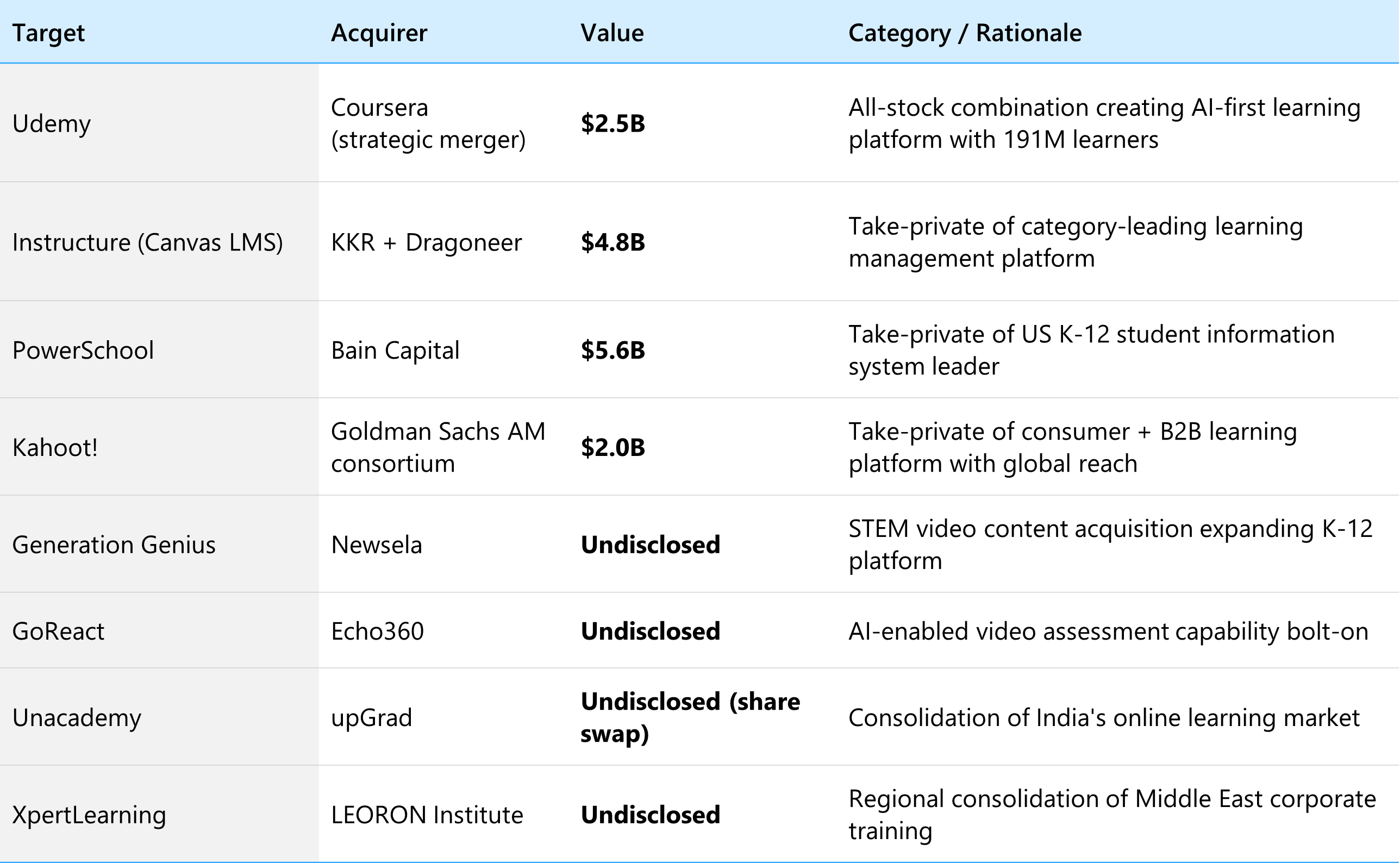

The defining moment for edtech M&A in 2026 was not a single deal. It was the realization that capital had decided where it wants to go. The $2.5 billion all-stock combination of Coursera and Udemy, which closed in May, sat alongside KKR's $4.8 billion take-private of Instructure and Bain Capital's $5.6 billion acquisition of PowerSchool as marquee proof points that scaled, workflow-embedded learning platforms are the assets serious capital wants to own.

