answers all three. We cover the valuation methods that apply at each stage (SDE, EBITDA, and revenue multiples), the 2026 benchmark data behind them, the subscription metrics and lifetime value math that drive multiples, and the real transactions that show what acquirers actually paid. We close with a practical preparation checklist and answers to the questions edtech founders ask us most.

The 2026 EdTech Market: Why Acquirers Are Paying Attention

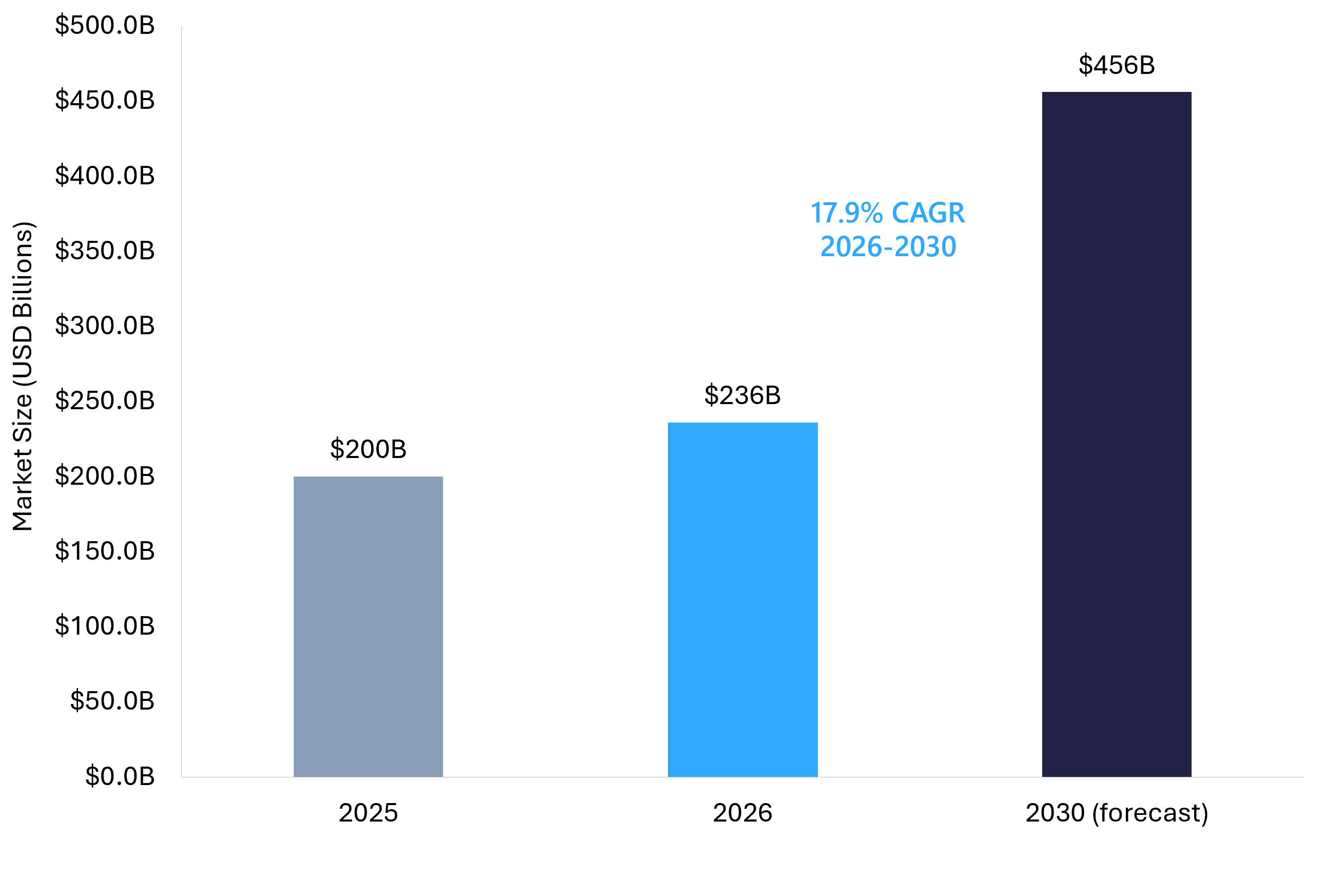

Valuations start with the market, and the edtech market is expanding at a pace few sectors can match. Global education technology spending is projected to reach $236.25 billion in 2026, up from $199.74 billion in 2025, and is forecast to hit $456.41 billion by 2030 at a 17.9% compound annual growth rate. Buyers underwrite future cash flows, so a sector compounding at nearly 18% a year gives every acquisition model a tailwind.

Demand is structural, not cyclical. Employers expect 39% of workers' core skills to change by 2030, and 59 out of every 100 workers will need reskilling or upskilling within that window. Corporations, school districts, and universities all have to buy learning technology to keep pace, which is exactly the kind of non-discretionary demand acquirers pay premiums for.

