US shoppers spent $326.7 billion online in the first quarter of 2026, up 9.8% year over year and growing at more than double the pace of retail as a whole. Behind that number sit hundreds of thousands of independent Shopify and DTC brands, and a deepening pool of buyers who want to own them. If you are researching Shopify ecommerce brand valuation in 2026, the short answer is this: your brand is worth a multiple of its provable earnings, and that multiple is set by how transferable, sustainable, and scalable those earnings look to a buyer.

This guide covers the full picture: the valuation methods used in real transactions (SDE, EBITDA, and revenue multiples), 2026 benchmark data, the specific metrics that push multiples up or down, and what recent strategic acquisitions of DTC-born brands reveal about what acquirers actually pay for. It draws on FE International's experience across 1,500+ completed transactions, alongside current data from the US Census Bureau, Bain, McKinsey, and Shopify's own filings.

Whether you run a $500,000 Shopify store or a $50 million omnichannel brand, the mechanics below are the same ones a buyer will apply to your business. Understanding them before you speak to anyone is the cheapest way to add value to your eventual exit. We also cover where the FE International M&A Platform fits for brands under $1 million, because the right sale route depends on the size of what you have built.

The 2026 Market Backdrop: Why Ecommerce Valuations Are Holding Firm

Start with demand for the product category itself. Ecommerce accounted for 16.9% of total US retail sales in Q1 2026, the highest share on record, and online sales grew 9.8% year over year against 3.9% for retail overall. Globally, online retail passed $6.4 trillion in 2025 and continues to take a growing share of total retail spend, with forecasts pointing to roughly $6.9 trillion in 2026. The channel your brand sells through keeps expanding, and buyers price that structural growth into their models.

Deal-making conditions improved just as sharply. Global M&A value rose 40% in 2025 to $4.9 trillion, the second-highest year on record, and 80% of the M&A executives Bain surveyed expect to sustain or increase deal activity in 2026. Consumer brands are a central part of that story. Acquisitions of insurgent brands have gone mainstream: deals under $2 billion now represent 38% of US consumer products M&A, up from about 16% over the prior five years, as large acquirers buy their way into new categories, channels, and customer cohorts.

What changed since the 2021 aggregator era is not appetite. It is selectivity. Buyers in 2026 underwrite contribution margin, retention, and channel durability rather than topline growth alone, which means well-prepared brands stand out and command premium attention. For founders who can document quality, this is one of the most constructive selling windows in years.

The window works for both sides of the table. Buyers get record ecommerce penetration at normalized entry prices, with a growing backlog of quality private assets coming to market. Sellers get a broader, better-capitalized buyer pool competing for the same well-run brands: private equity platforms, strategics, family offices, and experienced individual acquirers, each with a different reason to pay. Competitive tension between buyer types is what turns a fair price into a strong one.

.png)

Buyers in 2026 are not paying less for ecommerce brands. They are paying more selectively, which rewards founders who can prove quality with data.

Shopify's Own Valuation in 2026: What Platform Momentum Means for Your Brand

The phrase “Shopify brand valuation” carries two meanings, and both matter to a founder. One is what public markets say Shopify Inc. is worth. The other is what your Shopify-built brand is worth in a private sale. The two numbers are different, but they move on the same fundamentals: growth, retention, and cash generation. Here is the company side first, because the platform's trajectory shapes buyer confidence in every business built on it.

How Is Shopify's Ecommerce Brand Valued in 2026?

