FishPal acquired Clubmate, the UK's leading vertical SaaS and embedded payments platform for angling clubs and fisheries. FE International acted as exclusive sell-side advisor to Clubmate and brought the transaction to completion within 35 days of the signed letter of intent.

That speed was not luck. Clubmate sits in one of the most in-demand corners of software M&A today: vertical SaaS paired with embedded payments. For any founder thinking about selling a vertical SaaS business, the Clubmate sale is a useful guide. It shows what buyers chase, why they move quickly, and what separates a fair price from a premium one.

This article breaks down the model behind the deal. We cover what vertical SaaS and embedded payments mean, why the pairing earns strong buyer interest in 2026, the market data behind that demand, and the practical steps owners can take to position for a clean, well-priced exit.

Inside the Clubmate Acquisition

Clubmate was founded in 2017 by Owen Chapman to digitize a sector that still ran on paper forms, posted cheques, and manual administration. What started as a fix for one broken process grew into the operating system for its category, now serving hundreds of clubs, fisheries, and governing bodies across the UK.

The platform sits at the center of how the sector transacts. Members buy memberships and day tickets, book sessions, and pay online, while clubs handle permits, communications, compliance, and bankside checks from a single system. The part that matters most to buyers: Clubmate earns money two ways. It collects recurring software subscriptions, and it captures embedded payment economics on every membership renewal, day ticket, and booking processed on the platform.

Demand for that kind of infrastructure is rising alongside the sport. In England, rod licence sales rose for a second consecutive year in 2024 to 2025, the first back-to-back increase since 2010. As participation grows, clubs and fisheries are moving off spreadsheets and toward integrated platforms that combine memberships, bookings, and payments. That is exactly what Clubmate spent years building.

For FishPal, which has offered online rod-fishing booking since 2003 and owns Elveguiden, the market leader across Scandinavia, the deal adds Clubmate's management depth, bookings, embedded payments, and 380 vendors. FishPal already handles more than 15 million website visits, over 80,000 rod bookings, and more than 100,000 registered customers each year. Max Alderman, Partner at FE International, described Clubmate as a category-defining platform with a genuine moat, deep customer loyalty, and the recurring revenue economics the best acquirers look for.

The combination is the point. Bringing Clubmate, FishPal, and Elveguiden under one brand gives clubs, fisheries, and anglers more in a single place: bookings, memberships, payments, and management tools that used to sit in separate systems or in none at all. For a strategic buyer, that is a clean fit. FishPal already owned the audience and the booking demand, and Clubmate added the operating system and the payment rails underneath it. Owen Chapman built Clubmate to give people their time back so they could spend more of it fishing, and that focus on a single, well-understood job is what turned a niche tool into an asset worth acquiring.

What “Vertical SaaS With Embedded Payments” Means

Vertical SaaS is software built for one industry's workflows rather than for everyone. Horizontal SaaS, such as a general CRM or accounting tool, serves any business. Vertical SaaS, such as software for angling clubs, dental practices, or restaurants, is shaped around the specific tasks, rules, and language of a single sector. That focus tends to produce deeper customer relationships and higher switching costs, because the product is woven into how the business actually runs.

Embedded payments are the second half of the story. Embedded finance describes a non-financial software platform that offers an adjacent financial service, such as payments or lending, and takes a share of the economics. Embedded payments are the most common form: instead of sending customers to a separate processor, the platform handles the transaction inside its own product and earns a cut of every payment.

Put the two together and the logic is simple. The software wins the customer and owns the daily workflow. The payments turn each transaction into high-margin, recurring revenue that grows with customer activity, not just with the number of seats sold. This pairing has moved from novelty to standard practice. More than half of relevant independent software vendors in North America offered embedded payments in 2025, and integrated-payments providers already account for 36 percent of US small and medium business acquiring revenue, a share expected to reach 45 percent by 2028. Platforms such as Toast in restaurants and Shopify in commerce built large businesses on the same idea.

Why Buyers Pay a Premium for This Model in 2026

Acquirers like predictable revenue, and this model delivers two streams of it. The subscription line gives steady, recurring software income. The payments line adds revenue that scales every time a customer transacts. Together they raise the revenue per account and deepen the relationship, which makes the customer base harder for anyone else to pry loose.