The capital side confirms the story. Global M&A overall rose 40% to $4.9 trillion in 2025, the second-highest deal value on record, with median strategic deal multiples ticking up to 11.6x EV/EBITDA and 80% of surveyed M&A executives expecting to sustain or increase activity in 2026. Within education specifically, Europe captured close to half of all global education VC value in the most recent cycle, a sign that buyer and investor interest in learning businesses is genuinely global rather than concentrated in one region. Demand from emerging markets adds another layer: Asia Pacific alone is expected to account for 28% of the global edtech market in 2026, with North America at 36%, so businesses with international distribution are positioned in front of the fastest-growing learner populations.

For sellers, the comparison with traditional education businesses is worth noting. A tutoring center or training company tied to physical locations is valued on local cash flow with limited scalability. An edtech business with the same revenue typically commands a higher multiple because software margins, recurring billing, and borderless distribution give a buyer more growth per dollar of acquisition price.

The takeaway for valuation: edtech businesses sell into a market growing at roughly 18% annually with structural reskilling demand behind it, and that growth is priced into the multiples buyers are willing to pay in 2026.

EdTech Business Valuation in 2026: The Three Methods That Matter

There is no single formula for valuing an edtech company. The method depends on the size, profitability, and growth profile of the business. Nearly every transaction we see uses one of three approaches, and choosing the right one is the first step toward an accurate number.

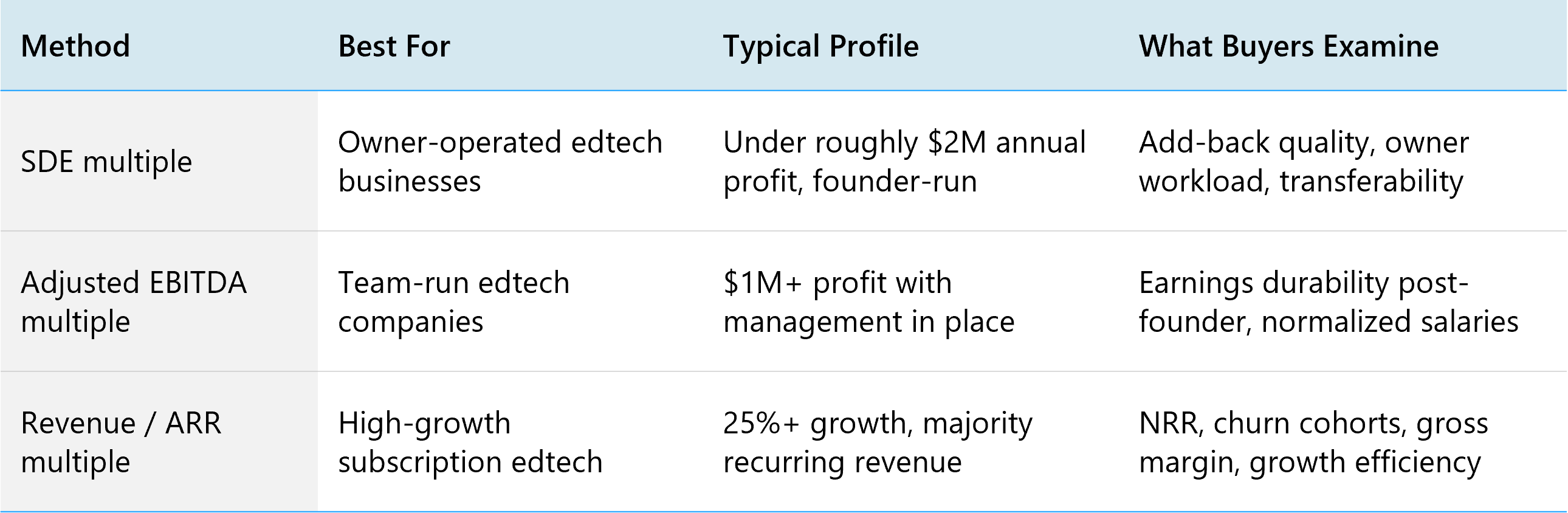

SDE: The Standard for Owner-Operated EdTech Businesses

Seller discretionary earnings (SDE) measures the total financial benefit a single owner-operator takes from the business: net profit plus the owner's salary, benefits, and any personal or one-time expenses run through the company. As FE International's guide to valuing a SaaS business explains, most businesses valued under $5 million are priced on a multiple of SDE, because a buyer at this level is usually replacing the owner and wants to know exactly what cash the business puts in one person's pocket.

SDE is the right lens for the course creator earning $300,000 a year, the niche learning app run by two founders, or the B2C study-tools site with a lean contractor team. If that describes your business, the work before a sale is documenting clean add-backs: your salary, one-off legal or development costs, and anything a new owner would not need to spend.

EBITDA: The Standard Once a Management Team Exists

Earnings before interest, taxes, depreciation, and amortization (EBITDA) takes over once a business runs on a team rather than an owner. Buyers at this level, typically $1 million and up in annual profit, want earnings that survive the founder's exit, so they price on adjusted EBITDA after normalizing for market-rate management salaries. The adjustment process matters: above-market founder compensation gets added back, but a missing CEO salary gets subtracted, and sophisticated buyers will model both.