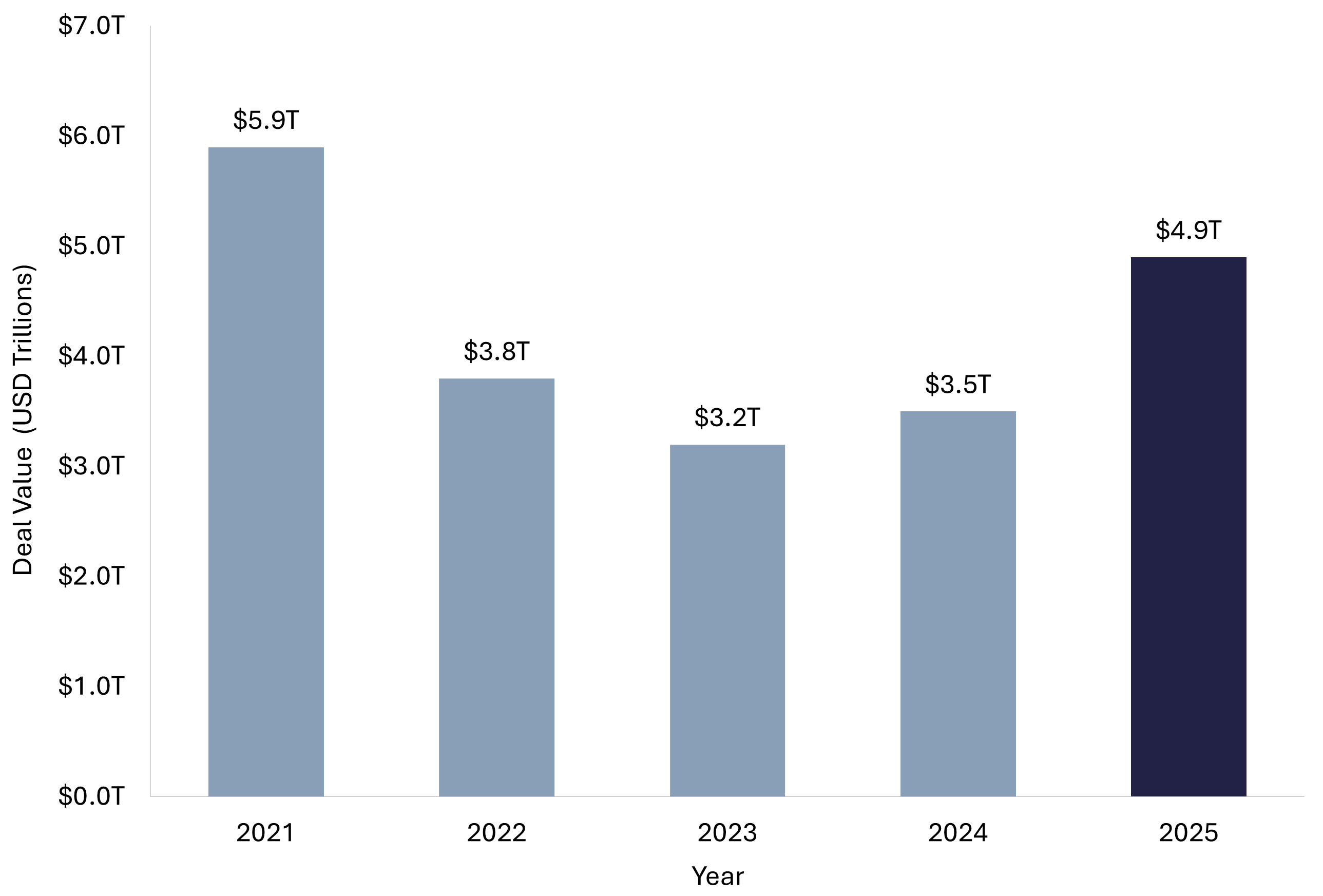

Global M&A as a whole rebounded 40% in 2025 to $4.9 trillion, the second-highest annual deal value on record. EdTech sat squarely inside that recovery. HolonIQ counted roughly 360 EdTech transactions for 2025, concentrated in systems, infrastructure, and job-aligned upskilling. The companies that traded are increasingly the ones with sticky enterprise contracts, defensible AI moats, and verifiable learner outcomes. That is the consistent thread running through nearly every category active today.

