The numbers tell a striking story. Global M&A deal value hit a record $4.9 trillion in 2025, surpassing the previous high set in 2021, with technology transactions driving more than a quarter of all mega-deal activity. Artificial intelligence was the single biggest catalyst behind that surge. Nearly half of all technology deals in 2025 carried an AI component, up from roughly one in four just a year earlier. And the pace is accelerating: private AI companies raised over $226 billion in Q1 2026 alone, surpassing the full-year 2025 total in a single quarter.

For AI founders, this is not just a headline about big-tech mega-deals. The same capital flows, strategic urgency, and premium valuations are reshaping how mid-market and lower mid-market AI businesses change hands. Acquirers of every size, from Fortune 500 corporate development teams to growth-focused private equity firms, are paying multiples for AI-native companies that would have seemed unreasonable just 18 months ago. And they are paying those premiums because the alternative, building comparable AI capabilities from scratch, costs more and takes longer than buying them.

The Stanford AI Index for 2025 put total corporate AI investment at $252.3 billion in 2024, with private investment jumping 44.5% year-over-year and M&A in the space rising 12.1%. US private AI investment alone reached $109.1 billion, nearly 12 times China's and 24 times the UK's. That gap underscores both the scale of the opportunity for US-based AI founders and the depth of the acquirer pool available to them.

This guide examines the AI M&A trends 2026 that matter most for founders, operators, and acquirers in the technology space. We break down where capital is flowing, what drives the valuation premium for AI-native businesses, how deal structures are evolving, and what sellers should know about positioning their companies for a successful exit. Whether you are running a $500K ARR AI tool listed on a technology marketplace or a $10M ARR vertical AI platform working with an experienced M&A advisory team, the dynamics covered here will directly shape your next move.

