You built the business. Now you are weighing how to sell it, and the pitch for doing it yourself sounds simple: skip the fee, keep more of the proceeds, stay in control. The real question behind selling a business yourself vs an M&A advisor is not which option looks cheaper on paper. It is which option puts the most money in your pocket, on the best terms, with the least risk that the deal falls apart. Those are different questions, and the data answers them clearly.

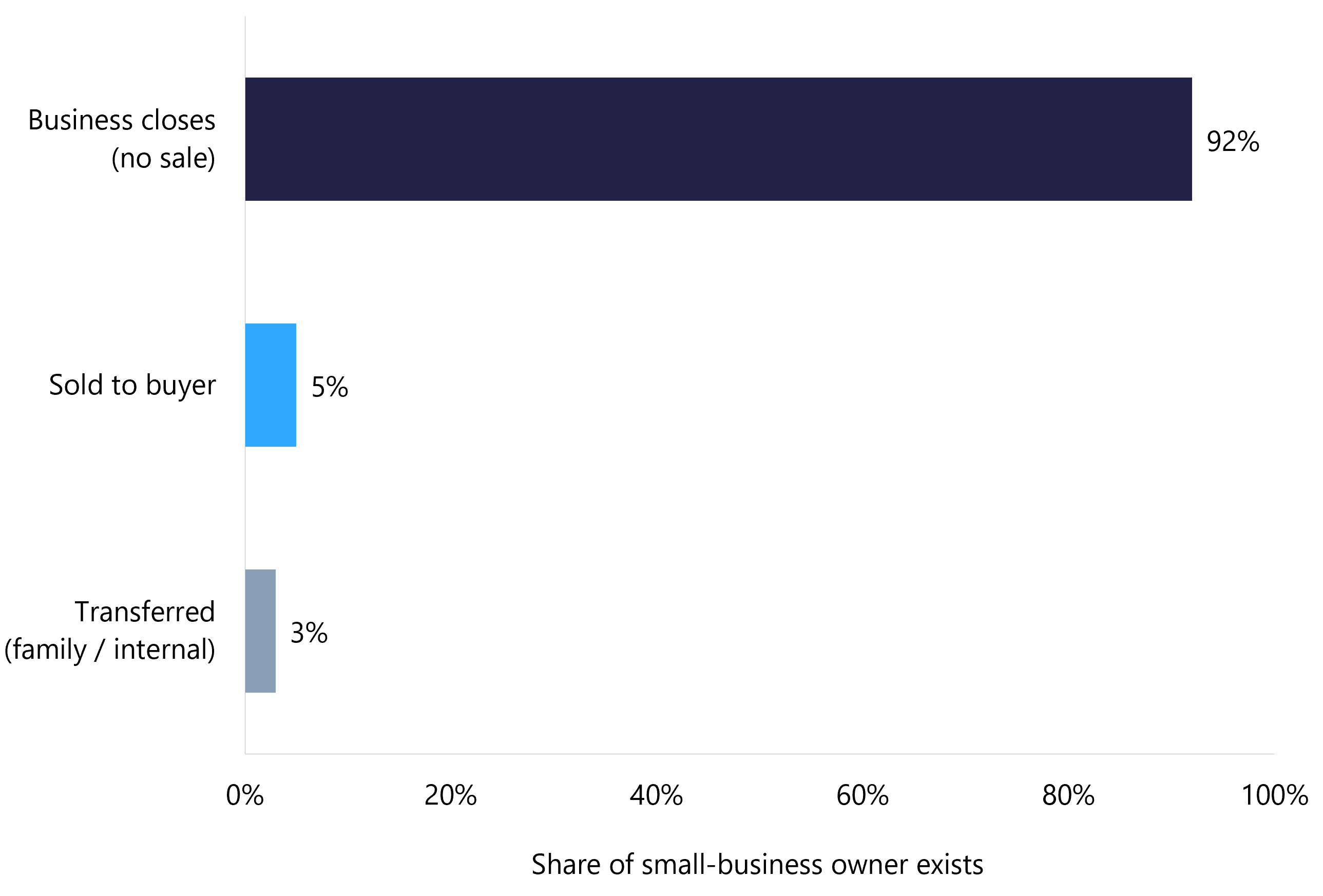

Here is the part most owners underestimate. A once-in-a-generation wave of business ownership transitions is now underway, with more than a million firms worth up to $5 trillion expected to be strong candidates for sale this decade. Yet only about 5% of owner exits are completed as a sale today. Getting to a clean, well-priced sale is the exception, not the default. This guide breaks down what a do-it-yourself exit actually costs, how an advisor-led process changes the outcome, and how FE International built a model, an advisory practice plus a self-serve M&A Platform, that fits both larger and smaller businesses.