For founders of edtech businesses, whether you're running a seven-figure SaaS platform for corporate L&D or a sub-million-dollar tutoring app with strong unit economics, the 2026 environment is built around your reality. Buyers want sectors with measurable outcomes. Capital wants AI-native infrastructure. Strategics want scale. Sponsors want predictable cash flow. Every one of those vectors creates a path to liquidity, and the rest of this analysis walks through where that demand is concentrating, what it is paying, and how to position your business inside it.

The 2026 EdTech M&A Landscape: A Market Rewarded for Quality and Outcomes

Three forces shape edtech M&A in 2026. The first is the broader recovery in dealmaking. The second is the maturation of AI from experimentation to embedded workflow. The third is a discipline shift among buyers, who now reward platforms that prove retention, persistence, and outcomes over those that simply add users.

Start with the macro. Bain's 2026 Global M&A Report surveyed more than 300 M&A executives and found that 80% expect to sustain or increase deal activity in 2026. Almost half of all technology deals already have an AI angle. Strategic buyers are putting M&A back at the center of growth strategy after a multi-year reset, and 60% of $1 billion-plus deals in 2025 were scope deals, the highest rate ever recorded, a clear signal that acquirers are buying capabilities, not just scale.

Inside that broader rebound, edtech is benefiting from a specific tailwind. HolonIQ's 2026 Global Education Outlook reports that 2025 venture capital into edtech reached $2.4 billion, driven by small- to mid-sized deals where investors deliberately favored AI-enabled, workflow-embedded, and workforce-aligned models. Eight education IPOs reached market in 2025, the most in years. The market is no longer pricing growth at any cost. It is pricing growth that comes with discipline.

That has direct implications for how founders should think about timing. When the bar is durability, the businesses that pre-empt the question, the ones with clean recurring revenue, low churn, embedded use cases, AI-aware product roadmaps, get the premium. The companies that simply show traffic and signups face longer processes. PwC's 2026 TMT M&A outlook puts it bluntly: the next phase of dealmaking will reward integrated AI-enabled platforms over content-volume plays.