Record Capital Is Flowing Into AI Acquisitions

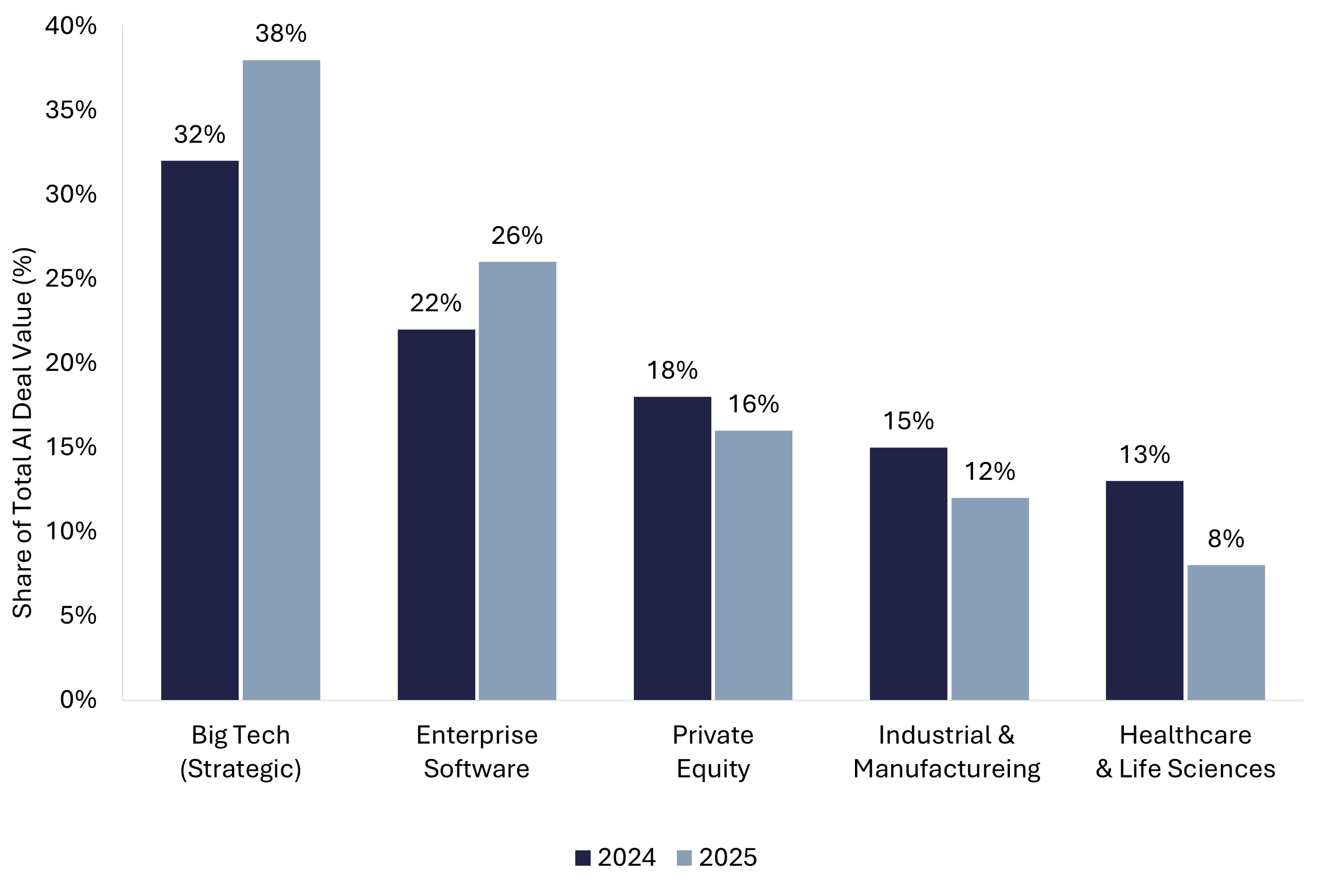

2025 was the strongest year for global deal-making since the pandemic-era boom, and AI was the primary engine. Total deal value reached an estimated $4.9 trillion across more than 50,800 transactions, with mega-deals (transactions above $5 billion) representing roughly 57% of all value. Technology M&A alone jumped 77% year-over-year, reaching approximately $1.08 trillion in total deal value, a pace the sector had not seen in years.

The concentration of capital in AI-related targets is especially notable. Almost half of all strategic technology deal value for transactions above $500 million came from AI-native companies or deals that explicitly cited AI benefits. That figure was closer to 25% in 2024, meaning the share effectively doubled in a single year. The Morrison Foerster Tech M&A Survey found that 57% of technology deal-makers expect deal counts to increase further over the next 12 months, with AI capabilities cited as the top acquisition priority.

Early 2026 data confirms the trend is intensifying, not cooling. CB Insights reported 266 AI M&A deals closed in Q1 2026, a 90% increase year-over-year. In Q2 2025, AI M&A had already hit a quarterly record of 177 deals, roughly double the quarterly average since 2020. The deal funnel is wider, the checks are larger, and the acquirer pool is more diverse than at any point in the AI era.

What does this mean for business owners? The market for AI-native companies has more active buyers, more available capital, and more competitive deal processes than most founders realize. The conditions for sellers have rarely been stronger.

Some context helps: the EY-Parthenon Deal Barometer projects total US deal volume to continue growing through 2026, with corporate M&A deals expected to rise 3% following a 10% increase in 2025, and PE volume increasing 5%. The share of transactions exceeding $1 billion now accounts for 27% of deal activity, up from a 22% average between 2016 and 2019. Technology, financial services, and life sciences are the sectors driving the largest deals, and within technology, AI is the dominant theme. This is not a single-quarter spike. It is a multi-year structural shift in how capital flows through the technology M&A market.

.png)

