Global M&A deal value rose 40% in 2025 to $4.9 trillion, and 80% of M&A executives surveyed expect to sustain or increase deal activity in 2026. Global buyout deal value alone climbed 44% to $904 billion, while 90% of PE and 80% of corporate dealmakers anticipate doing even more deals this year. The buyer landscape for SaaS companies has never been more active, or more complex.

If you are a SaaS founder or business owner weighing an exit, the question is not simply whether to sell. It is who to sell to, and how that choice shapes everything from your final valuation to whether your team stays intact after the deal closes. The three primary buyer types, private equity firms, strategic acquirers, and individual buyers, each bring fundamentally different priorities, deal structures, and valuation approaches to the table. A private equity buyout looks nothing like a strategic merger, and both differ from an individual acquisition.

This guide breaks down those differences with real 2026 data, comparison tables, and practical frameworks. Whether your SaaS generates $1M or $100M in annual revenue, understanding the key differences between financial and strategic buyers (and where individual buyers fit) will help you make a decision that aligns with both your financial goals and personal priorities. For businesses under $1M in annual revenue, the FE International Marketplace offers a streamlined, self-serve path to connect with curated, qualified buyers. For larger transactions, FE International's full advisory service, backed by a 94.1% success rate across 1,500+ completed deals, creates the competitive tension between buyer types that consistently produces better outcomes.

Understanding the Three SaaS Buyer Types

Before comparing specifics, it helps to understand what motivates each buyer type at a fundamental level. Their priorities differ sharply, and those differences ripple through every stage of a transaction. A SaaS company worth $20M in standalone terms could be worth $28M to a strategic buyer with clear synergies and $18M to a PE firm running conservative LBO math. The buyer you sell to is, in many cases, the single largest variable in your exit outcome.

Private Equity Buyers: Returns-Driven Financial Acquirers

PE firms evaluate SaaS businesses primarily on standalone financial performance. They model debt service, entry multiples, and exit targets, then back into a price that generates the fund's target IRR (typically 20-25%+). PE platforms typically pay 4-6x revenue for profitable, stable SaaS businesses with a clear path to 7-10x exit through growth and margin improvement. Add-on acquisitions (bolt-ons to an existing portfolio company) come in lower at 3-5x, reflecting the buyer's leverage in a non-competitive, relationship-driven transaction.

The appeal for founders is the "second bite of the apple." PE deals typically involve taking 60-80% cash off the table while retaining 20-40% rollover equity. You stay involved as CEO or in a senior role, the PE firm injects operational expertise and acquisition capital, and when the combined platform sells again in 3-5 years, your retained equity can be worth more than the first payout. This is particularly compelling for founders who believe significant upside remains but want to de-risk now.

The Bain Global Private Equity Report 2026 describes PE as entering a mature phase where "12 is the new 5," meaning today's deals demand faster EBITDA growth to generate returns. The buyout industry still holds $1.3 trillion in dry powder, and GPs face increasing pressure from LPs to deploy before investment periods expire. That means more competition for quality SaaS assets, and stronger offers for well-prepared sellers. Interest rate stability in 2026 has also improved LBO economics, making leverage more accessible and expanding the range of deals PE can underwrite profitably.

Strategic Acquirers: Synergy-Driven Buyers

Strategic buyers are other software companies (often larger) acquiring your business to expand product offerings, fill capability gaps, enter new markets, or acquire your customer base. The critical difference: strategics evaluate what your business is worth inside their ecosystem, not just its standalone value. Revenue acceleration, customer access, product integration, and competitive blocking all factor into their willingness to pay. That logic does not appear in a DCF model, but it absolutely shows up in the offer.

Announced cost synergies as a percentage of the target's cost base in 2024-2025 significantly exceeded the historical average of roughly 16%. TMT now represents nearly a third of all US M&A value, underscoring tech's outsized role in driving corporate growth. Strategic buyers are racing to secure control over AI models, data, and infrastructure, creating a bifurcated market where AI-based solutions command premium valuations. When IBM acquired Confluent for $11B in March 2026 at a 34% premium, the deal had nothing to do with leveraged buyout math. IBM was buying real-time data infrastructure that enterprise AI systems depend on. For SaaS transactions in the $1M-$100M range, the absolute numbers are smaller, but the principle is identical.