Corporate Training and Workforce Upskilling Take Center Stage

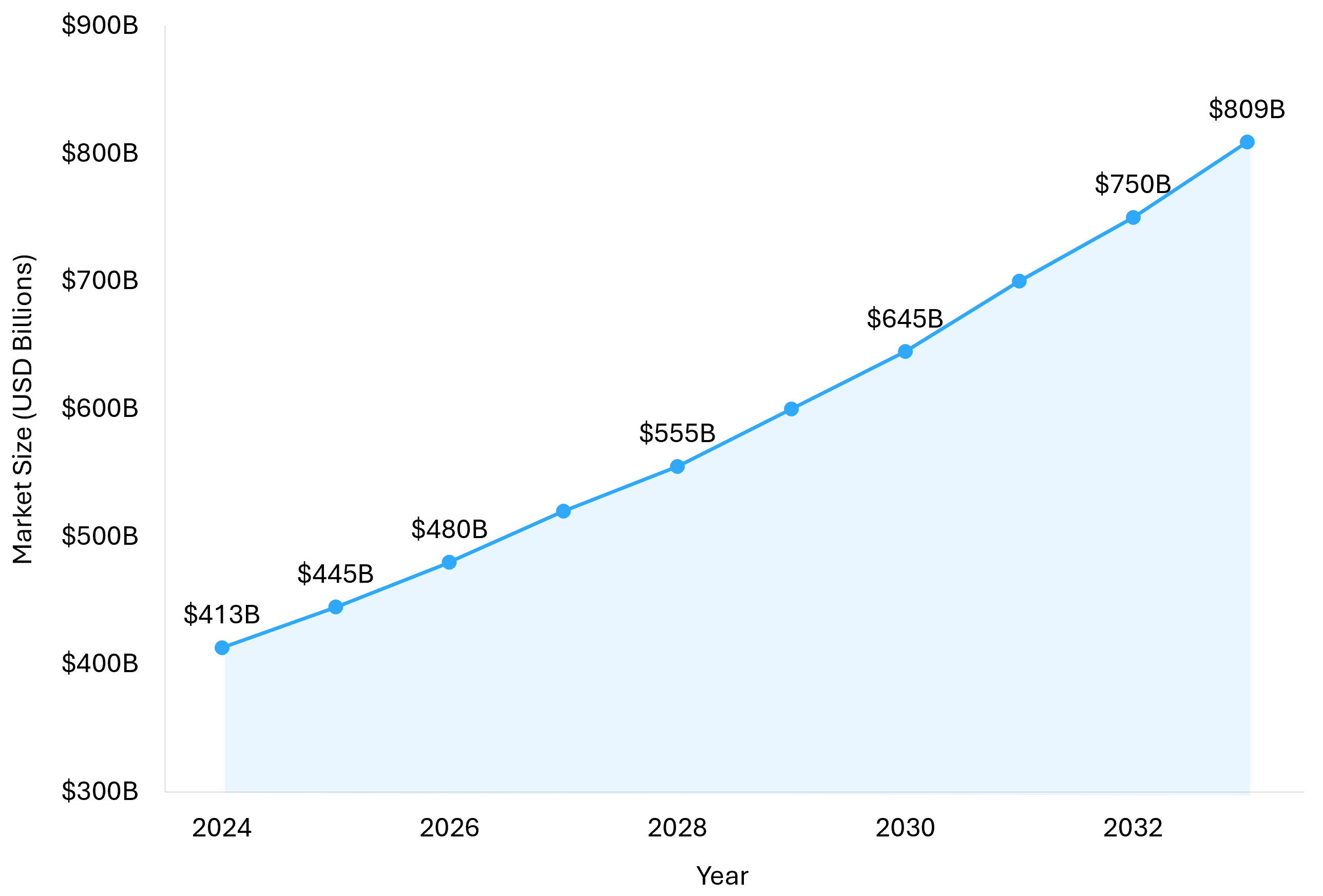

The single largest pool of buyer interest in edtech today sits in corporate training and workforce upskilling, and the macro numbers explain why. The global corporate training market reached $444.86 billion in 2025 and is projected to grow to $808.89 billion by 2033, a compound rate of 7.76%. That trajectory is structural, not cyclical. Employers across every sector are confronting a skills mismatch that they cannot hire out of.

McKinsey's Skills Reset for the AI Age analysis estimates AI-powered agents and robots could generate roughly $2.9 trillion in annual US economic value by 2030, but capturing that depends on how quickly workforces adapt. Demand for AI fluency has grown nearly sevenfold in two years, according to McKinsey research, faster than any other skill category, and this demand is no longer concentrated in technical roles, and it is spreading across management, finance, healthcare, education, and frontline services. The World Economic Forum estimates 59% of the global workforce will need reskilling or upskilling by 2030, roughly 120 million workers.

That demand is being met with capital. Microsoft committed over $4 billion to AI education and training in 2025, funding programs that span schools, community colleges, and its newly formed Elevate Academy. South Korea is investing approximately $740 million from 2024-2026 to train teachers on AI tools. These are not edge cases; they are the new baseline of what governments and employers are prepared to spend.

For founders inside this segment, the M&A implication is the most favorable in years. Strategic acquirers and private equity sponsors are both buying. The Coursera-Udemy combination is the most visible example, but the bulk of activity is happening at the middle and lower middle market, where buyers consolidate specialty training providers into broader platforms. Healthcare training, compliance training, technical certification, and AI fluency programs are commanding the strongest interest. In Q4 2025 alone, HolonIQ noted that workforce training continued to attract the most M&A activity across the sector.

Lower-middle-market businesses below the threshold of bulge-bracket investment banking are particularly well-positioned. For founders of edtech businesses under $1 million in valuation, FE International's marketplace offers a faster, more flexible path to liquidity, with direct access to a curated pool of qualified buyers without committing to a full advisory mandate. For larger deals, FE International's dedicated EdTech advisory practice provides the full sell-side process with global buyer reach and a track record of more than 1,500 transactions across technology sectors.

AI Tutors and AI-Enabled Learning: The Sector Drawing the Loudest Buyer Interest

AI in education is the single fastest-growing vertical within edtech, and its impact on M&A is impossible to overstate. The global AI in education market is calculated at $9.58 billion in 2026 and projected to reach $136.79 billion by 2035, a 34.52% compound annual growth rate. That kind of trajectory pulls in both strategic acquirers wanting to bolt on capability and financial sponsors looking for a defensible category bet.