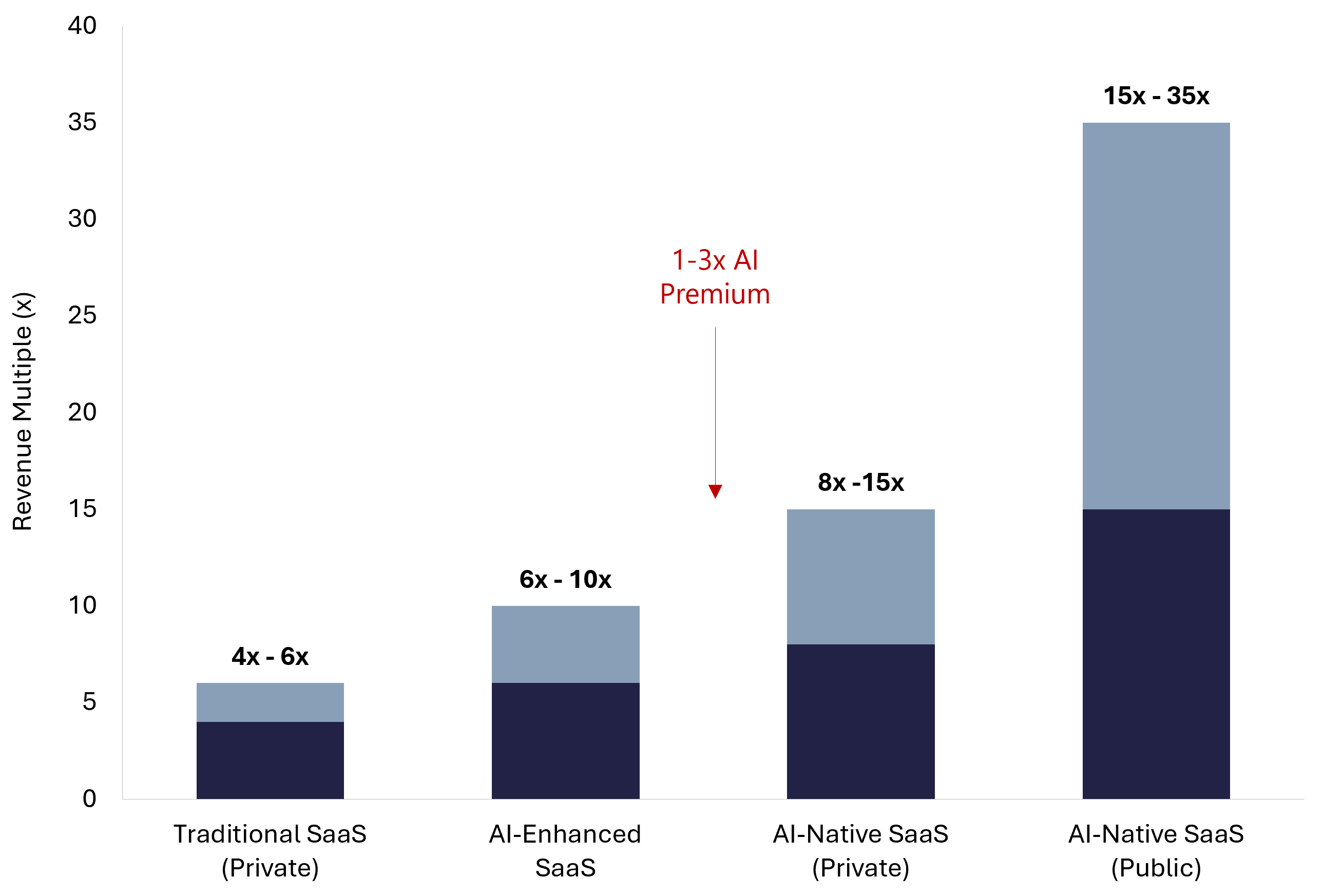

The AI Valuation Premium Is Real, Measurable, and Growing

One of the most significant AI M&A trends 2026 is the measurable premium that AI-native businesses command over their non-AI peers. This is not speculation or hype. The data across both public and private markets shows a consistent, widening gap.

In public markets, AI-native SaaS companies are trading at 15x to 35x forward revenue, with the highest-growth names exceeding those ranges. Private AI deals are closing at 8x to 15x revenue for well-positioned companies, with outliers stretching well beyond that for businesses with proprietary models, defensible data assets, and strong retention metrics. By comparison, traditional SaaS companies in the private market are trading at 4x to 6x revenue, depending on growth rate and profitability. That translates to a 1x to 3x multiple premium for AI-native companies over otherwise comparable non-AI peers.