Individual Buyers: Operator-Entrepreneurs and Search Funds

Individual buyers include high-net-worth entrepreneurs, search fund operators, and independent acquirers. A search fund model works like this: an aspiring operator raises capital from a group of investors, then spends 1-2 years searching for and acquiring a single privately held company to run. After the sale, the searcher steps in as CEO and operates the business for several years, with the ultimate goal of growing it and selling again. Search funds are most active in the $1M-$10M deal range and gravitate toward profitable, owner-operated SaaS businesses with recurring revenue and low churn.

Individual buyers offer advantages that larger buyers cannot: faster decisions, creative deal structures, and willingness to consider smaller companies below PE firm minimums. They can also be better stewards of legacy: if you built something you care about, an individual operator who plans to run it for 5-10 years may preserve your company culture and team better than a strategic that plans to integrate and absorb. The trade-off is limited capital. Deal sizes are typically under $5M, seller financing is common, and individual buyers may lack the resources to scale aggressively. For SaaS businesses valued under $1M, the FE International Marketplace is purpose-built for this segment: self-serve listings, curated buyer access, customer success support, and a structured offer process that eliminates tire-kickers.

How Each Buyer Type Values Your SaaS Business

Valuation is where buyer motivations diverge most sharply. The same SaaS company can command materially different offers depending on who is across the table, and that divergence is not a few percentage points. We regularly see 30-50% spreads between the highest and lowest qualified offers on the same business.

PE firms run LBO math: entry multiples, leverage capacity, operational improvements, and a target exit in 3-5 years. For lower-middle-market SaaS businesses ($5M-$50M enterprise value), current PE multiples sit at 4-5x EV/Revenue for companies with solid retention and profitability. Bootstrapped companies at the smaller end ($5M-$10M EV) see 3-4x, while the $25M-$50M tier can reach 5-7x when both PE and strategic interest creates pricing tension. The buyer universe matters as much as the financial profile: a structured competitive process is the mechanism for discovering where the real ceiling sits.

Strategic acquirers layer synergy value on top of standalone performance. BCG research shows sellers collect, on average, 31% of the capitalized value of expected synergies through the purchase premium. This is why a strategic acquirer versus a private equity firm will often produce different numbers for the same target. The synergy premium can come from multiple sources: revenue synergies (cross-selling your product into the acquirer's customer base), cost synergies (eliminating duplicate infrastructure, sales teams, or administrative functions), and capability synergies (acquiring technology or talent that would take years to build internally). In AI-driven deals, the capability premium is often the largest component.

Individual buyers work with the most constrained valuation framework, typically 2-4x SDE (seller discretionary earnings). SDE includes the owner's salary and discretionary expenses added back to net profit, giving a clearer picture of true cash flow available to a new owner. For businesses valued under $5M, this is the standard metric buyers use. A SaaS generating $200K in annual SDE at a 3x multiple would be valued at $600K. The multiple depends on growth trajectory, churn rate, customer concentration, and how passive the business is to operate. For founders selling a smaller SaaS, the FE International Marketplace connects you with qualified individual buyers actively seeking profitable, lower-ticket acquisitions. The marketplace's verified metrics and structured offers give both sides confidence in the valuation.

.png)

