.jpg)

.jpg)

The cybersecurity industry is experiencing its most aggressive wave of M&A activity on record. In 2025, disclosed deal value across cybersecurity transactions reached $92.5 billion across 426 deals, with eight acquisitions surpassing the $1 billion mark. Google's $32 billion purchase of Wiz, Palo Alto Networks' $25 billion acquisition of CyberArk, and ServiceNow's $7.75 billion deal for Armis have reset the bar for what buyers will pay for cybersecurity assets.

For founders and business owners in the cybersecurity space, this raises a practical question: what is your company actually worth? The answer depends on where your business sits along the maturity spectrum, how your revenue is structured, and which metrics buyers care about most. This guide breaks down the valuation methods, benchmark multiples, and M&A dynamics shaping cybersecurity business valuations in 2026, whether you run a bootstrapped security tools company generating $500K in annual earnings or a venture-backed platform with $20M in ARR.

We will walk through SDE, EBITDA, and revenue-based valuation approaches; share specific multiples by business size and niche; explain the metrics that push multiples higher (or lower); and map the buyer landscape so you know who is acquiring and why. If you are considering a sale, raising capital, or simply benchmarking your company's value, this is the data you need.

Key takeaway: Cybersecurity remains one of the few technology subsectors commanding sustained premium valuations in 2026, supported by record M&A activity, expanding enterprise spending, and a growing global threat landscape.

Why Cybersecurity Valuations Are at a Premium in 2026

Cybersecurity is not just growing; it's accelerating. Gartner forecasts that global information security spending will reach $240 billion in 2026, up 12.5% from $213 billion in 2025. That's a meaningful jump from 2025's comparatively modest 10% growth. Fortune Business Insights projects the broader cybersecurity market at $248 billion in 2026, growing at a 13.8% CAGR through 2034.

Several forces are driving this expansion. AI-powered cyberattacks have fundamentally changed the threat landscape: adversaries are using large language models to automate phishing campaigns, discover vulnerabilities, and generate polymorphic malware that evades traditional detection. Cybersecurity Ventures estimates global cybercrime costs will reach $10.5 trillion in 2025 and continue climbing. Regulatory pressure from frameworks like the EU's NIS2 Directive and the Cyber Resilience Act is forcing organizations to invest in compliance-ready security solutions.

For business owners, this tailwind matters. Buyers and investors pay premium multiples for companies operating in growing markets with strong structural demand. Cybersecurity checks both boxes, which is why PwC's 2026 M&A outlook identifies the sector as one of the few tech subsectors attracting sustained premium valuations even as other categories face compression.

.png)

Three Core Valuation Methods for Cybersecurity Businesses

The right valuation method depends on your company's size, growth rate, and profitability. Here's how each method applies in cybersecurity, and when to use which.

SDE (Seller's Discretionary Earnings): For Owner-Operated Businesses Under $5M

SDE captures the total economic benefit flowing to a single owner-operator. It takes net income and adds back the owner's salary, personal expenses run through the business, one-time costs, and non-cash charges like depreciation. For cybersecurity businesses generating under $5 million in annual revenue with limited management infrastructure, SDE is typically the most appropriate valuation basis.

We see small cybersecurity services firms and niche security tool providers selling in the range of 3x to 5x SDE. According to BizBuySell transaction data for 2025, the average SDE multiple across all small businesses was approximately 2.5x, but technology and software businesses consistently command a premium. Cybersecurity firms with recurring managed service contracts or subscription-based tools land toward the higher end of that range due to the predictability of their revenue.

A sole-proprietor MSSP (Managed Security Services Provider) with $300K in SDE and stable month-over-month contracts might reasonably expect a valuation of $900K to $1.5M, depending on client concentration, contract length, and whether the owner can be replaced without losing key relationships.

EBITDA Multiples: For Mature, Profitable Businesses

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is the standard valuation metric for cybersecurity businesses with established management teams, predictable earnings, and revenues above $2-5 million. Private equity buyers in particular gravitate toward EBITDA because it measures operational cash flow independent of capital structure.