The transition between the two methods is worth understanding because it changes the number. The same business can show $800,000 in SDE but only $650,000 in adjusted EBITDA once a market-rate general manager salary is deducted, and a buyer evaluating it as a managed asset will price the lower figure. Founders approaching the threshold sometimes benefit from making that hire before a sale: the headline earnings drop, but the business graduates into a larger buyer pool that pays higher multiples for team-run companies, and the trade is frequently positive.

Revenue and ARR Multiples: For High-Growth Subscription EdTech

Subscription edtech businesses growing quickly are often valued on revenue or annual recurring revenue (ARR) rather than earnings, because reinvestment suppresses current profit while recurring contracts make future revenue highly predictable. A buyer can see exactly what next year looks like from this year's retention cohort, which is why recurring revenue earns a fundamentally different multiple than one-time course sales. Revenue multiples apply where growth is strong (think 25% and up), gross margins are software-grade, and the majority of revenue renews automatically.

One practical note on deal channels. For edtech businesses valued under $1 million, a full investment-banking process is rarely the efficient path. FE International built its M&A Platform for exactly this segment: sellers get their business in front of a curated network of qualified buyers with verified metrics, and buyers browse vetted edtech and software listings with live data, all alongside the full advisory service FE International runs for larger transactions. The two work together rather than replacing each other. Owner-operated businesses priced on SDE move efficiently through the M&A Platform, while businesses above $1 million in value typically warrant the full advisory process with dedicated senior deal teams.

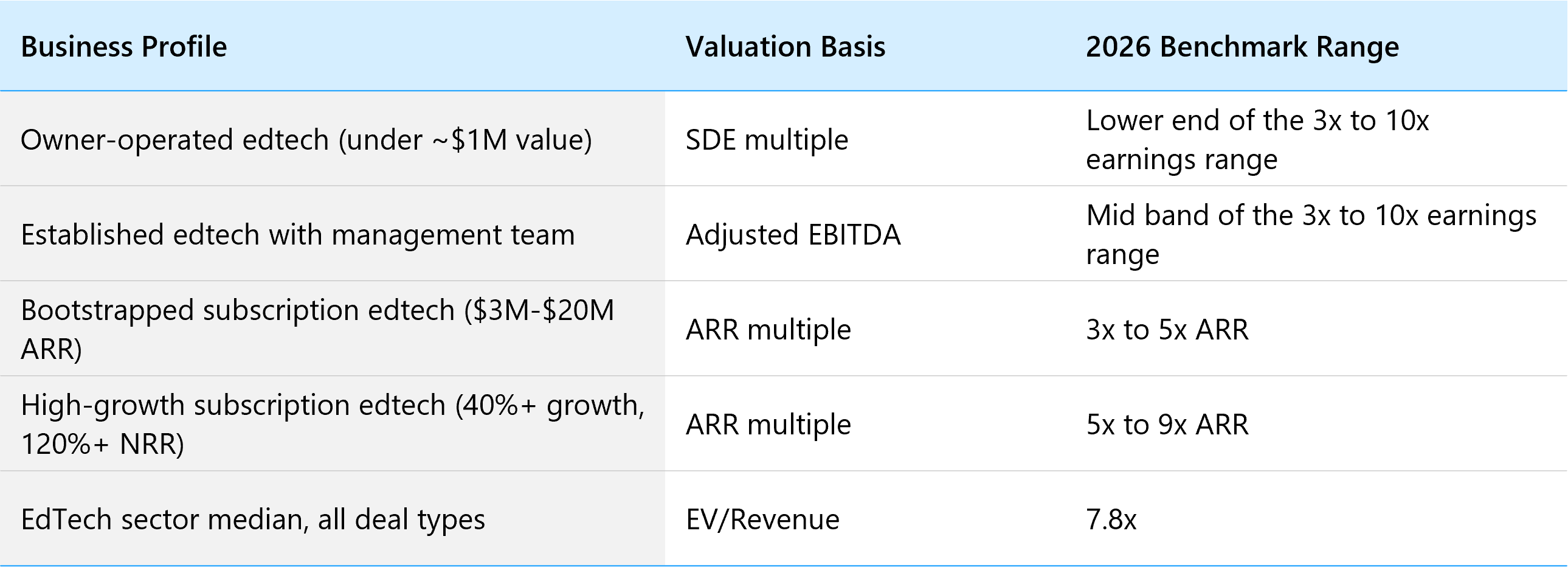

The takeaway for valuation: businesses under roughly $2 million in annual profit are usually priced on SDE, established companies with management teams on adjusted EBITDA, and high-growth subscription edtech on revenue or ARR multiples.

EdTech Valuation Multiples in 2026: The Benchmark Data

Multiples are where theory meets price, so let's get specific about what the 2026 data shows.