Why 2026 Rewards Prepared Sellers

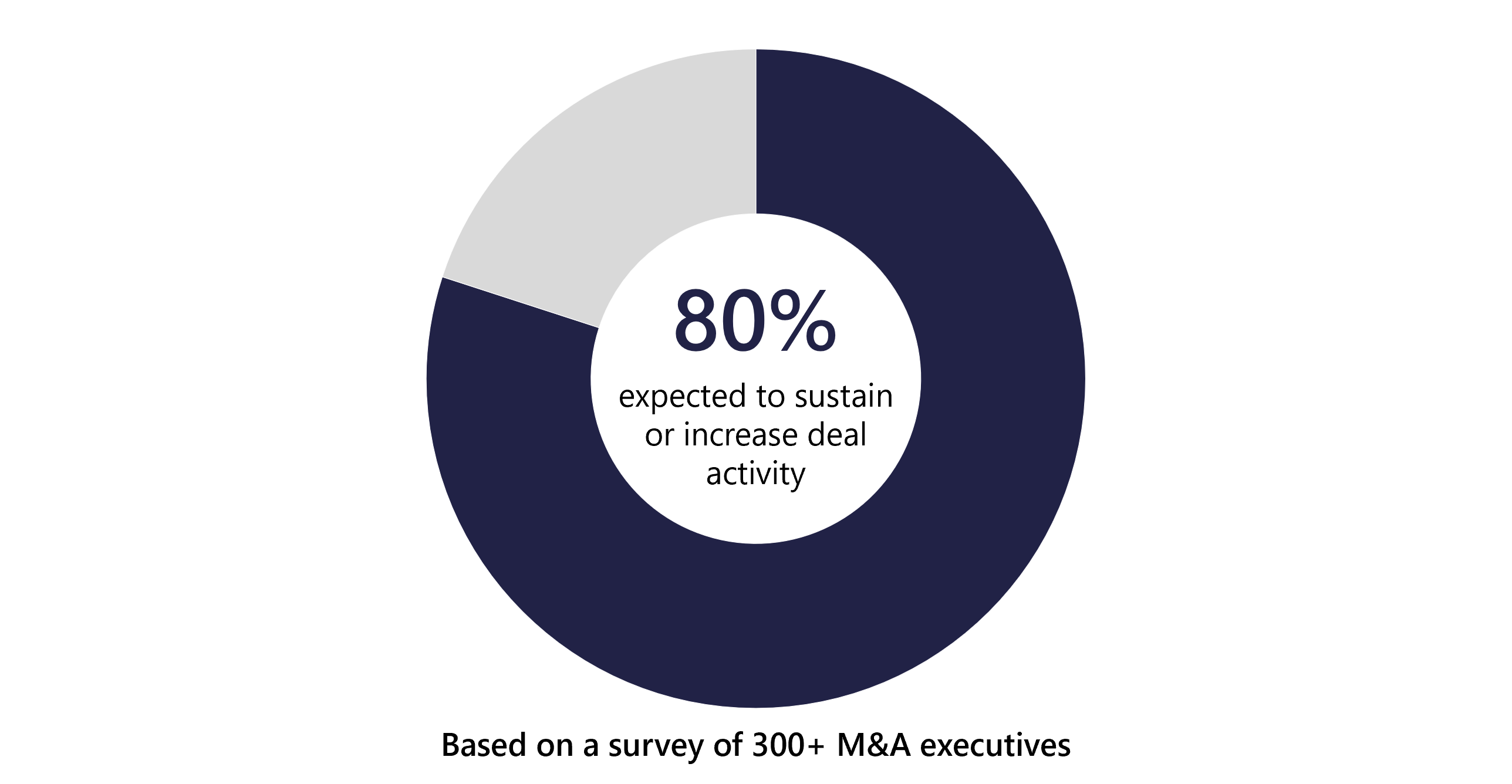

Start with the backdrop, because timing shapes everything that follows. Dealmaking is not slow or stuck. Global M&A reached a record $4.93 trillion in 2025, roughly 37% higher than the year before, and the first quarter of 2026 set a new quarterly record on top of it. Deal volumes closed 2025 at their highest level in four years. The mood among buyers points the same way: 80% of M&A executives expect to sustain or increase deal activity in 2026.

For technology owners, the signal is even stronger. Technology continues to drive the largest share of deal activity, tech M&A climbed sharply in the rebound, and roughly half of strategic technology deals now carry an AI angle. U.S. deal volume is forecast to keep growing through 2026. Buyers are active, capital is available, and the appetite for well-run software, ecommerce, and services businesses is real.

There is a catch that works in your favor if you prepare, and against you if you do not. Buyers in this market are selective. They move fast on businesses that are clean, well-documented, and credibly presented, and they pass on the ones that are not. A deep, active buyer market rewards the seller who shows up ready and reaches the full universe of acquirers. That is exactly where the gap between doing it yourself and running a professional process opens up.

Sell Your Business Yourself vs an M&A Advisor: The Two Paths, Side by Side

There are really three ways to take a technology business to market, not two. You can do it entirely yourself. You can hire a full-service advisor to run the whole process. Or, for smaller businesses, you can use a guided M&A Platform that gives you professional tooling and a real buyer network without a full engagement. Each path fits a different size and situation, and the smart move is matching the path to the deal rather than defaulting to whichever sounds cheapest.

To be fair to the DIY route: if your business is very small, simple, and you already have a credible buyer at the table, handling the sale yourself can work. The trouble is that most owners are not in that situation. They have one buyer or none, an asking price built on a rule of thumb, and a day job running the company. The table below lays out how the three paths stack up on the dimensions that actually move your outcome.

The choice is rarely FE versus you. It is which level of support fits the size and complexity of your deal.

What Selling It Yourself Actually Costs