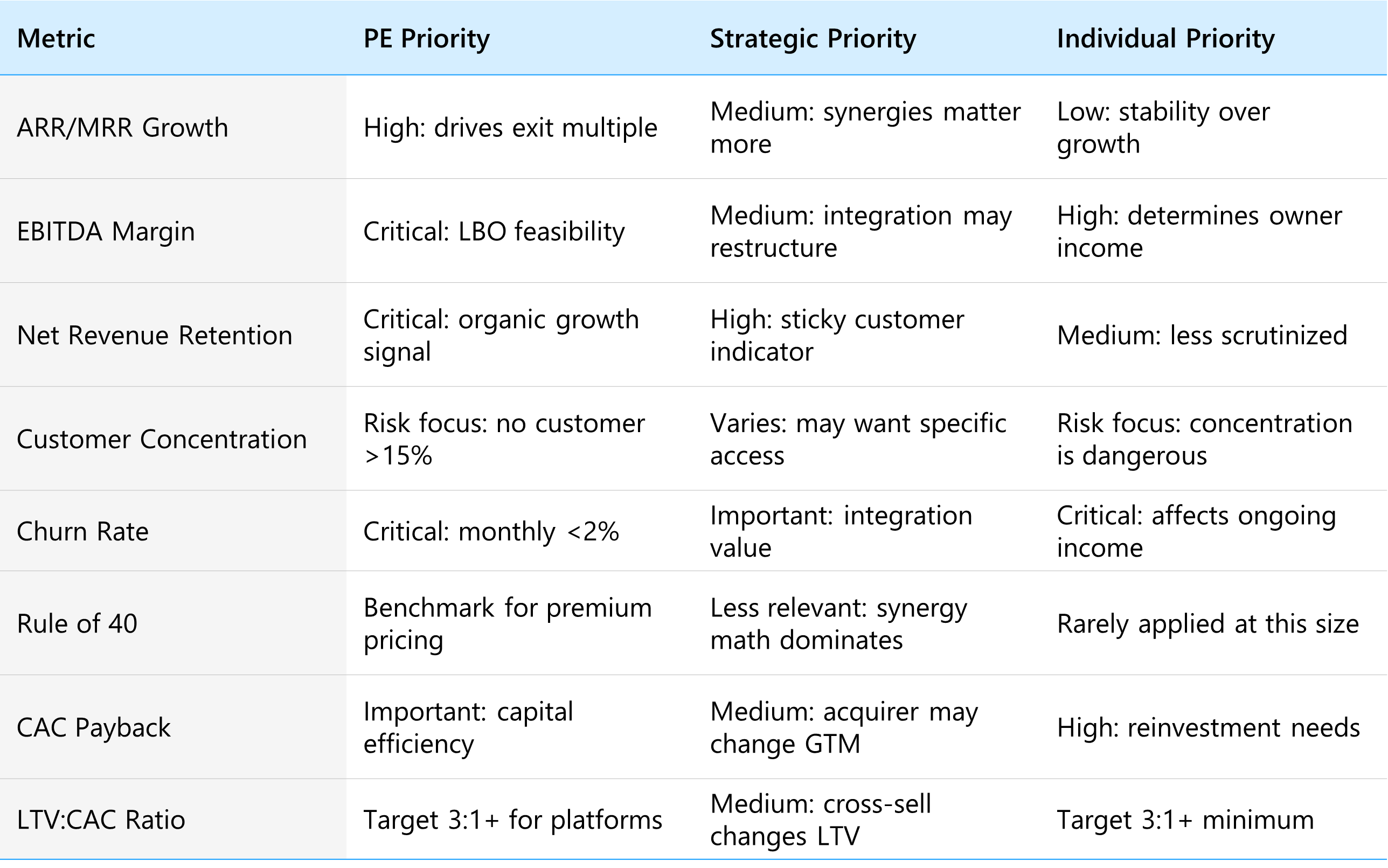

The Metrics Each Buyer Type Prioritizes

All three buyer types care about your SaaS metrics, but the weight they assign varies. Understanding these priorities helps you position your business correctly and prepare the right data for each audience.

PE buyers zero in on EBITDA margin and NRR because those metrics determine the reliability of the returns model. Strategic buyers often de-weight profitability if the product fills a critical capability gap. Individual buyers focus on cash flow and operational simplicity. A quality of earnings (QoE) report is a critical part of due diligence for all buyer types, but especially PE. Getting a sell-side QoE prepared before going to market can accelerate diligence and reduce retrade risk. FE International's pre-listing due diligence process addresses many of these issues before a business goes to market, which is one reason 94.1% of FE-listed businesses close successfully.