Across the sector as a whole, FE International's analysis of edtech M&A in 2026 places the median edtech multiple at 7.8x EV/Revenue across a dataset of 271 public, private, and M&A observations, with enterprise value to total funding at roughly 3.8x. That median masks wide dispersion by business model: workflow-embedded enterprise learning platforms sit at the top of the range, while direct-to-consumer products with weaker retention price well below it.

For the lower middle market, where most founder-owned edtech businesses trade, FE International's published benchmarks for internet and SaaS businesses run from roughly 3x to 10x annual earnings, with SaaS businesses under $20 million in revenue typically landing in the 5x to 10x band when metrics are strong. Bootstrapped subscription businesses with $3 million to $20 million in ARR generally trade at 3x to 5x ARR, while high-growth companies (40%+ growth with 120%+ net revenue retention) reach 5x to 9x ARR. Owner-operated edtech businesses priced on SDE typically transact at the lower end of the earnings range, which is still a meaningful outcome: a business producing $400,000 in SDE at 3.5x sells for $1.4 million.

At the top of the market, the public and unicorn data rounds out the picture. There are currently 14 edtech unicorns worldwide, collectively valued at $34.2 billion, with language-learning platform Preply the newest addition after reaching a $1.2 billion valuation in January 2026. The unicorn list has consolidated from its 2021 peak, and that consolidation is good news for anyone valuing a business today: pricing now reflects fundamentals rather than momentum, which makes 2026 benchmarks far more reliable for deal planning than anything from the zero-interest-rate era. Public-market activity tells a similar story of selective strength, with the Coursera and Udemy combination creating a listed learning company with more than $1.5 billion in pro forma annual revenue.

How does edtech compare with neighboring sectors? On a revenue basis it currently prices at a premium to much of the small-cap software market, and it has held value better than fintech, which has seen significant valuation compression since 2022, as covered in FE International's companion guide to cybersecurity business valuation. The premium reflects the structural reskilling demand discussed above and the recurring, contract-based revenue that the strongest edtech models generate.

The takeaway for valuation: the edtech sector median is 7.8x EV/Revenue in 2026, lower-middle-market edtech businesses typically trade between 3x and 10x earnings depending on size and model, and high-growth subscription companies command 5x to 9x ARR.

Subscription Metrics That Move EdTech Valuations

Two edtech businesses with identical revenue can sell for prices that differ by a factor of three. The difference lives in the subscription metrics, and in 2026 buyers price these with more precision than ever.