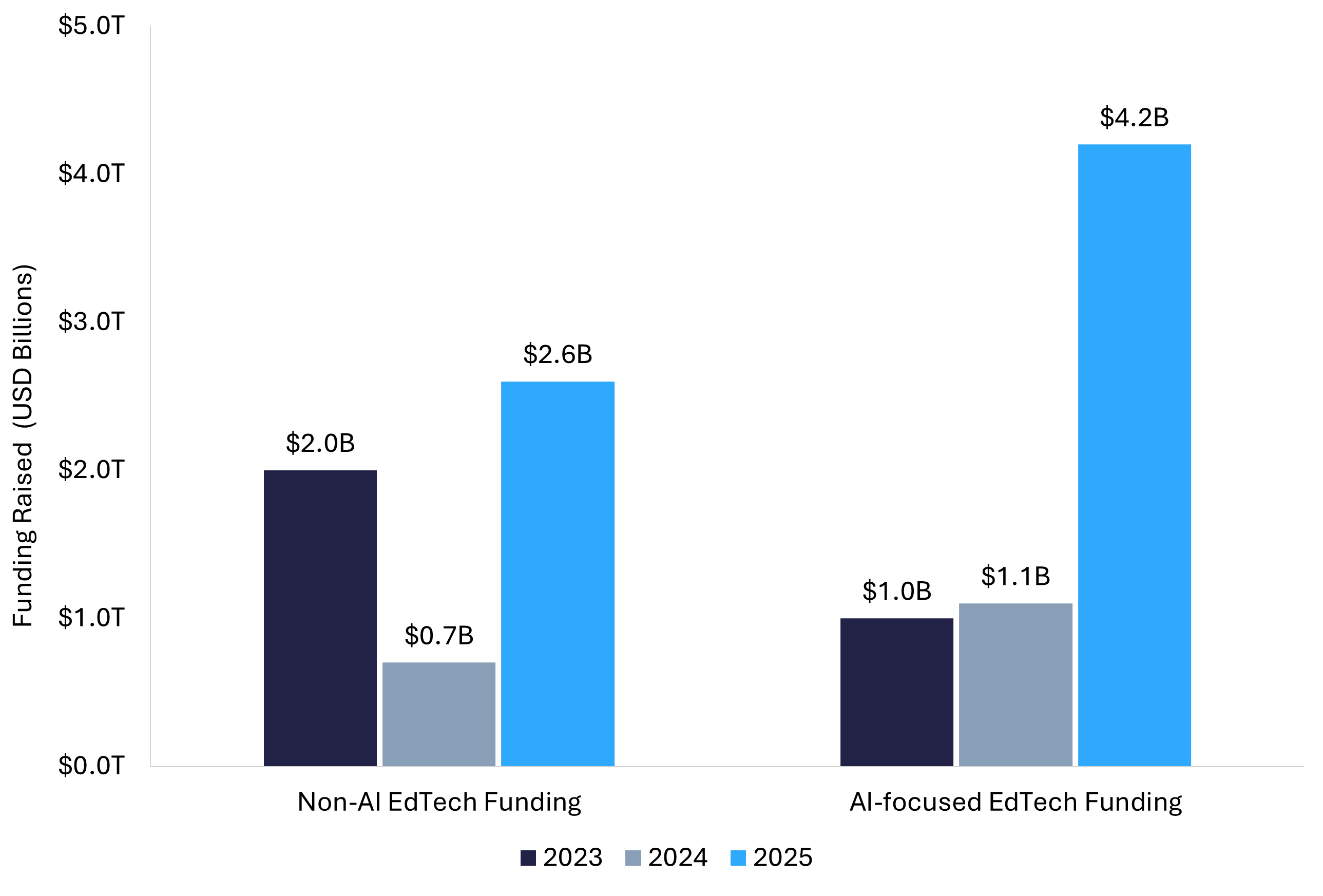

AI-focused education companies raised $4.2 billion in venture capital during 2025, representing 62% of all edtech funding for the year. Language learning has been the single largest sub-vertical, with Preply, Speak, ELSA, Praktika, Univerbal, and Blue Canoe collectively raising over $400 million. Teacher-focused AI tools, including MagicSchool AI, Brisk Teaching, and Curipod, added another $90 million in 2024-2025 alone. The number of active AI-focused education startups crossed 2,800 in 2026, an 18x increase from 2023.

Strategic interest is matching the venture momentum. Khan Academy's Khanmigo AI tutor grew from 68,000 users in 2023-24 to over 1.4 million users by mid-2025. MagicSchool AI reached over six million educator users by October 2025. Each of these platforms is the kind of asset that incumbents and PE-backed roll-ups now actively pursue. The acquirer logic is straightforward: building the same product in-house takes 18 to 24 months and produces inferior distribution.