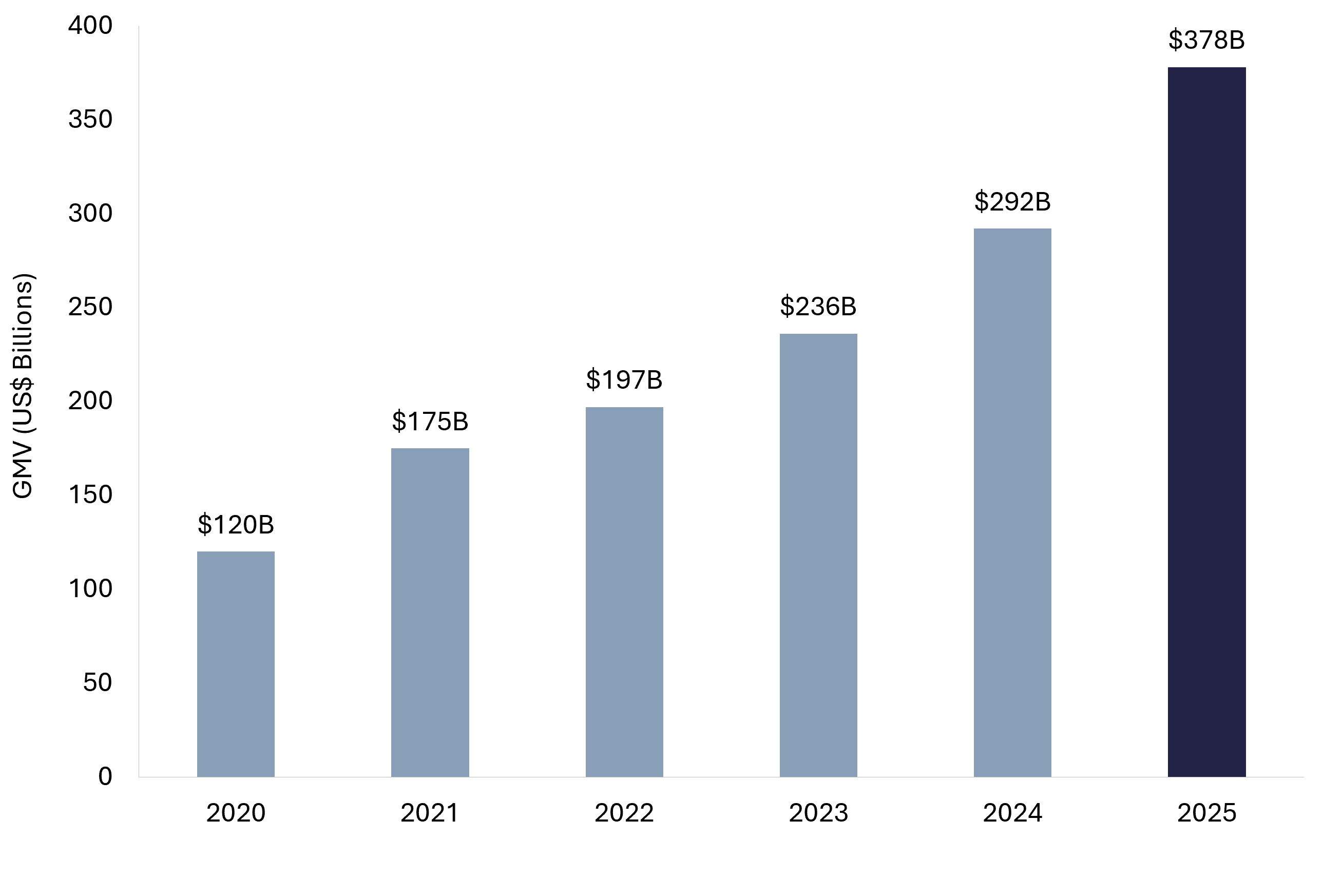

Shopify closed 2025 with $11.6 billion in revenue, up 30%, and $378.4 billion in gross merchandise volume, up 29%, alongside more than $2 billion in free cash flow at a 17% margin. Public investors value that performance at a premium: the stock trades at a forward price-to-sales ratio of about 8.9x, well above the industry average of 6.6x, with 2026 revenue consensus near $14.7 billion. Within a global online retail market approaching $6.9 trillion, Shopify's merchants generate more combined volume than the entire ecommerce economies of most countries, which is why the company anchors nearly every list of top ecommerce brands by valuation in 2026. Market trends feed directly into that valuation. Every point of ecommerce penetration, every merchant cohort that scales, and every new commerce surface Shopify monetizes shows up in the growth assumptions behind its multiple.