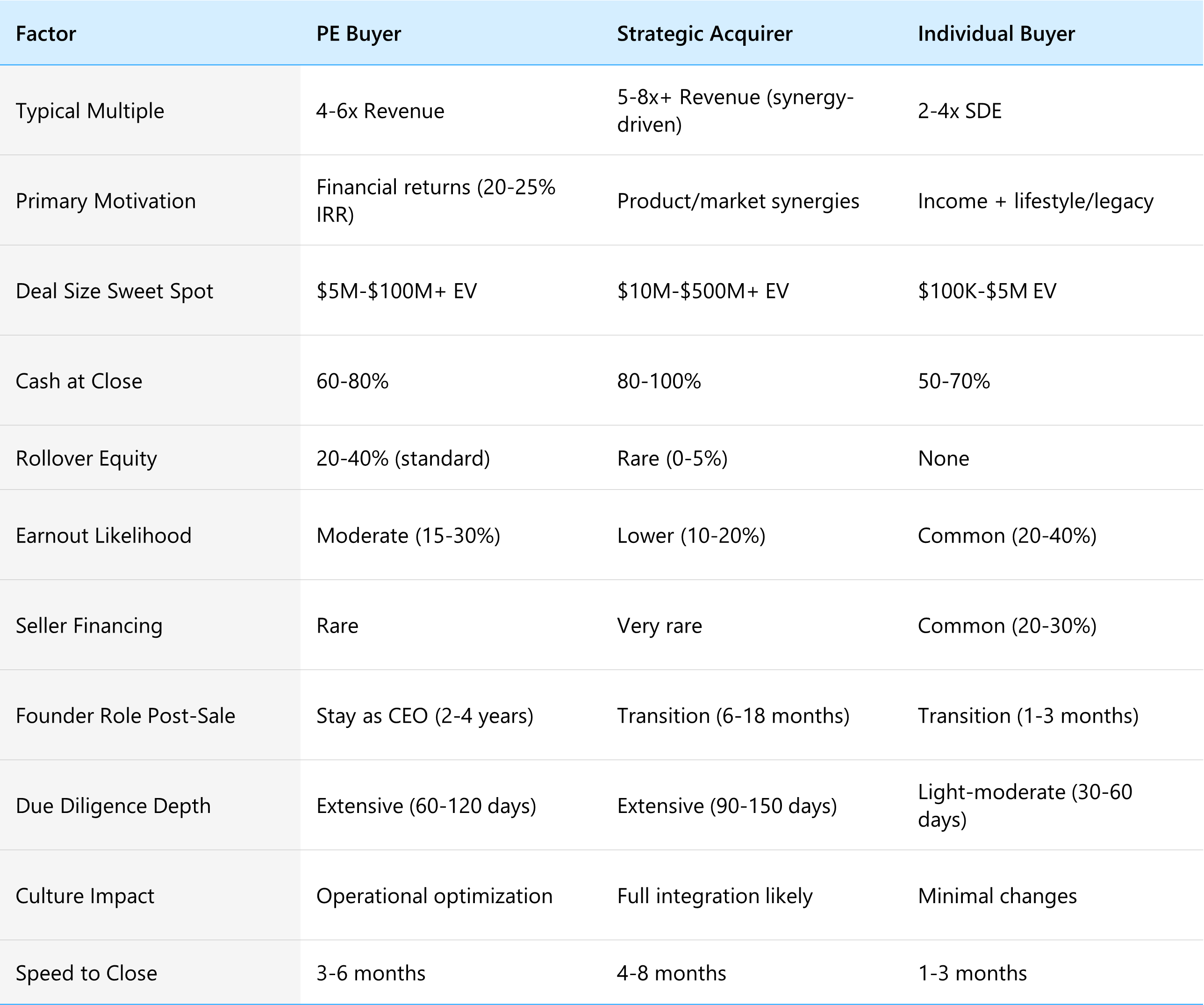

PE vs. Strategic Buyer vs. Individual Buyer: Side-by-Side Comparison

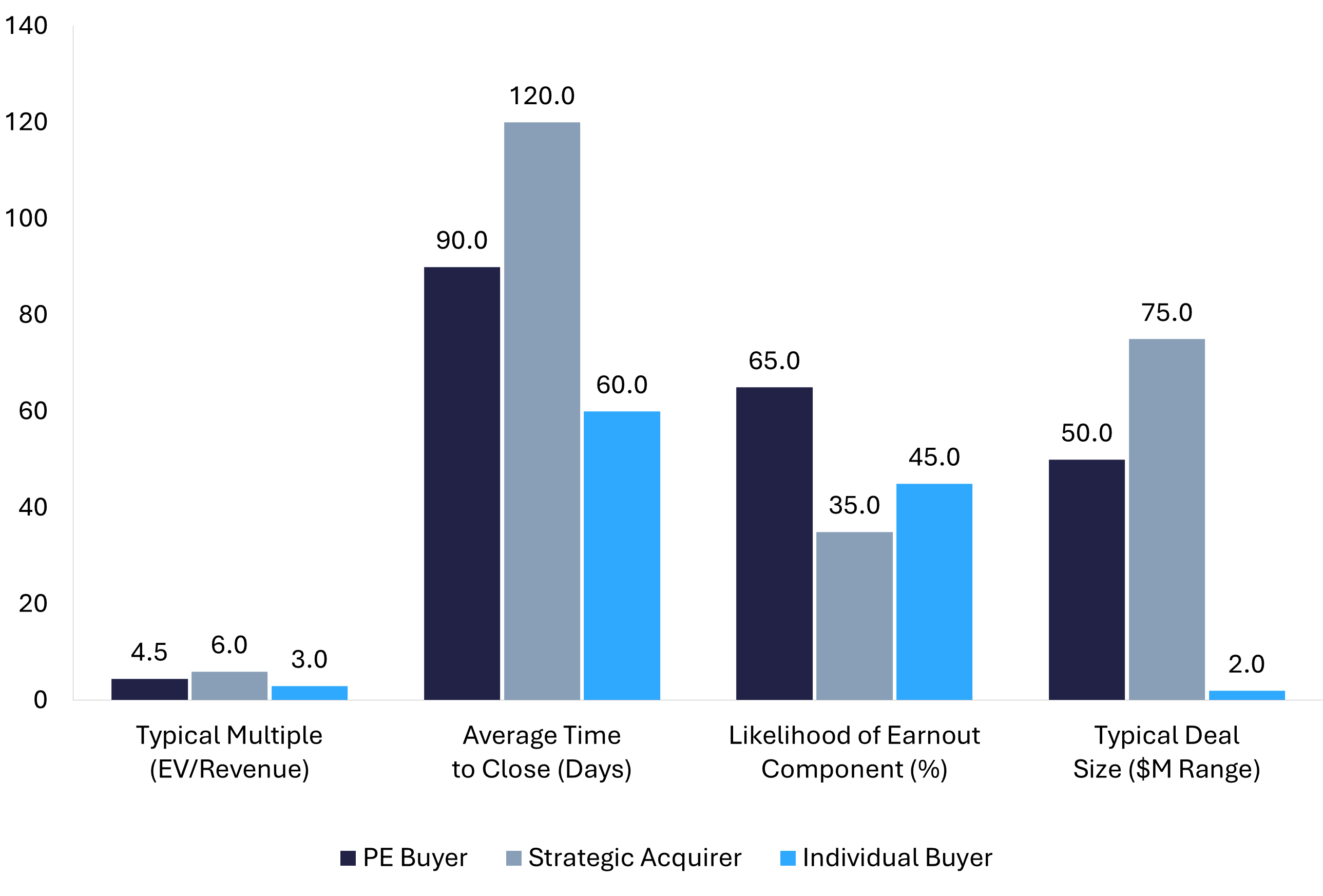

Deal Structure: PE LBO vs. Strategic All-Cash vs. Seller-Financed Acquisition

A $30M offer with 30% in earnouts tied to aggressive ARR targets is a fundamentally different deal than a $25M offer that is mostly cash. The headline number matters less than the structure, and structure is where the pros and cons of selling to a PE firm vs. a strategic acquirer vs. an individual buyer diverge most.