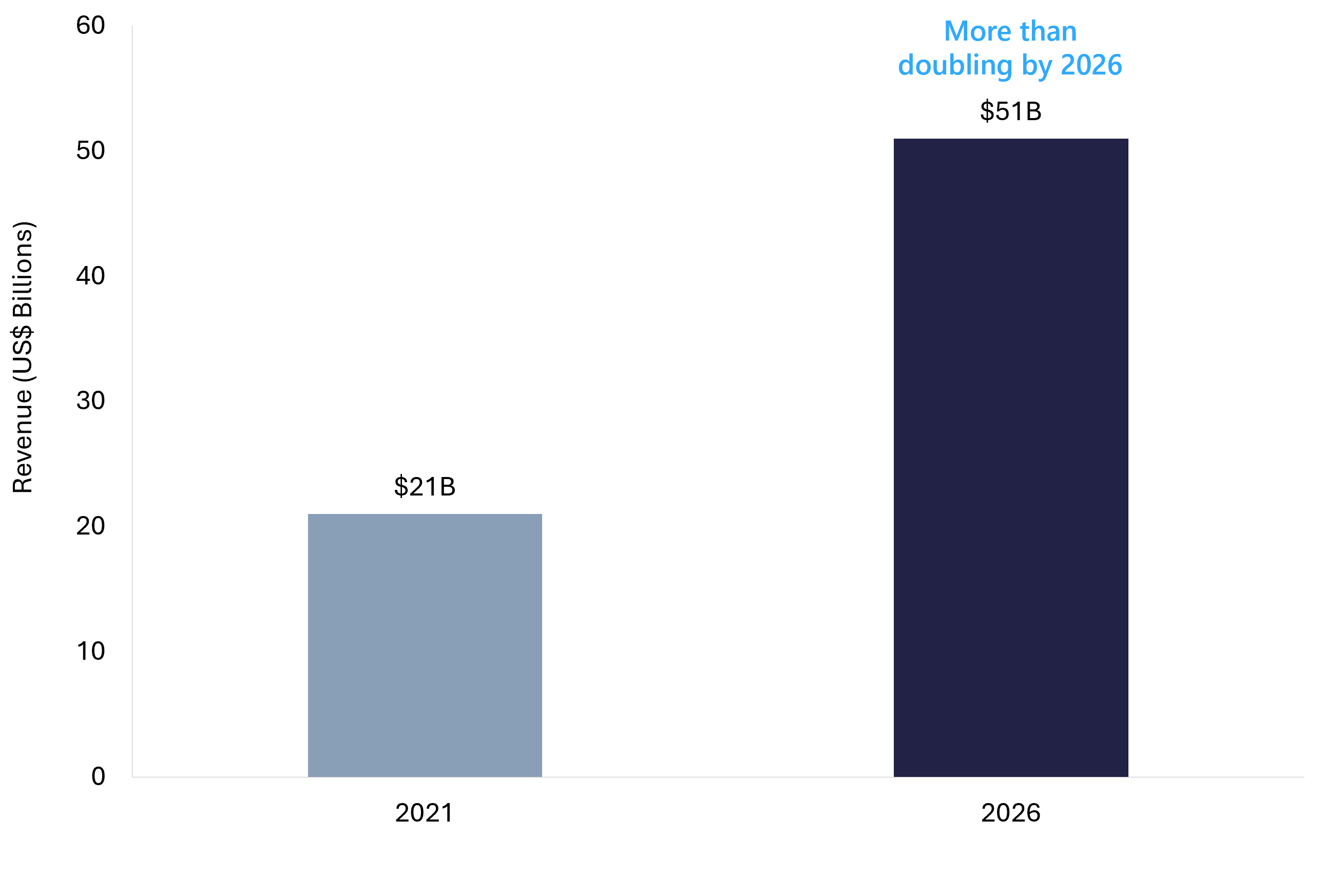

The pool behind embedded payments is large and growing. US embedded finance transaction value is on track to exceed $7 trillion in 2026, with revenue for software platforms and the providers that enable them climbing from $21 billion in 2021 to $51 billion. That is a structural shift in how software companies make money, and it rewards platforms that already sit inside a customer's daily workflow.

Pricing power follows from that structure. A business with both subscription and payment revenue has two ways to grow inside each account, which makes its future earnings easier to defend and easier to forecast. Strategic acquirers want the capability and the customer relationships. Financial buyers want the durable, recurring cash flow. When a vertical platform offers both at once, those two buyer types compete for the same asset, and that overlap is what tends to lift offers.

Buyers are acting on it. In 2026, fintech and payments dealmaking is centered on capability-driven acquisitions, including embedded finance. In plain terms, strategic acquirers are shopping for exactly the capability Clubmate had: a vertical platform that owns a workflow and monetizes the payments inside it. When a business combines both, it competes for the attention of several buyers at once, and competition is what moves price toward the premium end.

The 2026 M&A Backdrop Favors Quality Software

Timing rarely makes or breaks a good business, but the current market gives well-run software companies a strong tailwind. Dealmaking has rebounded with force. Global M&A deal value rose roughly 43 percent in 2025 to about $4.7 trillion, led by larger, more strategic transactions, with software contributing the largest share of value among the fastest-growing sectors.

The momentum carried into this year. Global M&A reached a record of about $1.6 trillion in the first quarter of 2026, up more than 50 percent from a year earlier. Demand for software itself stays healthy: worldwide software spending is projected to reach about $1.44 trillion in 2026, up 15 percent and the second-fastest-growing category in technology.

Buyers are more selective than they were at the last market peak, and that works in favor of quality. When acquirers are disciplined, a defensible, payment-monetized vertical SaaS business does not get lost in the crowd; it stands out. Sellers with strong retention, clean financials, and real switching costs are the businesses that command attention and premium pricing in this kind of market.