Shopify vs Amazon: Two Different Valuation Stories

Comparisons with Amazon and eBay come up constantly, and the useful distinction is business model. Amazon is a demand aggregator that owns the customer relationship. Shopify is commerce infrastructure that lets merchants own it themselves, and the company now powers more than 14% of US ecommerce. Markets reward that infrastructure position: Shopify's forward price-to-sales multiple of roughly 8.9x sits far above Amazon at about 3.0x, because investors pay up for platform economics and faster growth. Set against eBay's legacy auction model or traditional retail comparables, the same pattern holds: commerce infrastructure with network effects earns premium multiples, while store-count economics do not. The logic applies one level down, too. A brand that owns its customer data and demand channels earns a stronger multiple than one renting all of its demand from a single third-party channel, a point we return to below.

Future Projections, Investor Interest, and the Stock

Investor interest in Shopify heading through 2026 rests on execution against ambitious forecasts. Consensus estimates put revenue near $14.7 billion for 2026 and $18.0 billion for 2027, implying growth of 27% and 22%. The company has backed its own outlook with a $2 billion share repurchase program launched from a position of operating strength. A premium multiple leaves little room for missteps, which is precisely why analysts watch the numbers that also matter to merchants: GMV growth across regions, payments penetration, and how quickly agentic commerce converts into orders. Strong projections for the platform read through as durable demand for the brands built on it.

Innovation, AI, and Shopify's 2026 Growth Strategy

Shopify's competitive advantage in 2026 rests on how aggressively it is building for AI-driven commerce. The company launched the Universal Commerce Protocol with Google, expanded its Sidekick assistant across merchant operations, and reports that orders coming from AI searches have grown 15x since January 2025. Consumer behavior is moving the same direction: 68% of US consumers used an AI tool in the past three months, and 28% of Gen Z already shops with AI assistance. Partnerships, technology adoption, and this agentic commerce push are exactly the kinds of catalysts analysts cite when projecting Shopify's brand value forward.

What Shopify's Valuation Means for Small Businesses and Brand Owners

Platform strength flows downstream. International revenue grew 36% in 2025, with expansion across emerging markets, checkout and payments keep improving, and the AI investments give independent merchants distribution surfaces that once belonged only to the largest retailers. For acquirers, a thriving, investor-backed platform reduces perceived infrastructure risk in every Shopify-built target. Buyers also increasingly screen supply chain resilience and sustainability practices during diligence, and Shopify's tooling makes both easier to evidence. The takeaway for owners: the rails your brand runs on are getting more valuable, and disciplined operators capture part of that in their exit multiple.

Shopify's corporate valuation and your store's valuation are different numbers built on the same fundamentals: growth, retention, and cash generation.

The Three Ways Buyers Value a Shopify or DTC Brand

Every serious offer you receive will be built the same way: a measure of earnings multiplied by a number that reflects risk and growth. Which earnings measure applies depends mostly on your size and how the business is run. Our full guide on how to value an ecommerce business goes deep on the mechanics; here is the working summary.

SDE: The Standard for Owner-Operated Brands

Seller's Discretionary Earnings measures the total financial benefit available to a single owner-operator. Start with net income, then add back the owner's salary, personal expenses run through the business, and genuine one-time costs. For companies valued under roughly $10 million, SDE is used almost exclusively, because it shows a buyer the true cash the business generates for whoever owns it.

A worked example. A Shopify apparel brand shows $240,000 in net income. The owner pays herself $90,000, ran $20,000 of personal travel and software through the business, and absorbed a $10,000 one-time legal cost. Her SDE is $360,000. At a 3.2x multiple, the business is worth $1,152,000, with inventory then added on top at cost. The multiple, not the profit line, is where most of the negotiation happens.

Add-back discipline matters here. Buyers accept the owner's salary, genuinely personal expenses, and true one-off costs. They reject add-backs that quietly recur every year, unpaid family labor the new owner would have to replace, and any suggestion that slashing the ad budget counts as found profit when that spend is what drives the revenue. Overreaching on add-backs is the fastest way to lose a buyer's trust in the rest of your numbers, so build the SDE bridge conservatively and document every line.