PE deal structures (LBO model) typically include 60-80% cash at close, 20-40% rollover equity, and occasionally a modest earnout. The rollover aligns you with the PE firm's growth plan and gives you upside in the next exit. PE firms also use working capital adjustments, escrow holdbacks (typically 5-10% for 12-18 months), and representations and warranties (R&W) insurance to manage risk. R&W insurance has become standard in PE-backed deals: it shifts much of the indemnification risk from seller to an insurance policy. In practice, this means less of your sale proceeds get locked in escrow and more clean cash arrives at close. Negotiations around working capital targets, indemnification caps, and basket thresholds are where PE deals get complicated. The difference between a well-negotiated and poorly-negotiated PE deal can easily swing your net proceeds by $1M-$3M on a $20M transaction. Interest rate stability in 2026 has improved LBO economics considerably: PE firms can model debt service with more confidence, expanding the range of deals they can underwrite. As the Bain 2026 Global PE Report notes, deal and exit values surged to their second-highest levels on record in 2025, and the outlook for 2026 remains favorable.

Strategic deal structures typically offer the cleanest terms: 80-100% cash at close, minimal or no rollover, shorter transition periods. When synergies are clear and the buyer has confidence in integration, they pay a premium for simplicity. The trade-off: your product and team may get absorbed into the acquirer's platform. For founders who want a clean break at a premium price, this is often the right path.

Individual buyer structures and seller financing terms lean heavily on deferred consideration. Cash at close is typically 50-70%. The remainder is structured as seller notes (paid monthly over 2-4 years at 5-8% interest) or performance-based earnouts. Seller financing makes you the bank: you are lending the buyer money to buy your business. If the new owner cannot maintain performance, your deferred payments may not materialize. For sub-$1M SaaS businesses, the FE International Marketplace's structured offer system helps standardize terms and reduce friction.

.png)

Company Culture, Legacy Preservation, and Employee Retention After the Sale

For many founders, the sale is not purely financial. You built something, hired people who trust you, and care about what happens next. The buyer type you choose has a direct impact on whether your company culture survives, whether your employees keep their jobs, and whether the legacy you built continues.

PE buyers generally keep the existing team in place, at least initially. Their returns depend on operational execution, and replacing people who know the business creates unnecessary risk. Founders typically stay on as CEO for 2-4 years. PE firms will optimize for margin: redundant roles get eliminated, compensation structures shift toward performance-based models, the pace often accelerates. On the positive side, PE investment often brings career growth: your top people get board-level exposure and a broader professional network.

Strategic acquirers present the most uncertainty for employees. Full integration means your team may be absorbed into the acquirer's org chart, reporting lines change, duplicate functions get consolidated. Company culture as you built it is unlikely to survive intact. The best way to protect employees is to negotiate retention packages and employment commitments as part of the deal terms, before signing. Specific protections to negotiate include: guaranteed employment periods for key team members (typically 12-24 months), retention bonuses tied to staying through the integration period, severance packages for any positions eliminated within the first year, and commitments about office location and remote work policies. Some strategic buyers are better stewards of acquired teams than others: those with a track record of preserving acquired products and teams are worth prioritizing, and your advisor should have this intelligence.

Individual buyers are often the best option for legacy preservation when selling a family business or founder-built SaaS. An individual operator who plans to run the business for 5-10 years has every incentive to maintain the team, culture, and customer relationships. Changes tend to be gradual rather than top-down restructuring. If keeping your team employed and your product alive is a top priority, this buyer type deserves serious consideration, even if the multiple is lower.

Common Mistakes Sellers Make With Each Buyer Type

With PE buyers: the most common mistake is optimizing exclusively for financial sponsor logic while ignoring the strategic buyer universe. The right question is not just "what would a PE firm pay?" but also "who has a capability gap my product fills?" Running both tracks simultaneously creates pricing tension. A second PE mistake: undervaluing the rollover equity negotiation. Governance terms and waterfall structures can be worth more than the cash-at-close difference between two offers.