The premium is not uniform. It varies significantly based on what we see as four key factors: the quality and defensibility of the company's data assets, the degree to which AI is embedded in the core product (not bolted on), net revenue retention rates above 120%, and gross margins that account for inference costs without eroding unit economics. Buyers in 2026 are sophisticated about distinguishing companies that genuinely create AI-driven value from those that have added an AI feature to an otherwise conventional product.

For founders considering a sale, the practical takeaway is that understanding how to value an AI business requires going beyond traditional SaaS metrics. Revenue multiples tell part of the story, but the premium increasingly comes from intellectual property, data moats, and the operational proof that AI is driving measurable customer outcomes.

What Strategic Acquirers Are Actually Buying

The biggest AI acquisitions of 2025 and early 2026 reveal a clear pattern. Acquirers are not paying premium multiples for revenue alone. They are paying for capabilities that would take years and hundreds of millions of dollars to replicate internally: proprietary data sets, specialized AI talent, trained models, and distribution advantages in specific verticals.

Consider the landmark transactions that defined the cycle. Alphabet's $32 billion acquisition of Wiz combined cloud security capabilities with AI-powered threat detection at a scale no internal build could match. Palo Alto Networks spent $25 billion on CyberArk to accelerate its identity security and AI integration roadmap. ServiceNow paid approximately $3 billion for Moveworks, acquiring a natural language AI platform that now powers its enterprise workflow automation. Workday closed a $1.1 billion deal for Swedish AI startup Sana, following its earlier acquisitions of Paradox and Flowise, to build an AI-native HR and finance platform.

But the trend extends well beyond mega-deals. In Q2 2025, IBM completed three AI acquisitions in a single quarter, while Intuit, Nvidia, Databricks, and Salesforce each closed two. These are not one-off moves. They represent systematic programs to embed AI capabilities across product portfolios. Enterprise software companies, in particular, have realized that their customers expect AI-native functionality, and the fastest path to delivering it is through acquisition.

For mid-market AI founders, this is encouraging. The acquirer pool is not limited to a handful of tech giants. Enterprise software companies, vertical SaaS platforms, private equity firms building technology platforms, and even industrial companies are actively seeking AI assets. The question is no longer whether acquirers want AI-native businesses. The question is which specific capabilities they are willing to pay a premium for in your vertical.

It is worth noting what acquirers are not buying. Pure AI wrappers, companies that have layered a ChatGPT-style interface on top of commodity foundation models without building proprietary data, workflow, or distribution advantages, are struggling to attract serious interest. The market has matured past the point where "we use AI" is sufficient. Buyers want to see that the AI creates genuine competitive differentiation that will persist through the next model generation cycle. The companies that clear this bar are seeing multiple competing offers; the ones that do not are finding it difficult to transact at the premiums they expected.

Vertical AI and AI Agents Are Driving the Next Wave of Consolidation

Horizontal AI platforms grabbed the headlines in 2023 and 2024. Foundation model companies like OpenAI and Anthropic dominated funding rounds and media coverage. But the M&A market in 2026 tells a different story. The action, particularly at the mid-market level, has shifted decisively toward vertical AI applications and AI agent platforms.

Vertical AI companies, those building AI-native solutions for specific industries like healthcare, legal, financial services, real estate, or manufacturing, are commanding some of the strongest multiples in the market. The logic is straightforward: these companies combine domain expertise, industry-specific data sets, and regulatory knowledge in ways that horizontal tools cannot easily replicate. Thomson Reuters' acquisition of Casetext for $650 million set the template. In 2025 and 2026, similar deals are happening across every major vertical, often at premium multiples that reflect the difficulty of assembling comparable domain-specific AI capabilities from scratch.

AI agents represent another major catalyst for M&A activity. Bain's 2026 M&A Report notes that deals for AI agent companies are accelerating as enterprise software companies race to integrate autonomous workflow capabilities into their platforms. The ServiceNow-Moveworks deal is the highest-profile example, but the consolidation extends to coding agents, sales automation agents, customer support agents, and operational AI platforms. Developer-facing agents that integrate directly into engineering workflows are drawing particularly strong interest from acquirers who value the durable, SaaS-like revenue characteristics of these tools.