EBITDA: The Institutional Benchmark

Above roughly $10 million in value, buyers switch to EBITDA: earnings before interest, taxes, depreciation, and amortization. The key difference from SDE is that owner or management compensation stays in as a real operating expense, because private equity firms and strategic acquirers assume professional management will run the business. The $5 million to $10 million zone is the messy middle. If the founder still does everything, expect an SDE conversation; if a real team runs daily operations, EBITDA applies, and EBITDA-based valuations are usually the higher-value basis.

Revenue and ARR Multiples: The Exception Cases

Revenue multiples appear when current profitability understates the trajectory of the business, typically in high-growth brands investing ahead of earnings, or where a subscription component makes revenue unusually predictable. Replenishment and subscription models with low churn can price at 4x to 10x annual recurring revenue, similar to software. One caution: revenue multiples dominate headlines because strategic mega-deals get reported that way, but in the lower middle market it is cash flow that closes transactions. Treat any revenue-based number you read as a cross-check, not a promise.

A fourth method deserves a mention. Discounted cash flow analysis projects the free cash a business will generate and discounts it back to a present value. Institutional buyers run a DCF to pressure-test what a multiple implies, and it is genuinely useful for mature brands with several years of steady results. In practice, though, a DCF is only as reliable as its growth and discount-rate assumptions, so in the lower middle market it supports the price conversation rather than setting it. Our broader guide to valuing an internet business walks through the method in full.

Under roughly $10 million in value, expect an SDE conversation. Above it, expect EBITDA. In between, the depth of your team decides the basis.

