.png)

You've agreed a headline number with your buyer. Hands have been shaken, LOIs signed, and the deal feels real. Then your M&A advisor mentions that you still need to agree on the “pricing mechanism” and suddenly the conversation turns to locked boxes, closing accounts, leakage, ticking fees, and working capital pegs.

Don’t worry: this is completely normal, and it matters more than most sellers realize.

The pricing mechanism isn’t just a legal formality. It determines when the final price gets fixed, who bears the risk if the business fluctuates between signing and closing, and ultimately how much cash lands in your bank account on day one. Getting it wrong or simply not understanding what you’ve agreed to, can mean a painful post-closing adjustment that reduces your payout by hundreds of thousands of dollars.

This article explains how both mechanisms work, what the tradeoffs are for sellers of online businesses, and how to approach the negotiation.

Why the Gap Between Signing and Closing Creates a Problem

In most acquisitions, there’s a gap, sometimes weeks, sometimes months, between when the purchase agreement is signed and when the deal actually closes. During this window, lawyers are finalizing documents, lenders are completing financing, and the parties are working through due diligence and any regulatory requirements.

The business keeps running. Cash comes in, expenses go out, headcount changes, and customer contracts tick along. By the time closing day arrives, the financial profile of the business looks at least somewhat different from when the price was agreed.

This creates a fundamental question: who owns that value, and who bears that risk?

Both the locked box mechanism and closing accounts are answers to that question. They just take opposite approaches.

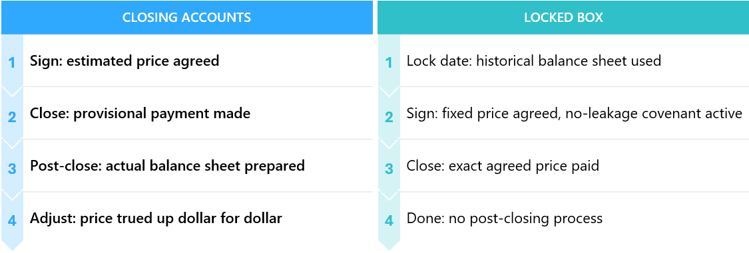

Closing Accounts: The Standard US Approach

Closing accounts (sometimes called “completion accounts” in cross-border transactions) are the dominant method in US M&A. The core idea is simple: the final purchase price is adjusted after closing to reflect the actual financial position of the business on the day the deal closes.

How It Works

1. Agree a preliminary price at signing. The parties negotiate a headline enterprise value and then estimate the key balance sheet items, usually cash, debt, and working capital, that will be used to calculate the equity price. This estimate gets built into the purchase agreement.

2. Close the deal. The buyer pays the estimated equity price on closing day. But this is explicitly understood to be a provisional number.

3. Prepare the closing accounts. In the weeks after closing, one party (typically the buyer, since they now control the business) prepares a set of financial statements as of the closing date. These capture the actual cash, debt, and working capital at that moment.

4. Calculate the adjustment. The closing accounts are compared against the estimates used at signing. If the business had more working capital at closing than estimated, the buyer pays the seller more. If it had less, the seller pays the buyer back, dollar for dollar. The same logic applies to cash and debt positions.

5. Dispute resolution. If the parties disagree on the closing accounts, the purchase agreement will set out a procedure, typically involving an independent accounting firm as expert determiner, to resolve the dispute.

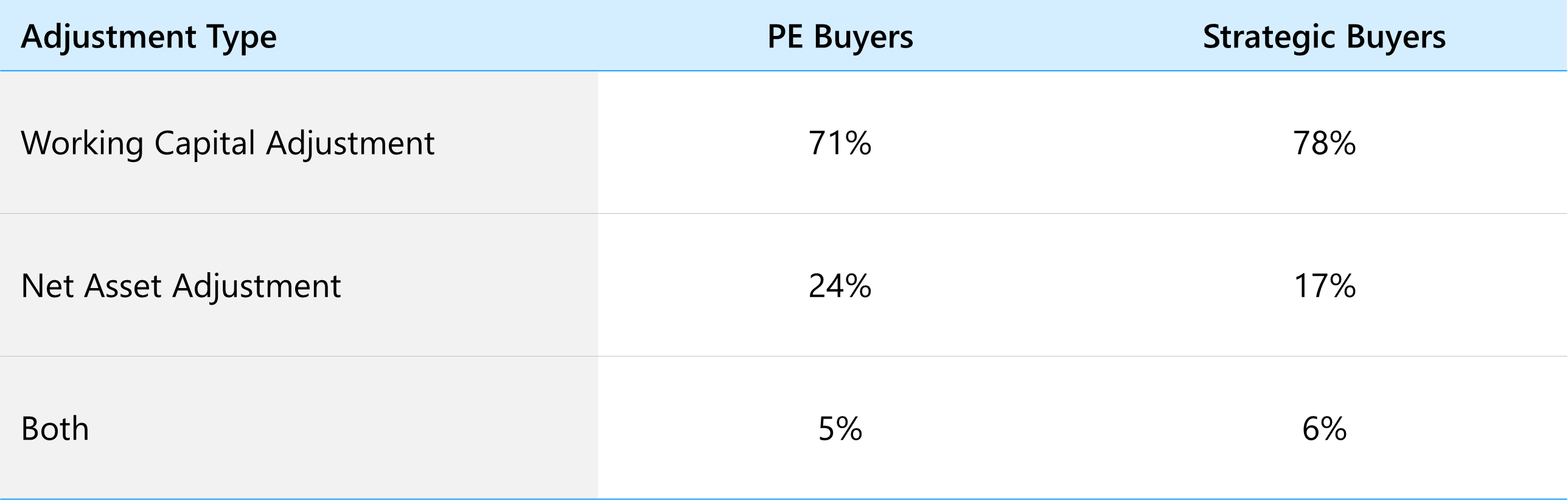

The Working Capital Peg

The most important and often most contentious element of closing accounts is the working capital peg. The parties agree a “target” level of working capital that the seller is expected to deliver at closing, typically calculated as the average working capital the business has maintained over the trailing twelve months.