Who Is Buying Vertical SaaS With Embedded Payments

Two kinds of buyers compete for businesses like this, and it helps to know what each wants. Strategic acquirers, such as FishPal, buy to extend their own product and reach. FishPal already owned booking demand and an audience, and Clubmate gave it the management software and payment rails to serve that audience more completely. Strategic buyers often pay up for a clean fit, because the acquisition makes their core business stronger.

Financial buyers, including private equity platforms, buy for durable cash flow and a path to grow it. They like recurring subscription revenue, the steady transaction income that embedded payments produce, and the option to add complementary products later. Both groups are active in 2026, and when a vertical platform with embedded payments comes to market, it can attract interest from both at the same time. That is the ideal setup for a seller, because competing buyers, rather than a single bidder, are what produce the best terms.

What Buyers Actually Reward: The Value Drivers

Buyers do not pay premiums for revenue alone. They pay for revenue that is durable, diversified, and hard to replace. A few drivers carry the most weight, and the Clubmate deal shows each one in action.

Workflow lock-in and switching costs come first. When a product runs a customer's daily operations, leaving is painful, so customers stay. That shows up as low churn and high net revenue retention, two of the metrics that move a SaaS valuation. Recurring revenue quality matters next: predictable monthly or annual income is worth far more than one-off sales, because a buyer can forecast it.

Embedded payments add a distinct layer of value. Payment revenue grows with customer activity rather than headcount, and it ties the customer even closer to the platform. Customer diversification helps too. Clubmate brought 380 vendors to the table, which spreads risk across many accounts instead of a few. Finally, buyers reward clean financials and a business that does not depend on the founder for day-to-day survival. The less a company leans on any one person, the more confident a buyer feels about life after the deal.

These drivers compound. Picture two software companies with the same revenue. One is a vertical platform with embedded payments, low churn, and revenue spread across hundreds of accounts. The other grows faster but serves a general market, leans on a handful of large customers, and depends heavily on its founder. In today's market, the first business usually draws more interest and a stronger price, because buyers can see exactly why its revenue will still be there in three years. Clubmate sat firmly in that first camp.

How to Position a Vertical SaaS Business for a Premium Exit

Most of the value in a sale is set before a buyer ever sees the business. Preparation, not timing, is what usually separates a strong outcome from an average one. A few moves make the biggest difference.

Start by separating and documenting your revenue. Show subscription income and payment income clearly, and track retention, churn, and net revenue retention over time. Reduce founder dependence by building a team and writing down how the business runs. Tidy the financials so earnings are easy to read, whether a buyer values on seller discretionary earnings for smaller companies or adjusted EBITDA for larger ones. These are core parts of preparing a software business to sell.

Then prove the moat. Document the integrations, compliance work, and workflow depth that make your product hard to replace, because that is what supports a premium multiple. When the business is ready, run a competitive, confidential process rather than negotiating with a single buyer. Competition is what surfaces the best price and terms. The Clubmate sale, brought to completion within 35 days of the signed letter of intent, shows how a focused process with the right buyers can move quickly once a business is well prepared.

It helps to picture what a buyer wants to find. A diligence-ready vertical SaaS business has clean monthly financials, a simple view of subscription and payment revenue, retention and churn tracked over at least a couple of years, key customer contracts in order, and clear documentation of how the product is built and run. The more of that you can show on day one, the faster a buyer gains confidence, and the less room there is to chip away at price later in the process.

Two Paths to Sell, Whatever Your Size

Not every business needs the same route to market, and the right path depends mostly on size.

For technology businesses valued at $1 million and above, full sell-side advisory is the strongest option. FE International runs the entire process, from valuation and preparation through buyer outreach, diligence, negotiation, and close. FE completes more $1 million to $100 million deals than any other advisor in the industry, with a 94.1 percent success rate across more than 1,500 transactions since 2010. That track record is why founders of larger, more complex businesses, Clubmate among them, choose to run a managed process.

For businesses under $1 million, FE International's M&A Platform is a great fit. It connects vetted buyers and sellers directly across SaaS, ecommerce, agencies, AI, cybersecurity, edtech, fintech, and marketplace apps. The M&A Platform works alongside full advisory rather than replacing it: it gives smaller businesses an efficient, lower-cost route to market, and it gives buyers a curated source of vetted deals. Both sides use it, which means a seller reaches real buyers and a buyer sees real businesses. Whatever the size of your company, there is a path that fits.

The Takeaway for Founders

The Clubmate sale is a clear signal of what buyers want in 2026: a vertical software platform that owns a real workflow and earns payment economics on top of its subscriptions. That combination produces durable, diversified, growing revenue, and it stands out in a market where buyers are selective and reward quality.

The wider conditions help too. M&A activity is strong, software demand is healthy, and embedded finance keeps expanding. For founders of vertical SaaS businesses, that adds up to a real opportunity to exit on good terms with the right preparation and the right process.

If you are weighing a sale, the first step is understanding what your business is worth. Talk to FE International for a confidential valuation and a read on the market. For businesses under $1 million, explore the M&A Platform to reach vetted buyers directly. Whatever the size of your company, there is a path to a strong outcome.