2026 Benchmarks: Shopify Ecommerce Brand Valuation Multiples

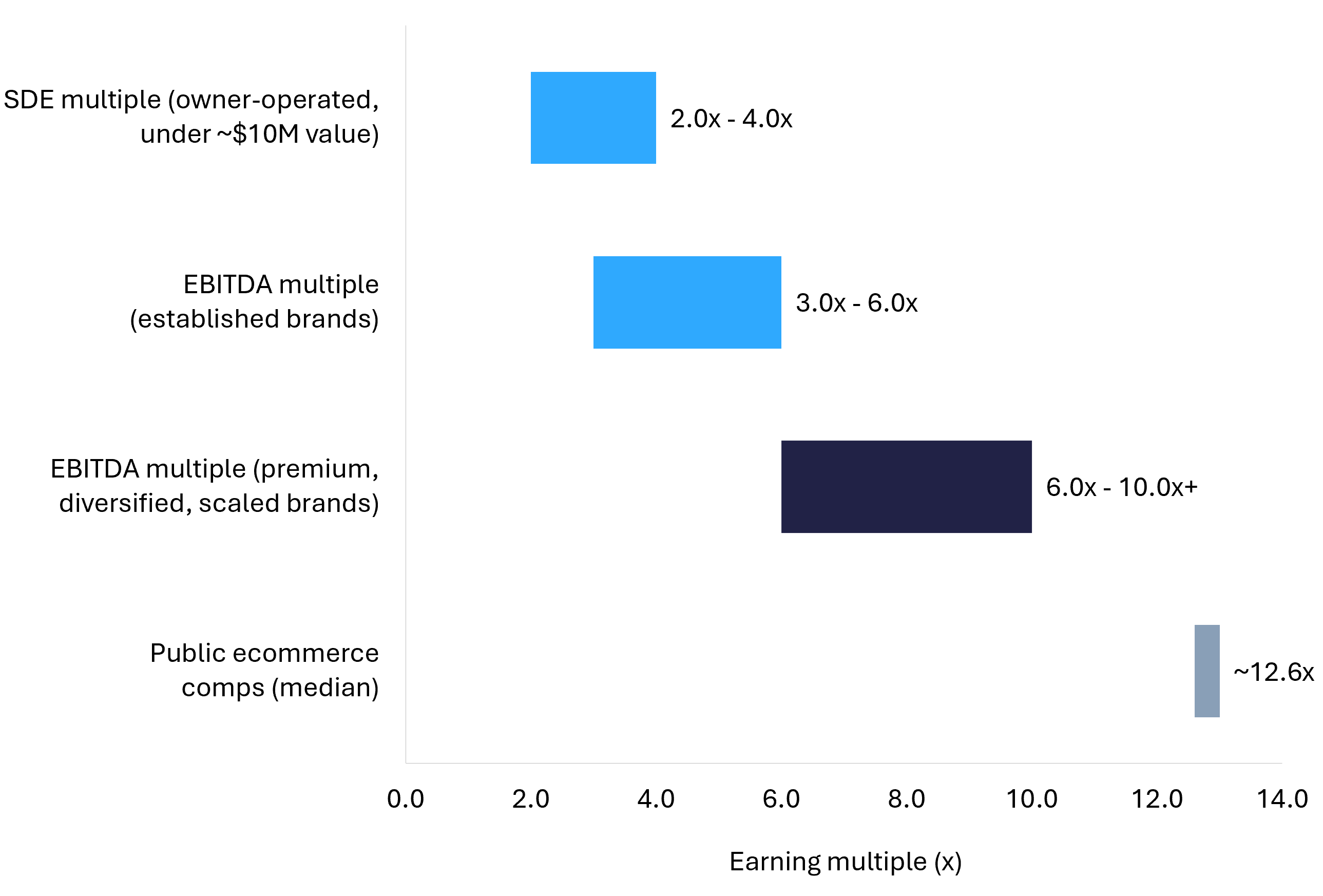

So what do the multiples actually look like this year? Across FE International's ecommerce transaction data, smaller owner-operated brands typically transact at 2.0x to 4.0x SDE, established businesses at 3.0x to 6.0x EBITDA, and premium diversified brands at 6.0x to 10.0x or more, with public ecommerce companies averaging around 12.6x EBITDA as the ceiling private valuations trend toward at scale. Businesses that score well across the core value drivers, transferability, sustainability, and scalability, consistently land in the 4.0x to 6.0x band, and omnichannel operators earn a further 15% to 25% premium over pure-play online peers.

Two adjustments matter in every ecommerce deal. First, inventory is valued separately and added to the purchase price at landed cost, so a $1.15 million business with $150,000 of sellable stock changes hands at $1.3 million. Second, business model shifts the band: dropshipping and single-product Amazon models sit at the bottom of the ranges because the demand is rented, while brands with proprietary products, owned audiences, and subscription revenue sit at the top. An Amazon-heavy brand and a diversified DTC brand with identical earnings will not receive identical offers, and the gap can run a full turn or more.

How does an advisor land on the exact number inside those ranges? At FE International, the multiple comes from a proprietary framework refined across thousands of data points and hundreds of ecommerce transactions, scoring each business on three families of drivers: transferability (how cleanly the earnings move to a new owner), sustainability (how defensible they are against competition and channel shifts), and scalability (how much headroom a buyer can underwrite). Every metric in the next section rolls up into one of those three questions.

Strategic acquirers stretch well past these bands when a brand fits a portfolio need. Beauty and personal care transactions averaged 3.6x revenue and 13.5x EBITDA from 2022 through mid-2025, against 1.9x revenue and 11.2x EBITDA for consumer packaged goods overall. Those are outcomes for category-defining brands, not baselines, but they show how high the ceiling sits when brand equity is real.

Most Shopify and DTC brands transact between 2.0x and 6.0x earnings in 2026. The spread between those numbers is where preparation pays.

The Metrics That Move Your Multiple Up (or Down)

Buyers do not pay for revenue. They pay for the confidence that earnings will still be there in year three under new ownership. Every diligence question maps to one of a handful of metrics, and each one nudges your multiple in a measurable way.

Revenue quality and retention. Repeat purchase rate is the first cohort number a buyer pulls. Brands where 25% to 40% of orders come from returning customers price meaningfully above one-and-done catalogs, and a lifetime-value-to-acquisition-cost ratio of 3:1 or better signals durable unit economics. Church & Dwight's CEO cited Touchland's high level of brand loyalty and repeat purchase when announcing an $880 million acquisition, which tells you exactly how acquirers think.