The implication for AI founders building vertical or agent-based products is clear: the buyer universe is expanding, and the premium for deep specialization is growing. Companies that own proprietary workflows within a specific industry are positioned to attract multiple categories of acquirers, from horizontal SaaS platforms looking to add vertical depth to PE firms executing industry roll-up strategies.

We see a similar dynamic playing out at the lower end of the market. Smaller AI-native tools focused on a single vertical workflow, say a $300K to $800K ARR AI tool for real estate document analysis or automated financial reconciliation, are finding eager buyers on technology marketplaces like FE International's platform. These buyers, often operators or small PE firms, recognize that a focused vertical AI tool with proven retention and a clear data advantage is worth more than its current revenue suggests, because the AI moat compounds over time as the data set grows.

.png)

Enterprise AI Spending Is Fueling Acquisition Demand

Behind every AI acquisition is a fundamental business calculation: build versus buy. And in 2026, that calculation increasingly favors buying. The reason is that enterprise AI spending has reached a scale that creates enormous pressure on companies to deliver AI capabilities quickly, while also making AI-native targets more valuable as acquisition candidates.

Gartner forecasts global AI spending will reach $2.52 trillion in 2026, a 44% increase year-over-year. Generative AI model spending alone is projected to grow 80.8%. AI-optimized server spending is expected to jump 49%, and AI infrastructure will account for more than half of total AI outlays. PwC estimates that between $5 trillion and $8 trillion will be required over the next five years to fund AI technologies and the enabling infrastructure, a figure roughly equivalent to total TMT deal-making value over the past five years.

This spending surge creates acquisition demand in two ways. First, companies that have committed billions to AI infrastructure need applications and capabilities to run on that infrastructure, and buying proven AI-native companies is faster than building. Second, the customers of these companies now expect AI-native features as table stakes, which forces every enterprise software vendor to either build or acquire AI capabilities.

McKinsey's State of AI research found that 88% of companies now use AI in at least one business function, but only about one-third have begun scaling AI across their organizations. That gap between adoption and scale is precisely where M&A fills the void. Companies stuck in pilot mode are acquiring their way to enterprise-wide deployment, and the AI-native businesses they are buying carry the premium of having already solved the hardest scaling problems.

The four largest hyperscalers, Amazon, Google, Microsoft, and Meta, are expected to commit over $350 billion in AI-related capital expenditure in 2025 alone. That level of infrastructure investment creates a downstream demand wave: every dollar spent on AI compute infrastructure requires complementary investments in the software, applications, and tools that run on it. For AI founders building products that help enterprises deploy, manage, or operationalize their AI investments, the tailwinds are structural and multi-year.

%202020%20to%202026%20Forecast.png)

Private Equity Is Rewriting Its AI Acquisition Playbook

Private equity's role in AI M&A is expanding rapidly, and the playbook looks different from what PE firms traditionally execute. Global private equity transaction value reached almost $2 trillion in 2025, up from roughly $1.6 trillion in 2024, even as the number of deals slipped to approximately 34,300 from about 36,500. The shift toward fewer, larger, higher-conviction transactions reflects a PE industry that is deploying capital more selectively, often in consortium arrangements with complex capital structures.

For AI companies specifically, PE interest is concentrating in three categories. First, platform plays: PE firms are acquiring mid-market AI-native SaaS companies and using them as platforms for bolt-on acquisitions in the same vertical. A PE-backed vertical AI platform in healthcare, for example, might acquire three or four smaller AI tools to build a comprehensive, AI-native suite that commands a higher multiple at exit than any individual tool would on its own.

Second, PE firms are targeting AI infrastructure and data center assets, where the combination of recurring revenue, high switching costs, and capacity scarcity creates predictable cash flow profiles that align well with leveraged buyout models. The KPMG 2026 M&A Outlook found that 76% of firms already use AI in due diligence and 83% expect AI to improve post-merger integration, underscoring how deeply AI is embedded not just as an acquisition target but as a tool that PE firms use to create value in their existing portfolios.