For profitable private cybersecurity companies, EBITDA multiples typically range from 10x to 20x, according to Biz Advisory Board's cybersecurity valuation analysis. The specific multiple depends heavily on growth rate, market position, and buyer type. Service-oriented cybersecurity businesses with traditional billing models tend to sell in the 5x to 9x EBITDA range, as noted by Jackim Woods & Co. Companies with software-driven recurring revenue, strong margins above 20%, and consistent growth command the higher end of the range.

For context, Breakwater M&A's 2026 benchmarks show IT consulting and services firms in the $2M-$20M revenue range trading at 4x to 7x EBITDA, with specialized cybersecurity firms reaching 8x to 10x. The premium reflects the strategic value and recurring nature of security engagements.

Revenue Multiples: For High-Growth SaaS and Platform Businesses

Revenue-based valuation is the standard for high-growth cybersecurity SaaS companies, particularly those reinvesting aggressively and not yet generating meaningful EBITDA. The logic is straightforward: when a company is deliberately running near breakeven to capture market share, current earnings understate the business's true value. Revenue serves as a proxy for future cash flow potential.

The range here is wide. Finro's mid-2025 analysis of 250+ cybersecurity companies found that public cybersecurity companies traded at a median 7.8x revenue, while private startups averaged 15.2x revenue and M&A transactions commanded a median 16.3x revenue. High-growth firms in cloud security and identity access management routinely see 15x to 30x in private markets.

As FE International's SaaS valuation methodology explains, revenue multiples are entirely predicated on growth. A cybersecurity company with $10M in ARR growing at 40% year-over-year will command a fundamentally different multiple than one with the same revenue growing at 10%. Without growth, the revenue multiple thesis falls apart.

Quotable summary: The choice between SDE, EBITDA, and revenue multiples depends on company size and growth profile. Owner-operated cybersecurity firms under $5M use SDE (3-5x). Profitable businesses with management teams use EBITDA (10-20x for software, 5-9x for services). High-growth SaaS platforms use revenue multiples (5-30x depending on growth rate and niche).

.png)

2026 Benchmark Multiples by Cybersecurity Niche

Not all cybersecurity businesses are valued equally. The specific niche within cybersecurity has a significant impact on the multiple a buyer will pay. Cloud security and identity access management are currently the most sought-after categories, while traditional network security trades at a discount.

Cloud security leads with the highest revenue multiples across all market segments. Finro's data shows average private-market cloud security valuations at 21.7x revenue, with M&A transactions reaching as high as 35.5x. Google's $32 billion acquisition of Wiz (valued at roughly 45x its run-rate revenue at the time of the original deal structure) set the ceiling, though that reflects a once-in-a-generation strategic acquisition rather than a market norm.

Identity and access management (IAM) is the second-highest-valued niche. Palo Alto Networks' $25 billion purchase of CyberArk underscores the premium buyers place on identity security as enterprises shift to zero-trust architectures. Herbert Smith Freehills' 2026 M&A analysis notes that identity emerged as a central M&A theme in 2025, reflecting the accelerating adoption of zero-trust models across distributed cloud platforms and remote workforces.

OT/IoT security is an emerging premium category. Mitsubishi Electric's $1 billion acquisition of Nozomi Networks represents the largest OT security deal ever, signaling strong buyer appetite for operational technology protection as critical infrastructure threats intensify.

Application security, data security, and GRC (Governance, Risk, and Compliance) occupy the middle ground, with public multiples typically in the 6x to 8x revenue range and private deals at 10x to 14x. Network security, while still essential, trades at the lower end of the cybersecurity spectrum due to commoditization pressures.

.png)