Contribution margin stability. Modern buyers rebuild contribution margin per SKU per channel across 24 months: revenue minus product cost, fulfillment, payment processing, and allocated paid acquisition. A brand holding a steady 30% contribution margin outprices one drifting from 35% down to 28%, even at identical revenue.

Channel and traffic mix. Owned DTC plus a second channel, whether Amazon, retail, or B2B, beats any single-channel concentration. When one channel or platform carries more than 70% of revenue, buyers discount for fragility. Strong organic and brand-name search traffic, plus an email and SMS list that drives a real share of revenue, earns a premium because the audience transfers with the sale.

Owner independence and operations. The more the business depends on you, the less it is worth to someone who is not you. Documented SOPs, a capable team or agency bench, supplier redundancy, and healthy inventory turns all push the multiple up. Registered trademarks and clean, accrual-based books are table stakes.

Growth trajectory and seasonality. Two to three years of steady growth is the simplest signal a buyer can underwrite, and it prices better than a spike-and-plateau pattern at the same revenue. Heavy seasonality is workable when it is predictable; buyers simply model it and may lean on earnout structures to share the timing risk. If recent quarters have softened, the constructive move is to stabilize the trend before going to market, because buyers weight the trailing twelve months most heavily and reward a business that enters the process on an upswing.

AI discoverability, the new 2026 driver. With AI-originated orders up 15x on Shopify since early 2025 and AI shopping tools moving mainstream, buyers have started asking how well a catalog surfaces in agentic channels: structured product data, first-party data depth, and presence in AI-driven discovery. This is the same shift reshaping how consumers find brands in the first place, and early traction here wins valuation arguments that did not exist two years ago. Diligence checklists are already adding a line for it.

.png)

A buyer prices the confidence that your earnings survive the handover. Every metric above is a proxy for that confidence.