With strategic acquirers: the biggest trap is approaching a sale without understanding the buyer's integration playbook. Some strategics acquire to absorb. Others keep your product running independently while cross-selling. The difference affects your team's continuity, your brand's survival, and the price. A second mistake: waiting for a strategic to approach you. The most valuable strategic deals come from a proactive process that identifies capability gaps across 10-20 potential acquirers simultaneously.

With individual buyers: sellers often agree to earnout structures without sufficient protections. Without clear performance benchmarks, dispute resolution mechanisms, and reporting requirements in the purchase agreement, disputes are common. For sub-$1M deals, the FE International Marketplace mitigates these risks through its structured framework.

The 2026 Capital Environment: Record Dry Powder and Returning Strategics

Three converging forces are creating a favorable backdrop for SaaS sellers. First, PE dry powder. The buyout industry holds $1.3 trillion in dry powder, and total private capital dry powder reached $4.63 trillion at the end of Q2 2025. Roughly 50% of that capital sits in funds two to five years old, meaning the pressure to deploy is real and growing. The McKinsey Global Private Markets Report 2026 describes PE as entering a mature phase where outcomes depend on operational value creation and AI integration rather than leveraged multiple expansion alone.

Second, strategic buyers came back at scale. Global M&A deal value rose 40% to $4.9 trillion in 2025, and the Bain M&A Report notes that almost half of all technology deals already have an AI angle. PwC's tech M&A outlook notes that TMT represents nearly a third of all US M&A value, with strategic buyers racing to secure AI capabilities and cloud infrastructure. Deloitte's 2026 M&A Trends Survey found that 90% of PE and 80% of corporate dealmakers expect an increased number of deals in 2026.

Third, vertical SaaS is commanding premium attention. Both PE and strategics are competing for niche software platforms with embedded workflows and high switching costs. Vertical SaaS accounted for roughly 46% of all SaaS M&A activity in 2025, up from 40% the prior year, and the trend is accelerating. PE firms want these assets because they offer defensible moats, high switching costs, and strong net retention. Strategics want them because vertical specialization is nearly impossible to replicate internally. More buyers competing for fewer quality assets means well-prepared businesses attract multiple competitive offers. This is exactly the environment where a structured advisory process delivers the most value.

%20Ecommerce%20Market%20Size.png)

How to Choose the Right Buyer Type for Your SaaS Exit

Choose PE if: you want significant cash now while retaining upside through rollover equity. You are willing to stay involved for 2-4 years. Your business has $5M+ EV, strong margins, and add-on or operational improvement potential.

Choose a strategic acquirer if: you want maximum cash at close and a clean exit. Your product fills a capability gap in a larger ecosystem. You are comfortable with integration. Your technology or AI capabilities match what strategic buyers are actively hunting for.

Choose an individual buyer if: your SaaS is smaller (under $5M), profitable, and relatively passive. Legacy preservation matters. You are comfortable with some seller financing. The FE International Marketplace is designed for this scenario.

The strongest outcomes come from a process that includes multiple buyer types competing simultaneously. When PE pricing competes against strategic synergy pricing, both offers move higher. This is a core principle behind how FE International structures its advisory engagements: running a competitive process across financial and strategic buyers. With 1,500+ transactions, a 94.1% success rate, and 50,000+ pre-qualified buyers globally, FE creates pricing tension that solo founders cannot replicate.

SaaS M&A Buyer Mix: How the Landscape Is Shifting

PE involvement in SaaS transactions has grown steadily, reaching roughly 58% of all SaaS deals in 2025. But buyers with any strategic angle, regardless of financial backing, comprised approximately 92% of transactions, meaning strategic outcomes drive most M&A volume even when PE is the backer. Strategic buyers staged a major comeback in late 2025, driven by the AI imperative: corporate development teams have a focused mandate to acquire AI capabilities and vertical workflow automation.

Individual buyers and search funds remain most active at the lower end (sub-$5M) but their total share has compressed as PE and strategics push further into the lower middle market. For sellers in this segment, the FE International Marketplace ensures you are not competing for buyer attention against institutionally marketed larger deals.