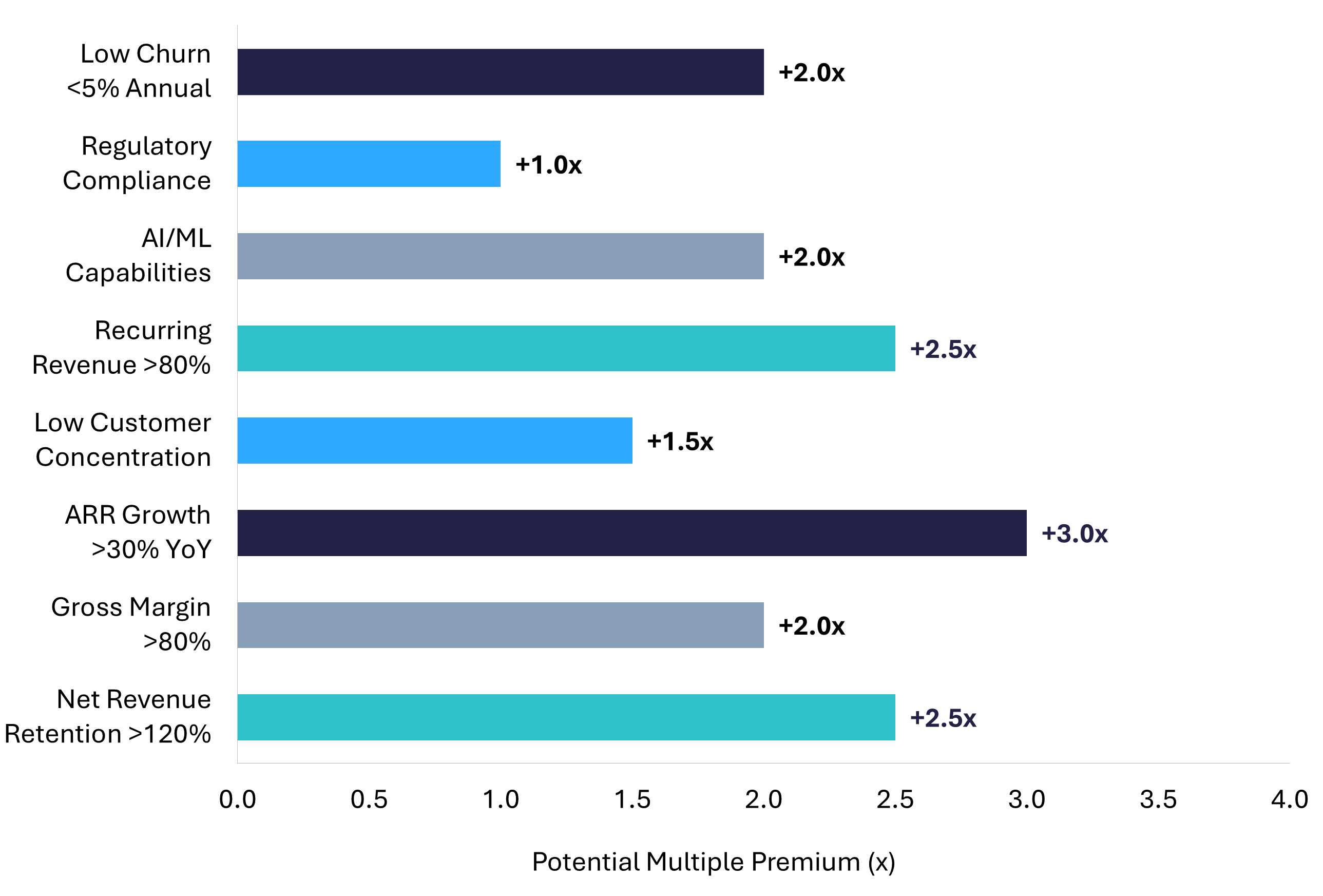

Key Metrics That Drive Cybersecurity Valuation Multiples Up or Down

Buyers in the cybersecurity space evaluate a specific set of metrics to determine where within a valuation range a company falls. Understanding these metrics, and optimizing them before going to market, is often the difference between a mid-range and a premium exit.

Annual Recurring Revenue (ARR) and Monthly Recurring Revenue (MRR)

ARR is the single most important number in cybersecurity company valuations, particularly for SaaS models. Buyers pay for predictability. A cybersecurity company with $5M in ARR from multi-year contracts is a fundamentally more attractive acquisition than one with $5M in project-based revenue, even if total revenue is identical. The distinction is risk: recurring revenue reduces the buyer's uncertainty about future cash flows.