Net Revenue Retention: The Single Biggest Lever

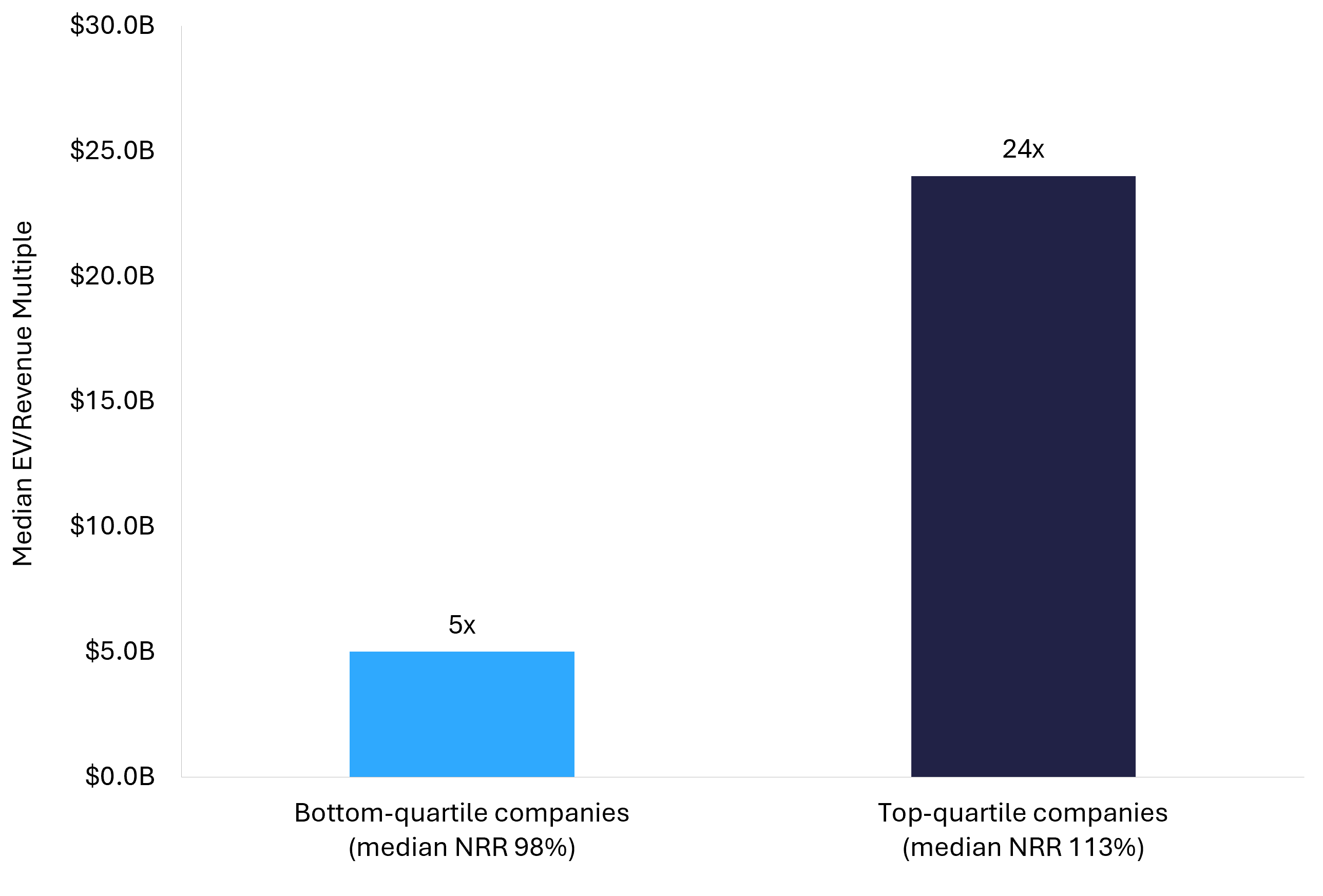

Net revenue retention (NRR) measures how much revenue you keep and expand from existing customers, before counting any new sales. The valuation impact is dramatic and well documented. McKinsey's analysis of more than 100 B2B SaaS companies found that top-quartile companies by valuation trade at a median 24x EV/Revenue against 5x for the bottom quartile, and the top quartile's defining trait is NRR of 113% versus 98% for the bottom. A 15-point retention gap corresponds to nearly a fivefold gap in multiple. Earlier McKinsey work on the Rule of 40 shows the same pattern: companies with NRR of 120% or more carried a median EV/Revenue of 21x against 9x for those below the line.

For edtech specifically, NRR shows up differently by model. Institutional businesses (districts, universities, corporate L&D) build NRR through seat expansion and multi-product adoption inside annual contracts. Consumer subscription products build it through plan upgrades and family or team tiers. Either way, FE International's guide to net revenue retention and SaaS valuation walks through the math showing a 10-point NRR improvement translating to a 20% to 30% valuation uplift, which makes retention the most valuable work a founder can do in the year before a sale. The encouraging part is that NRR moves: pricing tiers that create natural expansion paths, onboarding that drives early activation, and renewal outreach timed to usage data can all shift the number within two or three quarters.

Churn, Engagement, and the Numbers Behind Retention

Buyers read churn as the leak rate in your revenue bucket, and in education businesses they read engagement as the early-warning system for it. Course completion rates, weekly active learners, assignment submission rates: these are the leading indicators that predict whether a cohort renews. This is also where data analytics earns its place in an edtech valuation. A business that can show cohort-level dashboards connecting engagement to renewal gives a buyer confidence in the revenue forecast, and confident buyers pay higher multiples. A business that cannot produce that data invites conservative assumptions.

The Rule of 40 and Gross Margin

The Rule of 40 (revenue growth rate plus profit margin should total at least 40) remains the efficiency screen buyers apply to subscription edtech, and the market consistently rewards companies above the line with higher enterprise-value multiples. A business growing 30% with a 15% margin scores 45 and clears the bar; one growing 10% at breakeven scores 10 and should expect pricing pressure. The screen matters in edtech because the sector contains both profiles in large numbers, and buyers use it to separate efficient compounders from businesses buying growth they cannot afford.

Gross margin sets the floor underneath everything. Software-grade margins of 70% and up support software-grade multiples, while heavy human-delivery costs (live tutoring hours, manual grading, instructor payroll) pull a business toward services-style pricing unless the model demonstrates operating leverage. This is one place where AI is directly additive to edtech valuations: businesses that have automated grading, content generation, or learner support can show margin expansion in the actuals, not just the projections, and buyers pay for proof.

The takeaway for valuation: net revenue retention is the most powerful single metric in edtech business valuation, with documented multiple gaps of nearly 5x between top and bottom retention quartiles, followed by churn, engagement depth, Rule of 40 performance, and gross margin.

LTV in EdTech: Why Lifetime Value Per Learner Sets the Ceiling

Lifetime value (LTV) answers the question every acquirer ultimately asks: what is a customer worth over the full relationship? The standard formula divides gross-margin-adjusted average revenue per account by the churn rate, and the result sets the ceiling on what a buyer can rationally pay to acquire your customers along with your product.

In edtech the LTV math splits sharply by model, and buyers price the difference. An institutional contract with a school district or an enterprise L&D department often runs three to five years with high renewal probability, producing LTV measured in the tens or hundreds of thousands of dollars per logo. A consumer test-prep subscriber may stay four months, complete the exam, and leave, and no amount of marketing changes that natural endpoint. Neither model is wrong, but the institutional business converts each sales dollar into far more lifetime revenue, which is why B2B edtech consistently prices above B2C at the same revenue level.