A do-it-yourself sale is free only in the sense that you pay no advisory fee. The costs are real, they are just harder to see on an invoice. The biggest one is the price you leave on the table when no one is competing for your business.

The valuation gap from a single buyer

Price is set by competition, not by a calculator. When one buyer knows they are the only party at the table, they have no reason to stretch, and offers settle at the low end of the range. Peer-reviewed research on hundreds of takeover auctions found that running a competitive process, rather than a one-on-one negotiation, is linked to meaningfully higher prices for sellers, and the effect is strongest for smaller businesses. That last point matters: the founder-led and lower-middle-market deals where DIY is most tempting are exactly the ones where competition adds the most value.

The time, distraction, and performance cost

A sale is a second full-time job that lasts months. While you are writing memos, screening buyers, and sitting in diligence calls, someone has to keep the business growing. If revenue or margins dip mid-process, buyers notice, and a soft quarter during diligence can reset your valuation downward or sink the deal entirely. Many owners discover that the hours they spend trying to save a fee end up costing far more in lost focus and slipped numbers.

The buyer-pool limit

Your network is a fraction of the market. The buyer who pays the most is often a strategic acquirer or private equity platform you have never heard of, in a sector you do not track. Reaching that buyer takes a curated list, confidential outreach, and the credibility to get a reply. A public listing and a few personal contacts cannot replicate the reach of a vetted network of 80,000+ pre-qualified buyers.

The risk the deal simply never closes

This is the cost owners underestimate most. Getting to a completed sale is rare. Most owner exits end in closure rather than a sale, with only a small share completed as a transaction. Deals stall on diligence surprises, financing gaps, mismatched expectations, and terms that fall apart late. The figure below shows how owner exits actually end.

Terms, structure, and confidentiality

Price is one line in a deal. Earnouts, escrows, working-capital adjustments, representations and warranties, and the tax structure can swing your actual take-home by a wide margin. An owner negotiating their first deal often gives ground on these without realizing the cost. Confidentiality is its own risk: once customers, staff, or suppliers hear the business is for sale, relationships wobble, and that uncertainty can cost you both value and negotiating room.