Net Revenue Retention (NRR)

NRR measures how much revenue you keep and expand from your existing customer base year over year. An NRR above 100% means your customers are spending more over time, even before new sales. Top cybersecurity companies achieve NRR above 120%. Palo Alto Networks reports that its platform customers achieve 120% NRR with near-zero churn. SaaS Capital's 2025 benchmarks show the median NRR for private B2B SaaS companies is 106%, with top-quartile performers exceeding 115%. In cybersecurity specifically, NRR tends to run higher than typical SaaS because security products are deeply embedded into customer operations and difficult to rip out.

Gross Margins

Higher margins signal scalability. Cybersecurity SaaS companies with gross margins above 80% command premium multiples because each additional dollar of revenue translates to meaningful profit without proportional cost increases. Service-heavy cybersecurity businesses typically see gross margins between 40% and 60%, which is one reason they sell at lower multiples. If your business blends software and services, clearly separating the revenue streams in your financials can help buyers value the software component at a premium.

Growth Rate

Growth is the single largest multiplier on valuation. Solganick & Co.'s Q3 2024 cybersecurity market update found that publicly traded cybersecurity companies growing above 20% annually traded at a median 9.5x forward revenue, while those growing under 10% traded at just 4.0x. That's a 2.4x difference in valuation multiple driven entirely by growth rate. The message is clear: if you can accelerate growth before going to market, the return on that investment shows up directly in your valuation.

Customer Concentration and Churn

A business where the top three clients represent 60% of revenue carries significant key-person and key-account risk. Buyers discount heavily for customer concentration. Similarly, annual customer churn above 10% is a red flag that suppresses multiples. The best cybersecurity businesses maintain diversified customer bases with no single client exceeding 10-15% of revenue and annual dollar churn below 5%.

AI and Automation Capabilities

AI-native cybersecurity capabilities are commanding meaningful premiums in 2026. Momentum Cyber's 2025 M&A report identified AI-driven startups as commanding the highest valuations and strongest venture capital interest. Companies that use AI for threat detection, automated response, or security analytics are positioned to capture the growing enterprise demand for intelligent security platforms.

M&A Trends Shaping Cybersecurity Valuations in 2026

The cybersecurity M&A market in 2025-2026 is defined by three structural shifts: platform consolidation, the return of strategic buyers, and record deal volume. Understanding these trends helps sellers position their businesses for the right buyers at the right time.

Platform Consolidation Is Accelerating

The dominant theme is platformization. CISOs are under pressure to reduce vendor sprawl, and the major cybersecurity vendors are responding by acquiring companies that fill gaps in their product suites. Infosecurity Magazine reports that market demand shifted from 'buying growth' to 'buying cash flow and platform density' in 2025. Palo Alto Networks alone completed four major acquisitions in 2025. CrowdStrike followed with targeted purchases in identity management and AI. This creates a favorable environment for mid-market cybersecurity companies with differentiated technology that fills a platform gap.

Strategic Buyers Dominate

Strategic acquirers deployed 92% of all M&A capital in cybersecurity in 2025, a significant shift from the private equity-driven deal flow of previous years. Google, Palo Alto Networks, CrowdStrike, ServiceNow, and Check Point led acquisition activity. The pace has continued into early 2026: SecurityWeek tracked 42 deals in February 2026 and 38 in March 2026, with no signs of slowing down.

Record Financing Fuels the Pipeline

Cybersecurity financing reached $20.7 billion across 820 deals in 2025, up 52% from 2024, according to Momentum Cyber. The median Series C+ deal size increased from $50M in 2023 to over $80M in 2025. This capital infusion creates a healthy pipeline of scaling companies that will either IPO or be acquired in the coming years. Netskope's successful NASDAQ listing in September 2025 (at a $9.6 billion market cap) reopened the IPO window, with Windsor Drake noting that Cato Networks, Claroty, and Snyk are among the late-stage companies preparing for public listings in 2026.

.png)

Real Deal Examples: What Buyers Are Paying

Abstract multiples become concrete when you look at actual transactions. Here are six 2025-2026 deals that illustrate the range of cybersecurity valuations across different segments.

Google acquiring Wiz ($32 billion): The largest cybersecurity acquisition in history. Wiz, a cloud security platform, was valued at roughly 40-45x its reported annual revenue at the time the deal was announced. This is an outlier driven by Google's strategic urgency to strengthen its cloud security position, but it signals the ceiling for category-defining platforms.