The ratio that buyers examine is LTV to customer acquisition cost (CAC), with 3:1 the long-standing healthy threshold and the strongest operators running above 4:1. The economics behind the ratio are old and durable: acquiring a new customer costs 5 to 25 times more than retaining an existing one, which is why retention improvements compound into profit and valuation so quickly.

Edtech adds two wrinkles worth modeling honestly. First, seasonality: academic-calendar businesses concentrate acquisition in back-to-school windows, so CAC should be measured across a full year rather than a flattering quarter. Second, the natural completion point: a course business can extend LTV through alumni products, certifications, and subscription libraries, and buyers reward businesses that have already built those extension paths because the expansion revenue is proven rather than theoretical.

In practice, the way to present LTV in a sale process is through cohort tables rather than a single blended number. Show how the customers acquired in each month or semester behaved over time: how many remained at month 3, month 6, and month 12, what they spent, and how the curve has shifted as the product improved. A blended LTV figure invites skepticism because it mixes old cohorts with new ones; a cohort table shows a buyer the trajectory, and an improving trajectory is one of the strongest pricing arguments an edtech founder can make.

The takeaway for valuation: LTV per learner, measured against acquisition cost, determines how much growth a buyer can purchase with each dollar, and a 3:1 or better LTV-to-CAC ratio with documented cohort data supports premium edtech multiples.

What Drives EdTech Multiples Up (and What Buyers Discount)

Every edtech valuation conversation eventually becomes a list: which characteristics earn a premium, and which invite a discount. Here is the 2026 version of that list, drawn from live deal activity.

Premium Drivers

Recurring institutional revenue leads the list. Multi-year district, university, or enterprise contracts with auto-renewal language give buyers contracted visibility into future cash flow, and visibility is what multiples are made of. Documented learning outcomes come next: procurement teams in 2026 increasingly require efficacy evidence, so businesses that can show measurable improvement in learner persistence or skill acquisition clear diligence faster and price higher. Proprietary content libraries, owned training data, and distribution into hard-to-reach channels (K-12 districts, regulated industries, enterprise L&D systems) all function as moats that justify paying up. Diversified customer acquisition matters too. A business pulling learners from organic search, partnerships, email, and paid channels in balanced proportions carries less platform risk than one dependent on a single algorithm.

What Buyers Scrutinize

The discount list mirrors the premium list. Customer concentration is the most common issue we see: when one district, one corporate client, or one distribution partner accounts for a large share of revenue, buyers price the renewal risk into their offer or structure around it with earnouts. Founder dependence works the same way, which is why documenting processes and building a team that runs without you directly converts into valuation. Revenue mix gets examined closely in 2026: one-time course sales, implementation fees, and pandemic-era stimulus-funded contracts all get weighted below true recurring subscription revenue, so shifting your mix toward subscriptions ahead of a sale is among the most valuable preparation work available.

Business Model and Segment: Where You Play Shapes the Multiple

Business model is itself a valuation input. Workflow-embedded B2B learning platforms top the hierarchy because switching costs protect revenue. Marketplaces with real liquidity (Preply's tutor network is the current reference case) earn platform economics. Consumer subscription apps price on the strength of their retention curves. Pure content businesses, without platform features that lock in usage, price lowest per revenue dollar because content is the easiest layer to replicate. Segment matters in parallel: K-12 businesses benefit from sticky multi-year procurement but carry budget-cycle exposure, higher education tools sell into longer cycles with strong renewal behavior, and corporate learning currently attracts the broadest buyer pool because employers fund it from operating budgets tied directly to the reskilling pressure described earlier.

The takeaway for valuation: recurring institutional revenue, efficacy evidence, proprietary data, and diversified acquisition push edtech multiples up, while customer concentration, founder dependence, and one-time revenue mixes are the discounts buyers most commonly apply.

What Acquirers Actually Paid: Real EdTech Deals From 2024 to 2026

Benchmarks are useful, but completed transactions are proof. Here is what buyers actually paid across the recent cycle, from the megadeals down to the founder-scale exits.