Third, PE firms are increasingly comfortable with take-privates in the AI space. PwC's global M&A data shows that 74 megadeals of $5 billion or more were announced in 2025, the highest number since 2021, with more than 20% driven by AI. PE sponsors with $476 billion in global dry powder are looking for deployment opportunities, and AI-native businesses with proven recurring revenue, defensible moats, and growth potential are at the top of their lists.

For AI founders considering PE as a potential exit path, the dynamic is favorable. PE buyers bring capital for growth, operational discipline for scaling, and a willingness to pay competitive multiples when the business profile fits their investment thesis. And because PE firms typically hold portfolio companies for three to five years before seeking an exit, founders who sell to PE can often remain involved and benefit from the next phase of growth.

New Deal Structures Are Reshaping How AI Companies Change Hands

One of the more underreported AI M&A trends 2026 is the evolution of deal structures. The traditional acquisition playbook, where a buyer purchases 100% of a target's equity, is no longer the only or even the most common way AI transactions happen. A new set of hybrid structures has emerged, driven by regulatory scrutiny, talent scarcity, and the unique characteristics of AI assets.

The acqui-hire, where a larger company hires a startup's key talent while making a significant financial arrangement, has become a defining feature of AI deal-making. Morrison Foerster's analysis of 2025 technology M&A found that several of the year's largest AI deals were structured as hybrids: part acqui-hire, part infrastructure financing, part strategic partnership. Meta's $14.3 billion investment in Scale AI, combined with hiring the CEO, is a prime example. Google's $2.7 billion licensing arrangement to bring back key researchers from Character.ai follows the same pattern. These transactions achieve acquisition-like outcomes while navigating antitrust scrutiny and preserving operational flexibility.

The reverse acqui-hire structure, where a company pays a substantial licensing fee that gets distributed to shareholders as a dividend while separately hiring the target's leadership and core engineering team, is another increasingly common approach. Google's $2.4 billion arrangement with Windsurf exemplifies this model, as does Amazon's $330 million licensing deal with Adept AI.

Deloitte's 2026 M&A analysis observes that non-exclusive IP licensing is emerging as a distinct deal category, giving buyers immediate access to differentiated technology without a change-of-control transaction. For AI founders, this is important: it means there are more paths to a successful exit than the traditional full acquisition. Structured correctly, these alternative deal types can deliver strong outcomes for founders and investors while offering buyers the flexibility they need.

The key takeaway for sellers is to work with advisors who understand these evolving structures. The range of possible deal outcomes has expanded significantly, and founders who limit their thinking to a single transaction type may leave value on the table.

How AI Founders Can Maximize Their Exit Value in 2026

Strong market conditions do not guarantee a strong outcome for every seller. The companies capturing the highest multiples in AI M&A are the ones that have deliberately positioned themselves for acquisition. Based on what we see across hundreds of technology transactions, several factors consistently separate premium exits from average ones.

Demonstrate That AI Drives Measurable Customer Value

Buyers in 2026 are done paying for AI promises. They want to see evidence that AI functionality is driving retention, expansion, or cost savings for customers. Net revenue retention above 120% is the clearest signal. If your AI features are increasing customer spend over time, that shows up directly in the NRR number, and acquirers will pay a premium for it. Conversely, if your AI features are impressive demos that do not move business metrics, the premium disappears.

Build and Protect Your Data Moat

Proprietary data is the most durable competitive advantage in AI. If your company's AI is built on the same foundation models available to every well-funded startup, the feature advantage is temporary. Strategic buyers are explicitly looking for data engines: companies whose AI improves with usage because it is trained on data that competitors cannot easily access or replicate. Document your data provenance, governance practices, and the specific ways your data set creates compounding advantages.

Get Your Financials and Documentation Ready Early

AI companies face unique due diligence scrutiny around inference costs, model dependencies, and compute commitments. Buyers will examine your gross margins with AI costs fully loaded. They will want clarity on which models you depend on, how your cost structure changes as you scale, and whether you have vendor lock-in risk with cloud or model providers. Having clean answers to these questions, backed by documentation, accelerates deal timelines and protects your valuation. FE International's exit planning guide for SaaS founders covers these preparation steps in detail.