Palo Alto Networks acquiring CyberArk ($25 billion): CyberArk, an identity security leader, was acquired as part of Palo Alto's platformization strategy. The deal reflects the premium placed on identity and privileged access management as zero-trust adoption accelerates across enterprises.

ServiceNow acquiring Armis ($7.75 billion): Armis, specializing in asset discovery across IT, OT, and IoT, was valued at approximately 15x its annual recurring revenue. This deal highlights the premium for companies operating at the intersection of security and operational technology.

CrowdStrike acquiring SGNL ($740 million): An identity management startup acquired in early 2026, demonstrating that even sub-$1B deals in cybersecurity command strong valuations when the technology fills a strategic platform gap.

Varonis acquiring AllTrue.ai ($150 million): A targeted AI security acquisition focused on trust, risk, and security management for AI systems. This mid-market deal illustrates how AI security capabilities are commanding premium valuations even for smaller companies.

Mitsubishi Electric acquiring Nozomi Networks ($1 billion): The largest OT security acquisition ever recorded. This cross-border deal between a Japanese industrial giant and an operational technology security specialist demonstrates the strategic value of niche cybersecurity expertise.

Quotable summary: In 2025-2026, cybersecurity M&A deal values range from $150 million for AI security startups to $32 billion for category-defining cloud platforms. Revenue multiples in disclosed deals ranged from approximately 10x to 45x, with the specific multiple driven by growth rate, strategic fit, and the acquirer's competitive urgency.

How Business Size Affects Your Cybersecurity Valuation

The headlines about billion-dollar cybersecurity deals can be misleading if you run a smaller operation. Valuation dynamics differ significantly based on where your business falls on the revenue spectrum. Understanding these tiers helps set realistic expectations.

Under $1M in annual earnings (SDE businesses): Most cybersecurity businesses at this scale are owner-operated MSSPs, consulting practices, or niche security tools. Buyers are typically individual acquirers or small PE firms. Valuations run 3x to 5x SDE. The priority metrics at this level are owner-replaceability, client retention, and contract structure. As FE International's valuation guide explains, typical internet and SaaS business valuations range from 3x to 10x annual net income, with the lower end applying to owner-dependent operations.

$1M to $5M in annual revenue: This is the transition zone. Businesses here may be valued on SDE or EBITDA depending on whether a management team is in place. SaaS-model cybersecurity companies at this level often see 5x to 7x multiples, per FE International's SaaS valuation benchmarks. Adding a management layer and reducing owner involvement can meaningfully increase valuation.

$5M to $20M in revenue: This is the sweet spot for lower middle market M&A. EBITDA-based valuations are standard, and multiples of 7x to 10x are common for well-run cybersecurity companies with recurring revenue. Private equity buyers are active at this level, and competition between buyers tends to push multiples upward. Specialization in high-demand niches like cloud security or AI-driven threat detection can add 1-2x to the multiple.

$20M+ in revenue: At this scale, cybersecurity companies attract strategic acquirers and larger PE platforms. Revenue multiples become more common, and the range widens dramatically based on growth rate. The Aventis Advisors software M&A dataset shows a median EV/Revenue of 3.7x across all software transactions, but with top-quartile cybersecurity deals reaching 7x+ on revenue and 12x+ on EBITDA.

How AI Is Reshaping Cybersecurity Valuations

AI has become a valuation accelerator in cybersecurity. Companies with genuine AI-native capabilities are being acquired faster, at higher multiples, and with more buyer competition than their non-AI counterparts.

The numbers tell the story. In 2025, multiple AI-focused cybersecurity acquisitions occurred at notable valuations: Palo Alto Networks paid $700 million for Protect AI (LLM security), SentinelOne acquired Observo AI for $225 million, and Check Point purchased Lakera for $300 million. In early 2026, OpenAI acquired Promptfoo (an AI red-teaming platform), and Databricks purchased two cybersecurity startups to launch its AI-powered SIEM platform.

Gartner's 2026 cybersecurity trends report identifies agentic AI oversight, IAM for machine actors, and GenAI governance as three of the six forces reshaping CISO priorities. Companies that address these challenges have built-in buyer demand.