Within the AI tutoring sub-vertical, the highest interest is concentrated in platforms with verifiable learning outcomes such as randomized controlled trial data, district-level efficacy studies, and retention metrics that hold up under buyer scrutiny. The market is no longer rewarding chatbot wrappers. It is rewarding products that demonstrate measurable improvement in learner persistence and skill acquisition. Bain's data shows one in five strategic dealmakers walked away from a deal in 2025 specifically because of unfavorable AI impact on the target's business, and an equal share have actively pursued AI assets they would not have considered eighteen months earlier.

For founders building inside AI education, the M&A landscape is unusually founder-friendly. Strategic operators want capability. Private equity wants platforms. Public-market players want speed-to-market against incumbents. That three-sided buyer interest creates competitive auctions, which is the most reliable predictor of valuation upside. If you've built proprietary models, owned training data, or distribution into K-12 districts or enterprise L&D, you are sitting inside one of the most actively bid corners of the technology M&A market.

Where Buyer Demand Is Concentrating: Sub-Sectors Attracting Premium Multiples

Not all edtech assets trade at the same multiples. The 2026 environment has sorted the sector into a clear hierarchy. Workflow-embedded enterprise platforms sit at the top. Direct-to-learner consumer products with weak retention sit at the bottom. The chart below summarizes where buyer activity is concentrating across major sub-sectors based on disclosed 2025 deal volume, capital flow, and qualitative buyer-preference signals.

.png)

Workforce Training and Corporate Learning

This is the largest concentration of buyer activity in 2026 and the most varied. Buyers include strategic learning platforms (Coursera, Cornerstone), industry-vertical training specialists in compliance, healthcare, and technical certification, and PE sponsors building roll-ups. Recent regional examples include LEORON Institute's acquisition of UAE-based XpertLearning and GenSpark's acquisition of ProGrad in India, both completed in 2025 and both evidence that regional consolidation is happening alongside global megadeals.

AI Tutoring and Adaptive Learning

Highest growth, deepest funding, and broadest cross-buyer interest. Pure-play AI tutors, AI assessment platforms, and AI-enabled learning software each attracted disproportionate capital in 2025. AI Tutor Platforms posted capital-to-deal-share ratios of 1.28x, among the highest in the entire edtech dataset.

Skills Intelligence, Credentialing, and Career-Aligned Platforms

As employers and institutions push for verifiable outcomes, the assets that translate skills into portable credentials are increasingly valuable. The Coursera-Udemy combination explicitly cites credentials infrastructure as a strategic priority. CTE (career and technical education) is what EdWeek Market Brief calls "a very hot area" of buyer interest in early 2026.

K-12 Digital Curriculum and District-Embedded Platforms

Steady, durable buyer interest. The KKR-Instructure and Bain-PowerSchool take-privates anchored 2024-2025 activity. Strategic buyers now target K-12 platforms that sit inside district workflows like assessment, SIS, communications, and instructional content, because rip-and-replace is operationally painful and renewal economics are predictable.

Notable EdTech and Learning Technology Deals: 2024–2026

The transactions that have defined the current cycle share several traits. They cluster in workforce learning and infrastructure. They feature both sponsors and strategic operators as buyers. They are concentrated in the US and Europe. And they reflect a deliberate shift from chasing user growth to acquiring assets with embedded distribution, recurring revenue, and credible AI roadmaps. The table below summarizes a representative cross-section of the most significant deals from the current cycle.

Three observations cut across these transactions. First, the headline take-privates by KKR, Bain Capital, and the Goldman Sachs AM-led consortium each anchored multi-billion-dollar enterprise values, indicating that scaled platforms with predictable cash flow are commanding sustained premium attention from sponsors. Second, strategic operators (Coursera, Newsela, Echo360, upGrad, LEORON) are using M&A to add specific capabilities, distribution, or geographic reach rather than simply chasing scale. Third, the cycle is global. Major deals span North America, Europe, the Middle East, and South Asia, indicating that cross-border buyer interest is now structural rather than incidental.

For founders thinking about positioning their business, the implication is that there is no single playbook anymore. The buyer most likely to pay the highest multiple for your business depends on which capability gap you fill, which geography you serve, and which sub-vertical you sit inside. Identifying that buyer profile early, then designing the sale process to attract that buyer alongside competitive alternatives, is what separates a market-priced exit from a premium one.