DIY is not free. It trades a visible fee for invisible costs: a lower price, a longer timeline, and a real chance the deal never closes.

How an M&A Advisor Creates Value (and Why the Fee Pays for Itself)

A good advisor is not a paperwork service. The job is to engineer competition and protect the deal from the dozens of small failures that derail private sales. The mechanism is a structured, competitive process: a curated buyer list, a professional information memorandum, disciplined outreach to many qualified parties at once, and the tension that comes from several credible buyers knowing they are not alone. That tension is what lifts both price and terms, and it is the single hardest thing to recreate on your own.

FE International runs that process end to end. It starts with a data-driven valuation built on 1,500+ closed transactions, so the asking price is anchored in real deal data rather than a guess. A sector team prepares the materials and positions the growth story for the right buyers. Outreach goes to a vetted global network, and a dedicated senior advisor leads negotiation and deal structuring. In-house due diligence and in-house legal keep the deal moving through the stages where most private sales stall, and FE Capital Markets adds FINRA-registered investment banking for middle-market mandates that need it.

The buyer network is worth dwelling on, because it does more than add names to a list. A pre-vetted pool of buyers means the parties at your table are financially capable and genuinely interested, which cuts the time wasted on tire-kickers and lowers the odds of a deal collapsing late. It also means an advisor can reach acquirers who never publicly signal that they are buying, the strategic player quietly expanding into your category or the fund with a mandate that fits your business. Those buyers are usually invisible to an owner running a sale alone, and they are often the ones willing to pay the most.

Now the fee. A sell-side engagement typically combines a modest monthly retainer with a success fee tied to the final sale price and paid when the deal closes. The structure aligns incentives by design: the advisor earns their largest reward only when you get yours. The right way to weigh it is not fee versus zero. It is your net proceeds with a competitive process against your net proceeds without one. When a real process produces a higher price, cleaner terms, and a deal that actually closes, the value created routinely exceeds the fee, which is the whole point of hiring one.

Picture two identical businesses. One is sold quietly to the first buyer who makes a reasonable offer. The other is taken to market through a competitive process, where several qualified acquirers learn they are bidding against each other and each sharpens their offer to win. The second business almost always clears at a higher price and on cleaner terms, even though nothing about the company itself changed. The only difference is the process around it. That difference, repeated across thousands of deals, is what an advisor is actually selling.

The question is not whether you can avoid the fee. It is whether the price and certainty a process delivers are worth more than the fee. For most owners, they are.

M&A Advisor vs Business Broker vs Investment Banker

Owners often use these terms interchangeably, then end up with the wrong kind of help for their deal. They sit on a spectrum. A business broker typically handles Main Street sales, lists the business, and waits for a buyer. An M&A advisor runs a full sell-side process for lower-middle-market and mid-market companies, where value depends on competition and structure. An investment bank serves larger, more complex transactions and adds capital markets and underwriting.

The practical difference between a broker and an advisor is process. A broker finds a buyer; an advisor builds competition, manages diligence, and negotiates structure to maximize what you keep. The line between an advisor and an investment banker blurs in the middle market, where the same firm can do both. That is how FE is built. The advisory practice handles full sell-side M&A for technology businesses, and FE Capital Markets provides FINRA-registered banking, so a middle-market tech owner gets both capabilities under one roof rather than stitching together a broker, a lawyer, and a banker on their own.

The 94.1% Difference: What a Track Record Actually Means

Success rate is the number most self-serve options avoid publishing, because it answers the only question that matters when you list: how likely is it that my business actually sells? FE International reports a 94.1% success rate across more than 1,500 completed transactions, with combined deal value above $50 billion and a network of 80,000+ pre-vetted buyers. That figure is not a slogan. It reflects an operating model built around quality control at every stage of a sale.

A large part of why the rate is high is what FE declines. The firm turns away more than 90% of the businesses that approach it, taking on only mandates that pass pre-marketing diligence. That selectivity protects buyers, protects the firm's reputation, and, most importantly for a seller, means that when FE takes a business to market it is genuinely ready to sell. Discipline up front is what produces closings at the end.