A word of caution: Windsor Drake's Q4 2025 valuation report warns that investors will soon demand revenue proof from AI security companies. Firms claiming AI capabilities without distinct IP will see valuations correct. The winners will be those securing the AI pipeline itself, protecting LLMs, data lakes, and inference models, and those using AI to fundamentally reduce the cost of security operations.

The Buyer Landscape: Who Is Acquiring Cybersecurity Companies in 2026

Understanding who buys cybersecurity companies helps you position your business for the right audience. In 2026, three buyer categories dominate, each with distinct motivations and valuation approaches.

Strategic Acquirers

Large cybersecurity vendors and technology companies are the most active buyers and typically pay the highest multiples. Palo Alto Networks, CrowdStrike, Google, Check Point, Zscaler, and ServiceNow led acquisition activity in 2025-2026. These buyers are building end-to-end security platforms and are willing to pay premium valuations for technology that fills a gap in their product suite. If your company has proprietary technology in cloud security, identity management, AI security, or data protection, strategic buyers are your most likely acquirers. They evaluate targets based on technology fit, customer overlap, and integration potential, not just financial metrics.

Private Equity

Private equity firms deployed more than twice as much capital in cybersecurity in 2025 compared to 2023. Thoma Bravo, Francisco Partners, TA Associates, Vitruvian Partners, and Advent International remain the most active PE buyers in the space. PE firms typically target profitable businesses with $5M to $50M in revenue and stable, recurring cash flows. They are often more valuation-disciplined than strategic buyers but can move quickly and offer structured transactions that let founders retain partial equity. Francisco Partners' $2.2 billion acquisition of Jamf in 2025 is a representative example of PE-scale cybersecurity dealmaking.

Individual Acquirers and Search Funds

For smaller cybersecurity businesses with $500K to $3M in annual revenue, individual acquirers, search funds, and smaller PE groups represent the primary buyer pool. These buyers are often former cybersecurity executives or operators looking to acquire and grow a platform. They typically use SDE-based valuations and may rely on SBA financing, which caps maximum loan amounts and influences deal structure. Businesses at this level benefit from having clean financials, documented processes, and a clear transition plan for the departing owner.

Cybersecurity vs. Other Technology Sectors: A Valuation Comparison

How do cybersecurity valuations compare to other technology verticals? The short answer: cybersecurity generally commands a premium, but the gap varies depending on the specific sub-sector being compared.

Across all software M&A transactions from 2015 to 2025, Aventis Advisors reports a median EV/Revenue multiple of 3.7x. Cybersecurity consistently trades above this benchmark. Public cybersecurity companies average 7.8x revenue, roughly double the median software company. The premium reflects cybersecurity's essential nature: unlike discretionary software purchases that can be delayed, security spending is non-negotiable for most organizations, particularly in regulated industries.

Compared to general SaaS businesses, which FE International benchmarks in the 5x to 10x range for businesses under $20M in revenue, cybersecurity SaaS typically commands a 20-40% premium. The premium stems from higher customer retention rates (security products are deeply embedded and costly to switch), stronger pricing power (organizations rarely downgrade security), and structural demand growth that persists through economic cycles.

Cybersecurity also compares favorably to fintech, which has seen significant valuation compression since 2022. While fintech companies are navigating regulatory headwinds and margin pressure, cybersecurity benefits from the opposite dynamic: regulations like NIS2 and the Cyber Resilience Act are forcing more spending on security, not less. AI companies represent the one technology sub-sector currently commanding comparable or higher multiples than cybersecurity, but AI valuations carry more uncertainty given the rapidly shifting competitive landscape. Cybersecurity companies that combine both AI capabilities and core security value occupy the intersection of two premium-valued sectors.

Quotable summary: Cybersecurity businesses consistently trade at a 20-40% premium over general SaaS valuations. The premium reflects essential, non-discretionary demand, high customer retention, and structural growth driven by expanding threats and regulatory requirements.

Preparing Your Cybersecurity Business for a Premium Valuation

Knowing what your business could be worth and actually achieving that valuation are two different things. The cybersecurity companies that sell at the top of their range share common preparation patterns.