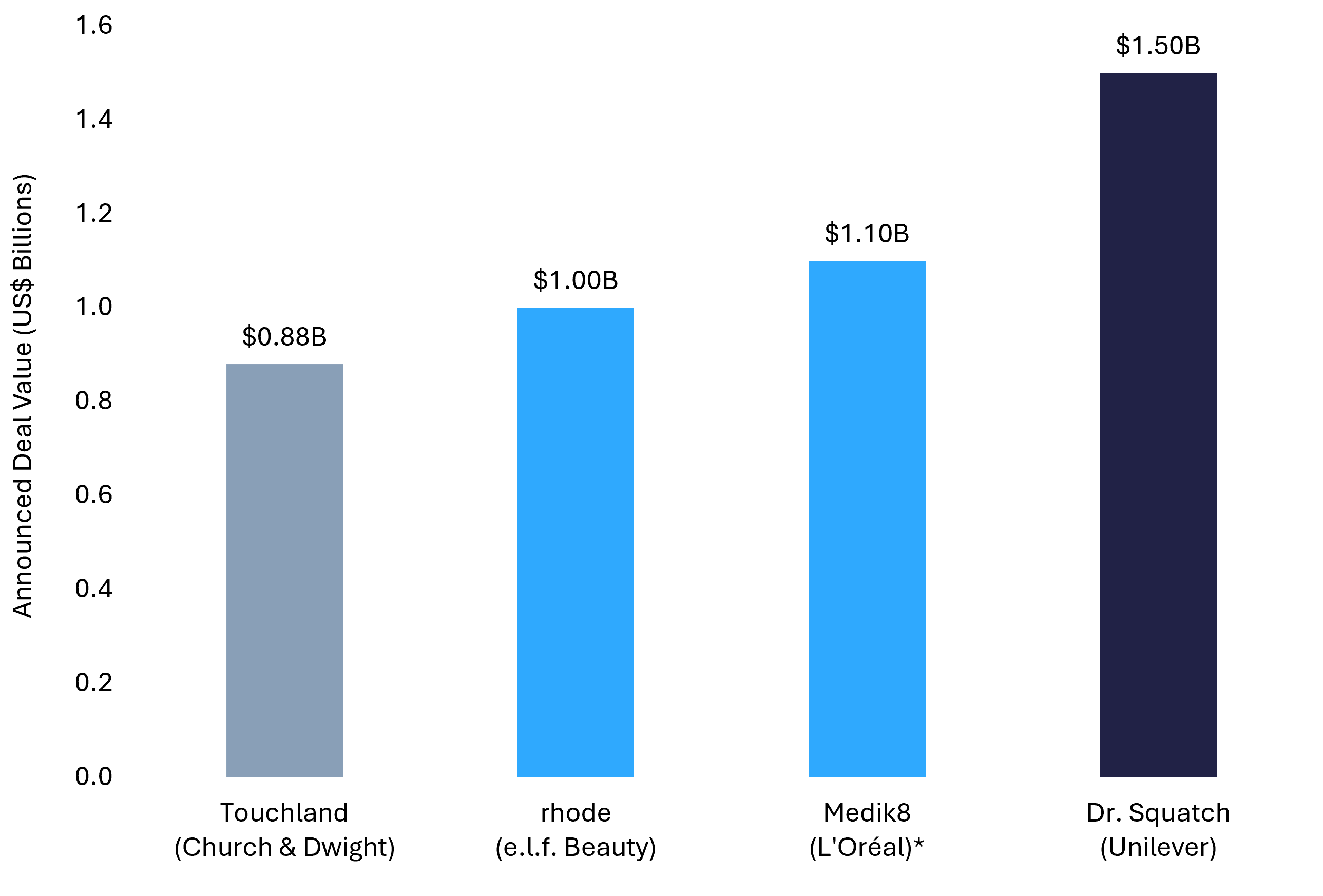

Real Deal Examples: What 2025 and 2026 Transactions Reveal

Benchmark ranges become concrete when you look at what acquirers signed for. Four strategic acquisitions of DTC-born brands announced in 2025 carry lessons that apply at every deal size.

e.l.f. Beauty and rhode: structure is part of the price. e.l.f. agreed to acquire Hailey Bieber's rhode for $1 billion, structured as $800 million at closing plus a $200 million earnout tied to three years of growth. Earnouts of this kind now appear in 25% to 40% of consideration in typical ecommerce transactions, bridging the gap between a seller's conviction and a buyer's caution. The lesson for founders: negotiate the structure as carefully as the headline number.

Unilever and Dr. Squatch: community compounds into a strategic premium. Unilever completed its acquisition of Dr. Squatch, the men's personal care brand that started selling soap online in 2013, for a total consideration of €1,243 million. The brand had built more than 8% US share in bar soap on the strength of its content-led, direct-to-consumer engine. A distinctive voice and a loyal community turned a commodity category into a nine-figure exit.

Church & Dwight and Touchland: retention shows up in the multiple. Church & Dwight paid $700 million at closing plus up to $180 million in earnout for Touchland, a brand with roughly $130 million in trailing sales, an implied multiple near 6.8x revenue. Loyalty and repeat purchase were the qualities the acquirer named on announcement day.

L'Oréal and Medik8: defensible product wins premium pricing. L'Oréal's majority acquisition of science-led skincare brand Medik8 was reported at around $1.1 billion, one of the richest multiples in the category, anchored in formulation credibility competitors could not copy.

It helps to name what these deals sit on top of. The buyer pool for ecommerce brands has matured well beyond the 2021 aggregator playbook: private equity platforms, family offices, strategic operators, and search funds now compete alongside experienced individuals, and capital in the consumer sector is clearly moving again. Sharper underwriting cuts both ways for founders. It means more questions in diligence, and it means a genuinely strong brand gets recognized and paid for instead of lost in a crowd of look-alike listings.

None of these founders started with a billion-dollar brand. The drivers that earned their premiums, retention, community, margin, and defensibility, are the same ones that move a $2 million Shopify exit from 2.8x to 3.6x. The checks differ; the underwriting does not.

Strategic buyers paid up to 6.8x revenue for DTC brands in 2025. They were not buying products. They were buying retention, community, and margin.