Who's Buying in 2026: Strategic Acquirers, Private Equity, and Strategic Operators

Understanding who is acquiring matters as much as understanding what they're paying. In 2026, three distinct buyer profiles are active across edtech, each with different priorities, deal structures, and post-close playbooks. Founders who go to market with a clear view of which buyer fits best tend to run cleaner processes and capture better outcomes.

Strategic Acquirers

Operating companies , both publicly traded learning platforms and private incumbents, are leading the scope dealmaking trend. strategic M&A in education proved more resilient than financial-sponsor activity in 2025, a reminder that operators have used acquisitions to add capability when organic growth was harder to achieve. Strategics typically pay for revenue synergies, distribution leverage, and time-to-market, and they're willing to outbid sponsors when the asset closes a capability gap. Newsela's acquisition of Generation Genius and Echo360's purchase of GoReact are prototypical 2025 examples, both reinforcing a content-plus-workflow thesis at the operator level.

Private Equity Sponsors

PE remains the most patient capital in the sector, even after a year of slower deployment. Goldman Sachs Asset Management's $2 billion acquisition of Kahoot! and KKR's Instructure take-private represent the high end of sponsor appetite for category-leading platforms with predictable cash flow. Below the headline transactions, sponsors are quietly building roll-ups across corporate training, healthcare education, K-12 curriculum, and CTE. The EdWeek Market Brief 2026 outlook notes that PE firms, which rely on debt to fuel acquisitions, are expected to benefit from a more favorable rate environment in 2026, which should support more activity at the platform and add-on level.

Strategic Operators (PE Portfolio Companies)

A growing share of edtech M&A now happens at the portfolio-company level, with operators backed by sponsors making tactical add-ons. This category has been one of the most active buyer pools for sub-$50 million targets. Examples include Intelvio (Eden Capital portfolio) acquiring the Professional Crisis Management Association, Procare Solutions acquiring Bertelsen Education, and Newsela continuing to expand through bolt-ons. For founders with strong product-market fit but limited scale, strategic operators are often the most aggressive bidders.

A clean process should expose your asset to all three buyer types simultaneously. That is the single most reliable lever for valuation upside, and it is precisely the kind of competitive process that a dedicated EdTech M&A advisory team is built to run.

Valuation Benchmarks for EdTech in 2026

Multiples in 2026 reflect a market that has matured into measurable discipline. The Finro Q4 2025 EdTech valuation dataset, drawn from 271 observations across public, private, and M&A transactions, places the median EV/Revenue multiple at 7.8x and median EV/Funding at 3.8x. Those are healthy numbers by historical standards. They are not pandemic-era inflation, but they are notably above the depressed levels of 2023.

Where the market has changed most is in the dispersion. Two edtech businesses with similar headline revenue can trade at very different multiples depending on retention, workflow embeddedness, and AI-readiness. The chart below shows median EV/Revenue benchmarks across the major edtech business models.

.png)

Three patterns stand out. First, infrastructure and workflow-embedded SaaS commands the highest multiples, anywhere from 8x to 10x revenue at the median, with strong platforms reaching higher. Second, corporate and workforce learning SaaS lands in the high single digits, a reflection of enterprise stickiness and recurring revenue. Third, consumer-facing direct-to-learner businesses trade at materially lower multiples (typically below 5x revenue) because customer acquisition is more expensive and retention is harder to engineer.

Two factors increasingly drive premium pricing within any model. Net revenue retention above 100% materially supports higher EV/Revenue multiples in any SaaS-style edtech business. AI defensibility is the second. Targets that can demonstrate proprietary data, custom model training, or AI-driven product differentiation receive premium attention from both strategic and financial buyers, while businesses that simply layered third-party AI on top of existing products face tougher diligence.

EBITDA multiples for strategic deals reached a median 11.6x EV/EBITDA in 2025 across the broader M&A market, up a turn from the prior year. For edtech specifically, multiples cluster around the broader software median, with premium businesses commanding more on the back of growth, retention, and category position.

How Geography Is Shaping the EdTech M&A Map

North America anchors the global edtech M&A market. HolonIQ reports North America led 2025 EdTech M&A activity, followed by Western Europe. The US remains the largest single deal market by both volume and value, and a deep pool of strategic acquirers operating across K-12 districts, higher education, and corporate L&D continues to drive consistent transaction flow. PowerSchool and Instructure were anchored in the US. So was Coursera-Udemy.