Clean your financials. Separate personal expenses, normalize one-time costs, and present 24-36 months of clear P&L statements. Buyers want to see trends, not just snapshots. As FE International's SaaS exit planning guide emphasizes, understanding every aspect of your financials from the outset is vital to a successful sale.

Maximize recurring revenue. Convert project-based engagements to retainer agreements where possible. Even shifting 20-30% of revenue to recurring contracts can add 1-2x to your EBITDA multiple. Buyers distinguish sharply between project work and contracted recurring revenue.

Reduce owner dependency. If you are the primary relationship holder with clients, the primary technical resource, or the sole decision-maker, that creates risk for buyers. Building a management team, even a small one, and documenting processes turns your company from a job into a business, and the valuation reflects it.

Track and present your SaaS metrics. If your business has a subscription component, measure and report ARR/MRR, NRR, gross margin, churn, CAC, and LTV. These are the metrics buyers use to benchmark your company against comparable transactions. Arriving at the table with these numbers already calculated signals operational maturity.

Time the market. With cybersecurity M&A at record levels and strategic buyers actively acquiring, 2026 represents a favorable window. Herbert Smith Freehills projects that M&A activity will remain elevated through 2026, driven by structural cybersecurity demand rather than transient cyclical conditions. Waiting for an even better environment carries the risk of market conditions shifting.

How Regulations and Compliance Requirements Affect Cybersecurity Valuations

Regulatory developments are becoming a direct valuation driver in cybersecurity M&A. Companies that help organizations achieve and maintain compliance with evolving frameworks command measurable premiums over those that do not.

The EU's NIS2 Directive, which became enforceable in October 2024, requires organizations across critical sectors to implement cybersecurity risk management measures and report significant incidents. The Cyber Resilience Act, entering into force in phases through 2027, extends security requirements to connected devices and software products. In the United States, the SEC's cybersecurity disclosure rules (effective December 2023) require public companies to report material cybersecurity incidents within four business days and describe their governance processes for managing cyber risk.

For cybersecurity companies, these regulations create two valuation tailwinds. First, they expand the total addressable market by making security spending mandatory for categories of organizations that previously treated it as optional. Gartner's 2026 trends analysis identifies global regulatory volatility as one of the six forces reshaping CISO priorities. Second, companies with solutions purpose-built for regulatory compliance, particularly GRC (Governance, Risk, and Compliance) platforms, attract premium attention from buyers who see regulatory tailwinds as a durable growth catalyst.

Cross-border regulatory dynamics are also driving M&A structure. Herbert Smith Freehills observes that US-based vendors are acquiring European-native firms specifically to gain compliant local hosting and support structures that satisfy EU sovereignty requirements. This creates opportunity for European cybersecurity companies with established compliance credentials and local market presence.

If your cybersecurity business serves regulated industries like healthcare, financial services, or government, or if your product directly supports compliance with specific regulatory frameworks, make that a central part of your positioning when going to market. Buyers are actively seeking assets that reduce their customers' compliance burden, and they pay more for proven regulatory alignment.

Conclusion: Get Your Cybersecurity Business Valued

Cybersecurity business valuations in 2026 are shaped by a convergence of record M&A activity, accelerating enterprise spending, and structural tailwinds from AI adoption and regulatory expansion. Whether your company is a $500K owner-operated MSSP or a $30M SaaS platform, the fundamentals are the same: buyers pay for recurring revenue, growth, and strategic positioning. The specific multiple depends on which valuation method applies to your business, how your key metrics compare to benchmarks, and how well you prepare for the transaction process.

The cybersecurity M&A window is open. With strategic buyers actively acquiring, private equity sitting on record dry powder, and multiple avenues to exit available, well-prepared cybersecurity businesses are commanding premium valuations. The question is not whether to explore your options, but when.

Ready to find out what your cybersecurity business is worth? Get a free, confidential valuation from FE International. With over 1,500 completed transactions and deep expertise in SaaS, cybersecurity, and technology M&A, FE International's team provides data-driven valuations and end-to-end advisory for founders looking to achieve the best possible outcome. Start the conversation today.