.png)

Why the Right Advisor Changes Your Outcome

Businesses represented by experienced M&A advisors sell for higher prices and are significantly more likely to close. PE firms do not browse listing websites for deals: they rely on trusted intermediaries. The most valuable strategic deals come from proactive outreach to 10-20 potential acquirers, not reactive responses to a single inbound inquiry.

FE International's advisory model is built specifically for technology businesses: over 1,500 completed transactions since 2010, combined deal value exceeding $50 billion, and a 94.1% success rate. That rate comes from rigorous process: pre-listing due diligence (FE turns down 90% of inquiring businesses to ensure quality), confidential marketing to 50,000+ vetted buyers, structured competitive bidding across all buyer types, and in-house legal support from LOI through closing. The confidentiality piece matters more than most founders realize. A poorly managed sale process can leak information to competitors, unsettle employees, and spook customers. FE's approach protects sensitive business information through NDA-gated buyer access and controlled information disclosure that only reveals details to pre-qualified, serious acquirers.

For larger SaaS businesses ($1M-$100M+), FE's full advisory service creates multi-buyer competitive tension. For smaller businesses (under $1M), the FE International Marketplace provides a professional, lighter-touch path: self-serve listings, curated buyer access, customer success support, and the credibility of FE's brand.

Preparing Your SaaS for Any Buyer Type: The 12-18 Month Playbook

Regardless of which buyer ultimately acquires your business, the preparation is largely the same. Founders who begin exit readiness 12-18 months before a process consistently achieve better outcomes.

Clean, auditable financials. Every buyer type scrutinizes your numbers. Track ARR, MRR, churn, CAC, LTV, gross margin, and NRR with analytics tools like Baremetrics or ChartMogul, not just spreadsheets. Consider getting a sell-side quality of earnings report prepared before going to market: this independent financial analysis verifies your reported earnings are real, sustainable, and properly categorized. It identifies add-backs, one-time expenses, and adjustments to normalized EBITDA. Getting the QoE done proactively accelerates diligence and reduces the risk of a retrade, where the buyer lowers their offer after discovering discrepancies. PE firms and strategics expect sophisticated reporting including deferred revenue, revenue recognition, and cohort analysis. Even individual buyers through the marketplace make faster, cleaner offers when the data is clear.

Reduce founder dependency. A business that cannot operate without you is worth less to every buyer type. Outsource tasks, document processes, build a small team that can maintain the product and serve customers independently. If your marketing uses personal branding, phase it out early. A stand-alone brand is far more attractive to every buyer type. FE International's guide to making your SaaS attractive for acquisition covers this in depth, including payment processor transferability, email list development, and code documentation standards.

Optimize the metrics that drive multiples. NRR above 110% signals organic expansion. Gross margins above 75% indicate scalability. Rule of 40 performance (revenue growth rate + EBITDA margin at or above 40%) separates premium valuations from average ones. LTV:CAC ratios of 3:1 or higher demonstrate efficient customer acquisition. Monthly churn below 2% signals strong product-market fit. For a deep dive on each of these metrics and how they impact what buyers will pay, see FE International's SaaS valuations guide.

Understand your positioning across buyer types. The same company can be positioned differently. A vertical SaaS platform might appeal to PE as a platform with add-on potential, while a strategic might value it for customer access and data. Working with an advisor who tests both framings simultaneously is the most reliable path to the highest-value outcome.

Matching Your Exit to the Right Buyer

The PE vs. strategic buyer vs. individual buyer decision shapes your valuation, deal structure, involvement after the sale, your team's future, and the legacy of what you built. In 2026, with PE dry powder at record levels, strategic acquirers surging back, and a deep pool of individual buyers for smaller assets, the opportunity set for SaaS sellers is as strong as it has been in years.

If your SaaS generates under $1M in revenue, list on the FE International Marketplace to connect with qualified buyers today. If your business is in the $1M-$100M+ range, request a free valuation from FE International. With 1,500+ transactions, $50B+ in combined deal value, and a 94.1% success rate, FE International has the track record, the buyer network, and the process to find the right buyer at the right price.