Europe is the surprise outperformer of 2025. HolonIQ notes Europe captured close to half of global VC value, outpacing North America. The UK in particular has emerged as a strong center of strategic and PE activity. According to Shoosmiths' 2026 UK education investment outlook, K-12, SEN (special educational needs), and EdTech across the UK are all attracting growing buyer attention, supported by structural workforce shortages and rising demand for digital learning infrastructure.

Asia is a more complex picture. China continues to operate under regulatory constraints that have reset the consumer K-12 market, but workforce and corporate-facing edtech remains active. India's market has matured into a consolidation phase. Unacademy's share-swap acquisition by upGrad in March 2026 was widely interpreted as a signal that the next phase of India's edtech story will be consolidation rather than expansion. Latin America and the Middle East remain active for buy-and-build strategies, particularly in K-12, vocational, and language learning.

Cross-border activity has been one of the underappreciated stories of 2025-2026. Strategic acquirers are looking outside their home markets to find capability and distribution. For founders of edtech businesses with international revenue, that means buyer interest is increasingly coming from acquirers in geographies different from your own, and a process designed to surface that demand globally is increasingly important.

What This Means for EdTech Founders Looking to Sell

If you're an edtech founder weighing a sale, the 2026 environment offers some of the most favorable conditions in years for well-prepared businesses. Here is what the data above translates into, practically, for sellers.

Buyer Demand Is Real, Plural, and Differentiated

Multiple buyer types , strategic operators, PE sponsors, and portfolio-backed operators, are all actively bidding. The most reliable lever for valuation upside is exposing your asset to all of them. A clean, structured process designed to attract multiple bidder types is the difference between a market price and a premium price.

Preparation Matters More Than Ever

Buyers in 2026 are scrutinizing AI-readiness, retention metrics, and outcome data more carefully than they have at any point in the last five years. Over 75% of strategic acquirers in 2025 assessed AI's impact on the target's business as a core diligence step. Founders who can present a defensible view of how AI shapes their product roadmap, whether you are enabling AI, defending against it, or somewhere in between, close cleaner deals.

Match the Path to the Business

For businesses valued at $1 million or more, a full sell-side advisory process is the right vehicle. FE International's EdTech M&A advisory team has guided founders across the sector through that process, including the eight-figure exit of PositivePsychology.com, an edtech platform used by more than 19 million professionals. For sub-million-dollar businesses, the FE International M&A Platform provides direct access to a curated pool of qualified buyers with self-serve listings and customer success support , designed for founders who want a faster path to liquidity without committing to a full advisory mandate.

Timing Is About Readiness, Not Markets

Founders who try to time the macro often miss the more important variable, which is internal readiness. The right time to sell is when your retention is healthy, your AI story is coherent, your financials are clean, and a multi-bidder process is achievable. The 2026 market is rewarding that level of preparation with multiples that justify the work.

Positioning Your EdTech Business for a Premium Exit in 2026

The 2026 edtech M&A market is unusual in how broadly it is rewarding well-prepared sellers. Strategic acquirers are actively building. Private equity sponsors are deploying. AI is reshaping every category, and buyers want exposure. Workforce upskilling is structurally undersupplied for the next decade. Each of those vectors creates a path to liquidity for the founders who run their process right.

If you're starting to think about a sale, the most valuable first step is a confidential, data-backed valuation of where your business stands today. FE International has guided founders across SaaS, AI, ecommerce, fintech, cybersecurity, agency, and edtech businesses through more than 1,500 successful transactions, with a 94.1% sales success rate and a global pool of strategic, financial, and operator buyers.

Whether your business sits comfortably inside the marketplace tier or is a candidate for a full sell-side advisory process, the right starting point is the same. Request a free, no-obligation valuation today and our team will assess your business against current edtech M&A benchmarks, identify the most likely buyer profile, and help you understand exactly what your business is worth in the 2026 market. For founders of edtech businesses below $1 million ready to explore listing directly, you can also browse the FE International M&A Platform to see live demand and start a conversation with qualified buyers.

Markets reward founders who prepare. The 2026 edtech M&A environment is one of the strongest in years for the right business at the right time. The work starts with understanding where you stand.