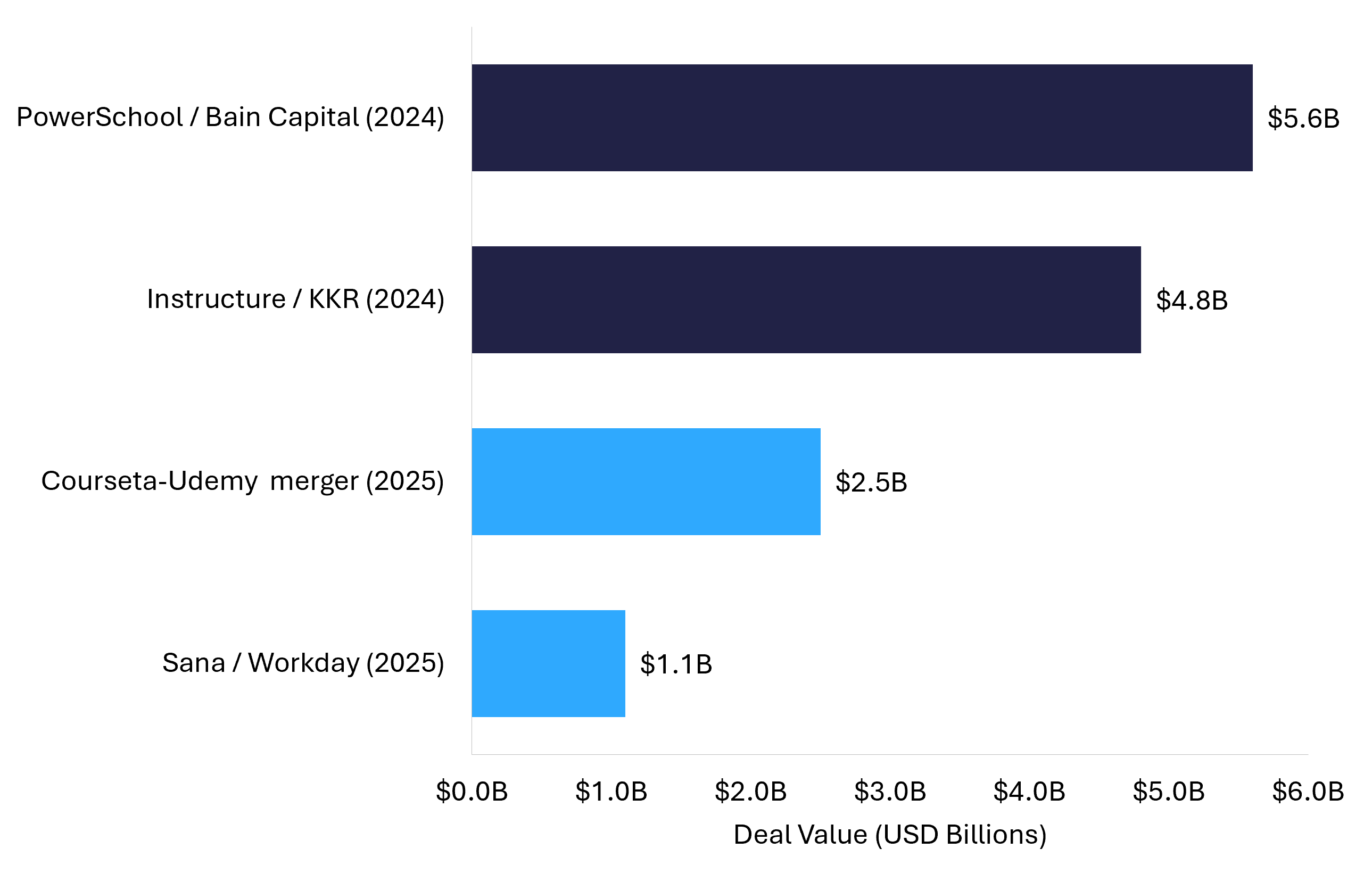

Bain Capital acquired PowerSchool for $5.6 billion, paying $22.80 per share, a 37% premium to the unaffected price, for the K-12 software provider serving more than 55 million students across 17,000 customers. Weeks later, KKR took Instructure private at $4.8 billion, a 16% premium for the company behind the Canvas learning management system. Two multibillion-dollar take-privates in one summer told the market that private equity views established education software as core infrastructure worth owning through cycles.

The strategic buyers then raised the stakes. Workday completed its $1.1 billion acquisition of Sana in November 2025, buying an AI-native learning and knowledge platform to anchor its enterprise suite, a deal that priced capability rather than current revenue. And in December 2025, Coursera and Udemy announced their combination at roughly $2.5 billion in implied equity value, with a 26% premium to Udemy holders and $115 million in expected annual synergies, creating a consumer-and-enterprise learning company at $1.5 billion in revenue. The deal is expected to close in the second half of 2026.

The funding market reinforces what the deal market is saying. Preply's January 2026 round, which made the language-learning company the newest edtech unicorn at a $1.2 billion valuation, demonstrated that investors still write large checks for education businesses with global scale and credible AI strategies. For founders, funded competitors at premium valuations are good news in a sale process: they validate the category and frequently become acquirers themselves.

Activity at the founder scale is just as instructive, even if the numbers are smaller. FE International advised the founders of PositivePsychology.com, a learning platform serving more than 19 million users, through an eight-figure exit built on exactly the fundamentals this guide describes: organic acquisition, strong engagement and retention metrics, and clean financials. The same buyer demand driving billion-dollar take-privates reaches down into the lower middle market, where strategic operators, PE-backed platforms making add-on acquisitions, and individual buyers compete for well-run edtech assets. FE International's analysis of edtech M&A buyer behavior in 2026 maps these three buyer types in detail, and the practical implication is simple: a competitive process that reaches all three is the most reliable path to a premium price.