Choose the Right Path to Market

The ideal exit path depends on the size and maturity of your business. For AI businesses generating under $1 million in annual revenue, FE International's online marketplace connects sellers directly with a curated pool of vetted buyers, including individual acquirers, search funds, and small PE firms looking for AI-native acquisition targets. The marketplace provides a streamlined listing, diligence, and transaction process specifically designed for lower mid-market technology businesses. Sellers benefit from exposure to thousands of qualified buyers actively seeking AI opportunities, while buyers gain access to pre-vetted technology businesses they would struggle to find through other channels.

For AI companies above that threshold, working with an experienced M&A advisory team provides the strategic positioning, buyer outreach, competitive deal process, and negotiation expertise needed to capture the full premium the market supports. With over 1,500 successful exits since 2010, FE International's advisory practice combines deep AI sector knowledge with the operational infrastructure to manage complex, multi-party transactions. The advisory and marketplace operate as complementary channels: together, they cover the full spectrum of AI business exits, from early-stage tools to enterprise-scale platforms.

What This Means for Acquirers Seeking AI-Native Targets

The buy side of AI M&A is evolving just as quickly as the sell side. EY's February 2026 M&A activity report notes that large-cap acquirers continue to pursue AI capabilities as a top priority, with technology, healthcare, and energy leading sector activity. But competition for quality AI targets is intensifying, which means buyers need to move faster, evaluate more creatively, and engage with deal sources that can surface opportunities before they hit the broader market.

For corporate development teams and PE firms actively acquiring AI-native companies, a few dynamics are shaping 2026 deal-making:

Valuation expectations are anchored to the premium. AI founders are aware of the multiples their peers are commanding. Lowball offers will not get you to the table. Buyers who succeed in this market come prepared with comp sets that justify their pricing and deal structures that align seller incentives with post-acquisition performance.

Speed matters more than it used to. The best AI-native targets attract multiple bidders quickly. The Stanford AI Index found that total corporate AI investment reached $252.3 billion in 2024 alone, with private investment jumping 44.5% year-over-year. That flood of capital means founders have options. A slow, bureaucratic acquisition process will lose to a faster, better-prepared competitor.

Access to deal flow is a competitive advantage. The most attractive AI targets are often not publicly marketed. Buyers who maintain relationships with M&A advisors specializing in AI and technology, such as FE International's advisory and marketplace platform, gain access to proprietary deal flow that is not available through general market channels. For acquirers searching for AI businesses under $1 million in value, the FE International marketplace offers a curated selection of vetted technology businesses with detailed financials, traffic data, and technical documentation ready for review.

The Window for AI Founders Is Open. Here Is How to Act.

The AI M&A trends 2026 are unambiguous: more capital, more buyers, and higher multiples for AI-native businesses than at any previous point. The convergence of record enterprise AI spending, strategic urgency among acquirers, and an expanding buyer pool that now includes PE firms, SaaS platforms, and non-tech corporates has created conditions that distinctly favor sellers of well-positioned AI companies.

But favorable conditions do not last indefinitely. Capital cycles shift. Acquirer priorities evolve. Regulatory environments change. The founders who capture the full premium are the ones who prepare early, position their companies with precision, and partner with advisors who understand the specific dynamics of AI transactions. Waiting for "a better time" is a strategy that works until it does not. Every AI M&A cycle eventually cools, and the sellers who fare best are those who act when conditions favor them, not those who try to time the absolute peak.

Whether your AI business is generating its first $500K in ARR or operating at $10M and above, FE International can help you understand your options. For smaller AI businesses, list on the FE International marketplace to connect with thousands of active, vetted buyers. For larger transactions, request a free, confidential valuation from FE International's advisory team. With more than 1,500 successful exits since 2010, including deep expertise across AI, SaaS, cybersecurity, fintech, edtech, ecommerce, and marketplace verticals, FE International is the technology M&A advisor that AI founders trust to deliver premium outcomes. Start with a valuation. It is free, it is confidential, and it gives you the data you need to decide when and how to make your move.