The track record shows up in outside recognition too: FE has been named a Financial Times Fastest-Growing Finance Company in America for six consecutive years and an Inc. 5000 honoree for eight. Set that against the broader reality, where a completed sale is the exception rather than the norm, and the gap is stark. A 94.1% close rate is not a vanity metric. It is the difference between listing your business and actually selling it.

A track record is a forecast. Across 1,500+ deals, FE's 94.1% success rate is the closest thing a seller has to a reliable signal of how their own process will end.

Choosing Your Path: Advisory, the M&A Platform, or Both

Here is the part that resolves the whole DIY debate. With FE, you are not choosing between a full-service firm and going it alone. FE built two doors to the same outcome, sized to the value of your business, so the right level of support is always available.

Businesses worth $1M and up: full-service advisory

For technology businesses in the $1M to $100M+ range, full-service advisory is the strongest path. A dedicated senior advisor manages the entire transaction: valuation, a professional information memorandum, buyer outreach across the vetted network, negotiation, deal structuring, in-house legal, due diligence, and post-close transition. This is where a competitive process and experienced negotiation produce the largest gains, and where the value created comfortably outweighs the fee. The first step is a free, data-driven valuation.

Businesses under roughly $1M: the M&A Platform

For smaller businesses that do not need a full engagement, the FE International M&A Platform is the better alternative to selling entirely alone. It is self-serve, but you are not on your own: the platform covers valuation, listing creation, buyer discovery, outreach, and deal management, with access to the same pool of vetted buyers FE's advisory clients reach. You keep control and keep costs low, while still tapping a real buyer network and professional tooling that a solo listing cannot match.

Deciding between the two is less complicated than it sounds. Deal value is the main signal, but readiness matters too. If your business has meaningful scale, multiple value drivers, or any complexity in its revenue, customers, or structure, the hands-on guidance of full advisory tends to pay for itself. If it is smaller and more straightforward, the M&A Platform gives you the network and tooling to run a credible process yourself. A valuation settles the question quickly by grounding it in a real number rather than a guess.

The two paths are complementary, not competing. Same quality standards, same buyer network, different levels of hands-on support matched to deal value. If you are unsure where your business fits, start with a valuation and let the number guide the path. The point is simple: there is a smarter option than going it completely alone at every size, whether that is the M&A Platform for a smaller business or advisory for a larger one.

Selling a Technology Business Across Every Vertical

Buyers value a software company differently from an ecommerce brand, and an agency differently from a payments business. FE International is a technology M&A advisor across eight verticals, each with a dedicated team that knows the metrics buyers reward and the buyers who pay the most. A generalist selling on their own cannot speak each acquirer's language. Sector depth is where that knowledge turns into price.

- SaaS: recurring revenue, net revenue retention, the Rule of 40, churn, and gross margin drive value, with a clear premium for genuine AI capability. See the FE guide on how to value a SaaS business.

- Ecommerce and Consumer Products: brand strength, contribution margin, supply-chain resilience, customer acquisition cost, and repeat-purchase behavior shape buyer interest. Explore ecommerce and consumer products M&A.

- Agency and Marketing Solutions: retained versus project revenue, client concentration, EBITDA margins, and AI-enabled delivery separate a premium agency from an average one. See agency and marketing solutions M&A.

- Artificial Intelligence: defensibility, proprietary data, technical talent, and real product impact matter more than the label. Learn about AI company M&A.

- Cybersecurity: recurring contracts, retention, relevance to current threats, and compliance posture drive demand from strategics and sponsors. See cybersecurity M&A.

- EdTech: enrollment and engagement metrics, lifetime value per learner, and the mix of institutional versus consumer revenue shape valuation. Explore edtech M&A.

- FinTech: transaction volume, regulatory standing, and momentum in payments and embedded finance define buyer appetite. See fintech M&A.

- Marketplace Apps: gross merchandise value, take rate, liquidity, and network effects are the metrics buyers underwrite. Learn about marketplace apps M&A.

Whatever you have built, the case is the same: a team that knows your sector can position the business to the buyers most likely to pay a premium, then run a process that gets them competing. The right acquirer is often a strategic buyer looking to add your product line or customer base, or a private equity platform building in your space, and the two value a business in different ways. Knowing which buyers to approach, and how each one underwrites a deal, is difficult to do alone and central to what an advisor brings.