The takeaway for valuation: between 2024 and 2026, acquirers paid premiums of 16% to 37% for established edtech platforms in deals from $1.1 billion to $5.6 billion, and the same buyer competition extends to founder-owned businesses at every size band.

The AI Effect on EdTech Valuations in 2026

No factor moves a 2026 edtech valuation conversation faster than AI, in both directions, and founders should understand exactly how buyers now price it.

The capital flow sets the context. AI startups captured 65% of total US venture deal value in 2025, and within technology M&A, almost half of 2025 tech deals carried an AI component, up from roughly one in four a year earlier. Education is participating fully: AI-focused learning tools are the fastest-growing slice of the sector, and the Workday-Sana transaction showed a strategic buyer paying $1.1 billion primarily for AI-native learning capability.

Diligence has evolved to match. One in five strategic dealmakers walked away from a deal in 2025 specifically because of AI's anticipated impact on the target's business, which means every edtech seller should expect an AI-impact assessment as a standard diligence workstream. The question buyers ask is whether AI strengthens your moat or threatens your category. Products embedded in institutional workflows with proprietary data, fine-tuned models, or efficacy evidence sit on the right side of that question. Products whose core function a general-purpose model can replicate need a differentiation story, and building one before going to market is far better than improvising one in diligence.

For prepared founders this environment is a genuine opportunity. Buyers across all three pools are actively seeking AI-capable learning assets, AI-native businesses are commanding premium attention, and even non-AI edtech businesses benefit when they can show a credible roadmap for integrating AI into the product and the cost base.

The takeaway for valuation: AI readiness now functions as a multiplier in edtech business valuation, with AI-capable assets drawing premium competition while every seller should prepare for AI-impact diligence as a standard part of the 2026 process.

How to Prepare an EdTech Business for a Premium Exit

Valuation is determined long before a buyer appears. The edtech businesses that sell at the top of their range share preparation patterns, and most of the work fits inside a 6 to 18 month window.

Start with the financials. Separate personal expenses, normalize one-time costs, and produce 24 to 36 months of clean monthly P&L statements that reconcile to payment-processor data. Buyers verify revenue against Stripe or its equivalents, and clean reconciliation builds the trust that keeps a process moving.

Instrument your metrics next. Build the cohort retention dashboards, NRR calculations, engagement-to-renewal analyses, and LTV-to-CAC tracking described throughout this guide. The businesses that present these numbers proactively control the diligence narrative; the ones that cannot produce them concede pricing power.

Then work the levers. Convert one-time course sales into subscription or membership revenue where the product supports it. Reduce any customer above 15% to 20% of revenue through deliberate diversification. Document learning outcomes, because efficacy evidence is now a procurement requirement and a diligence asset. Lock in IP assignments from every contractor who touched your codebase or content. And reduce founder dependence by documenting processes and delegating the functions a buyer will worry about.

Timing the market matters less than founders assume; timing the business matters more. The strongest moment to sell is when growth is visible in the trailing twelve months, retention cohorts are improving, and the next year's pipeline is already partially contracted, because buyers pay for momentum they can verify. Every element of edtech business valuation discussed in this guide, from the SDE add-back schedule to the NRR trend line, is something a buyer will test, and sellers who arrive with the evidence assembled negotiate from strength.

Finally, choose the right channel for your size. Businesses under $1 million in value move efficiently through FE International's M&A Platform, where sellers reach qualified, vetted buyers and buyers evaluate verified listings with live metrics. Larger businesses warrant the full advisory process, with senior deal teams running competitive auctions across strategic, private equity, and individual buyer pools. Both paths exist inside one ecosystem, so the right starting point is simply an honest read on what your business is worth today.

The takeaway for valuation: clean financials, instrumented retention metrics, a subscription-weighted revenue mix, documented outcomes, and the right deal channel for your size are the preparation steps that consistently move edtech businesses to the top of their valuation range.

Know What Your EdTech Business Is Worth

Edtech business valuation in 2026 rewards founders who understand their numbers. The market is compounding toward $456 billion by 2030, acquirers from private equity to global strategics paid 16% to 37% premiums across the recent deal cycle, and the metrics that separate a median multiple from a premium one (net revenue retention, LTV-to-CAC, engagement-backed cohort data) are all measurable and improvable today.

The methods are equally clear. SDE for owner-operated businesses, adjusted EBITDA once a team runs the company, and revenue or ARR multiples for high-growth subscription models, benchmarked against a sector median of 7.8x EV/Revenue and lower-middle-market earnings multiples of 3x to 10x.

What those benchmarks cannot tell you is the number for your business. That takes a direct look at your financials, your retention cohorts, and your buyer fit. FE International has advised on more than 1,500 technology transactions with a 94.1% success rate, including edtech exits from eight-figure platform sales to founder-scale deals through its M&A Platform. Request a free, confidential valuation and find out exactly what acquirers would pay for your edtech business in 2026.