How to Increase Your Brand's Valuation Before You Sell

Multiples reward preparation, and most of the highest-return moves take 12 to 24 months to show up in the numbers a buyer will trust. Start early. Our guide on how to sell an ecommerce business covers the process end to end; these are the levers with the biggest effect on price.

- Clean up the financials. Accrual accounting, channel-level P&L, and reconciled payment processor data. Every hour spent here removes a diligence discount later.

- Add a recurring revenue layer. Subscriptions and replenishment programs make cash flow predictable, and predictability is what multiples pay for.

- Diversify one channel beyond your core. A second proven channel, even at 15% of revenue, changes how a buyer models risk.

- Grow the owned audience. Email and SMS revenue transfers with the sale; rented reach does not.

- Reduce owner hours and document everything. SOPs, delegated supplier relationships, and a team that runs the week without you.

- Secure the moat. Trademarks, brand registry, supplier redundancy, and structured product data ready for AI-driven discovery.

- Build the data room early. Cohort retention, contribution margin by SKU, and traffic analytics, organized before anyone asks.

A brand that executes even four of these typically moves a full turn on its multiple. On $500,000 of SDE, one turn is half a million dollars for work you control entirely.

Timing matters as much as the checklist. Start the preparation 12 to 24 months before you want to close, since retention cohorts and margin trends only become credible once a buyer can see them across multiple quarters. If your fundamentals are already strong, the current market rewards acting rather than waiting: valuations for high-quality ecommerce businesses are holding firm and rising into 2026, and a sale process typically runs several months from preparation to close, so decisions made now land inside this window.

On $500,000 of SDE, one extra turn on the multiple is $500,000 of value. Preparation is the highest-margin project in ecommerce.

Two Paths to a Sale: FE International Advisory and the FE International M&A Platform

Where you sell should match the size and profile of what you have built, and FE International runs both routes side by side, for sellers and for buyers.

For brands valued above roughly $1 million: a full advisory process. FE International has completed more than 1,500 transactions with a 94.1% success rate, running competitive, confidential processes that put your brand in front of vetted strategic acquirers, private equity firms, family offices, and experienced individual buyers across 34 countries. Deal structuring, earnout negotiation, and diligence management are handled by a team that does this every week.

For brands under $1 million: a full investment-bank-style process rarely makes economic sense at this size, which is exactly why the strongest sub-$1M businesses list on the FE International M&A Platform. It is a curated, structured environment built for both sides of the deal: sellers get vetted, qualified buyer demand without running a lengthy process, and buyers browse pre-screened listings with live metrics and make offers through a structured flow. The Platform extends FE International's standards down-market; it works alongside the advisory practice rather than replacing it.

For buyers: both routes apply in reverse. Acquirers targeting $1M+ businesses work with the advisory team on mandated opportunities, while those hunting below $1 million can source directly on the Platform, where every listing has passed pre-screening before it reaches the market. Our 2026 ecommerce buyer's guide walks through diligence, deal structures, and the first 100 days.

Whichever route fits, the starting point is identical: an accurate, current valuation. A proper one gives you a defensible range, the buyer types most likely to compete for your profile, and a candid read on which fixes would raise the number, all before you commit to anything.

Get an Accurate Valuation for Your Shopify or DTC Brand

Shopify ecommerce brand valuation in 2026 comes down to a formula anyone can learn and a multiple that rewards evidence. The market backdrop is working in sellers' favor: record ecommerce penetration, resurgent M&A, and strategic acquirers proving they will pay premium multiples for retention, community, and margin. The founders who capture those premiums are the ones who prepare like buyers think.

Ranges tell you the neighborhood. Your actual number depends on cohort retention, contribution margin, channel mix, and a dozen factors a benchmark table cannot see. FE International provides free, confidential valuations built on 1,500+ completed transactions, with no obligation attached. If your brand generates under $1 million in value, the FE International M&A Platform gives you a direct, structured route to qualified buyers. Either way, the smartest first step is the same: find out what your brand is really worth, from the team that closes these deals at a 94.1% success rate.