A DIY Business Sale Checklist (and Where Each Step Gets Hard)

If you want to understand the process before deciding how much help you need, here is the path a business takes to a successful sale, step by step, with the point where each step tends to trip up owners going it alone.

- Get a defensible valuation. Price the business on real data, not a rule of thumb. The hard part: set it too high and buyers walk; too low and you give away value before you start.

- Clean up financials and records. Prepare buyer-ready books, defensible add-backs, and clear recurring-versus-one-time revenue. The hard part: anything messy becomes a discount or a deal-breaker in diligence.

- Prepare the materials. Build a real information memorandum that tells a credible growth story, not a one-page summary. The hard part: presenting the business the way buyers underwrite it.

- Build a buyer list. Identify strategics, sponsors, and individuals who would pay a premium. The hard part: reaching buyers you do not know, confidentially, and getting a reply.

- Run outreach and create competition. Engage multiple qualified parties at once to build tension. The hard part: managing several conversations without leaking that the business is for sale.

- Qualify buyers and compare offers. Separate serious acquirers from tire-kickers and weigh offers on more than headline price. The hard part: comparing different structures apples to apples.

- Negotiate terms and structure. Work through earnouts, escrows, working capital, reps and warranties, and tax. The hard part: protecting net proceeds on terms a first-time seller rarely sees coming.

- Manage diligence and legal to close. Survive buyer diligence and definitive documents without losing momentum. The hard part: this is where most private deals stall or die.

Every step on that list is a place where a DIY seller can lose value or lose the deal. That is the case for support sized to your business: the M&A Platform gives smaller sellers the tooling and buyer access to handle these steps well, and full advisory runs all of them for you end to end.

Common Mistakes Owners Make When Selling Without an Advisor

The same handful of errors show up again and again in private sales, and most of them are expensive. The first cluster is about price and competition. Owners often anchor on what they need the business to be worth, or on a multiple they heard at a conference, rather than on a defensible valuation. Then they negotiate with a single interested buyer, which removes the one thing that reliably lifts price: tension between parties who know they have rivals. Price too high and the process stalls. Price too low, or sell to the only bidder in the room, and you hand value away before the real negotiation even begins.

The second cluster is about preparation. Messy books, undocumented add-backs, customer concentration that is never addressed, and a thin growth story all become discounts or deal-breakers the moment a serious buyer starts digging. A related mistake is taking your eye off the business while you run the sale. A soft quarter during diligence is one of the fastest ways to weaken your position, because buyers price the trend, not just the trailing numbers. Selling is demanding enough that doing it well usually means someone else is driving the process while you keep the company on plan.

The third cluster is about terms, confidentiality, and the finish line. Treating price as the only number, and ignoring earnouts, escrows, working-capital pegs, and tax structure, can quietly cost more than any fee. Letting word leak to staff, customers, or suppliers can spook the relationships that make the business valuable. And underestimating due diligence is how otherwise-good deals die in the final stretch. A structured process, whether through full advisory or the tooling and buyer access of the M&A Platform, exists precisely to keep these mistakes from happening.

The Bottom Line on a DIY Exit

Selling a business yourself vs an M&A advisor comes down to one honest comparison: not the fee you avoid, but the price, terms, and certainty you walk away with. A do-it-yourself exit trades a visible fee for a quieter set of costs, a lower price with no competition, a months-long distraction from running the company, a smaller buyer pool, and a real chance the deal never closes. The fee is the number you can see; the value left on the table is the number you cannot, and for most owners it is far larger. In a record M&A market, the businesses that capture the most value are the ones that arrive prepared and reach every qualified buyer.

FE International gives you a path at every size. For a technology business worth $1M or more, advisory runs a competitive, end-to-end process backed by a 94.1% success rate, $50B+ in closed deals, and 80,000+ vetted buyers. For a business under roughly $1M, the M&A Platform gives you that same network and professional tooling on a self-serve basis. Either way, the smart first move is the same: get a free, data-driven valuation and start the conversation with a team that has done this more than 1,500 times.