If working capital comes in above the peg, the seller gets paid more. If it comes in below, the seller pays back the difference, dollar for dollar.

For SaaS businesses, this negotiation can be genuinely complex. Working capital in subscription businesses doesn’t behave the same way it does in traditional product companies. Deferred revenue, timing of annual contract billings, and fluctuating accounts receivable balances all affect the calculation. Getting the peg right requires detailed historical analysis, and disputes are common.

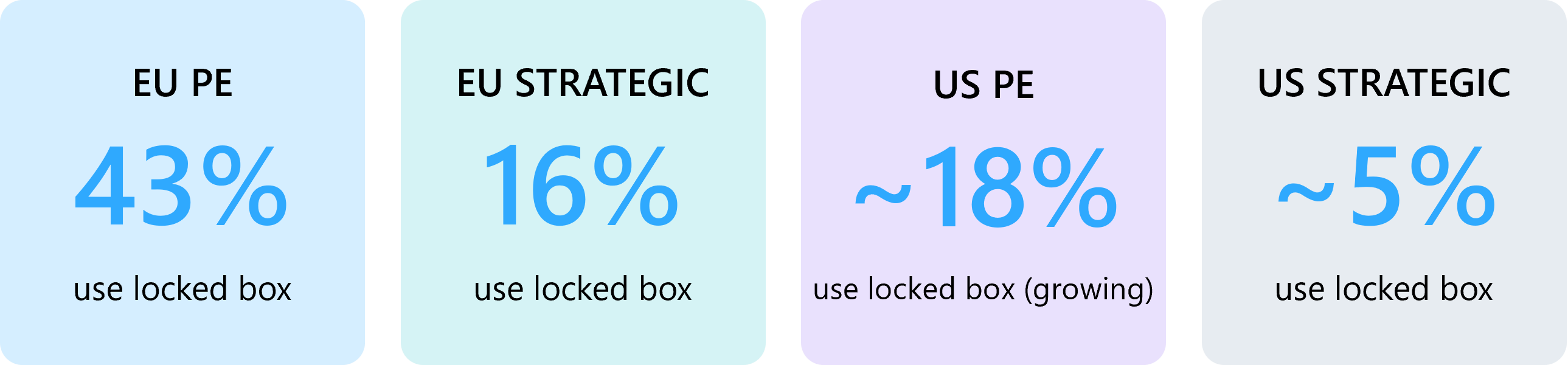

European PE & Strategic transactions, 2025- indicative of growing US practice

Case Study – Project bird

A SaaS business with $28M in annual revenue was acquired for an enterprise value of $144M. The parties estimated the working capital peg at $2.3M. At closing, several large annual contracts renewed in the week before closing, pushing deferred revenue higher and net working capital below the peg by $900K. The seller received $141.1M instead of the $144M headline price, a $900K haircut they hadn’t anticipated when signing the LOI.

The Locked Box: A Cleaner Alternative

The locked box mechanism flips the logic entirely. Rather than adjusting the price after closing, the parties agree on a fixed price at signing, and that price doesn’t change, regardless of what happens to the balance sheet between then and closing day.

To achieve this, the parties pick a reference date in the past, the “locked box date” and use the balance sheet as of that date to calculate a definitive equity value. From that point on, economic risk and reward in the business transfers conceptually to the buyer, even though they don’t take legal ownership until closing.

How It Works

1. Choose the locked box date. This is typically the most recent date for which reliable, audited (or at minimum internally prepared) financial statements exist, often the most recent fiscal year-end or quarter-end.

2. Agree the price. The parties negotiate the equity value based on that locked box balance sheet. Cash, debt, and working capital are all “determined” from those historical financials rather than estimated. Because the numbers already exist, there’s less to argue about.

3. Sign the deal. The price is fixed. Both parties know exactly what the final number is. There is no post-closing adjustment mechanism.

4. The seller doesn’t touch the money. Between the locked box date and closing, the seller is contractually prohibited from extracting value from the business. No dividends, no related-party transactions, no unusual management fees. This protection, called the “no leakage” covenant, is what makes the fixed price work.

5. Close the deal. The buyer pays exactly the agreed price. Done.

The locked box is gaining traction in US deals, particularly in competitive auction processes and larger transactions where sellers have the leverage to push for certainty of price.

A European Playbook; Now Coming to the US

The locked box isn’t a new concept, it has been the preferred structure for private equity transactions in Europe for well over a decade. If you want to understand where the US market is heading, looking at European deal practice gives a clear preview.

In European PE, the locked box is effectively the default. Sellers running competitive auction processes routinely demand it, PE buyers are thoroughly fluent with the mechanism, and the legal infrastructure around leakage covenants is well-established. Across the Netherlands, Germany, Ireland, and Spain, locked-box structures are described as “standard” across mid-market transactions.

The US market is earlier in this adoption curve, but the direction is clear. Cross-border PE activity, the globalization of M&A advisory firms, and the growing sophistication of both sellers and their advisors are all accelerating familiarity. US PE buyers who regularly transact in Europe now carry those deal norms home. And sellers with experienced advisors are increasingly willing to push for the certainty that locked box provides.

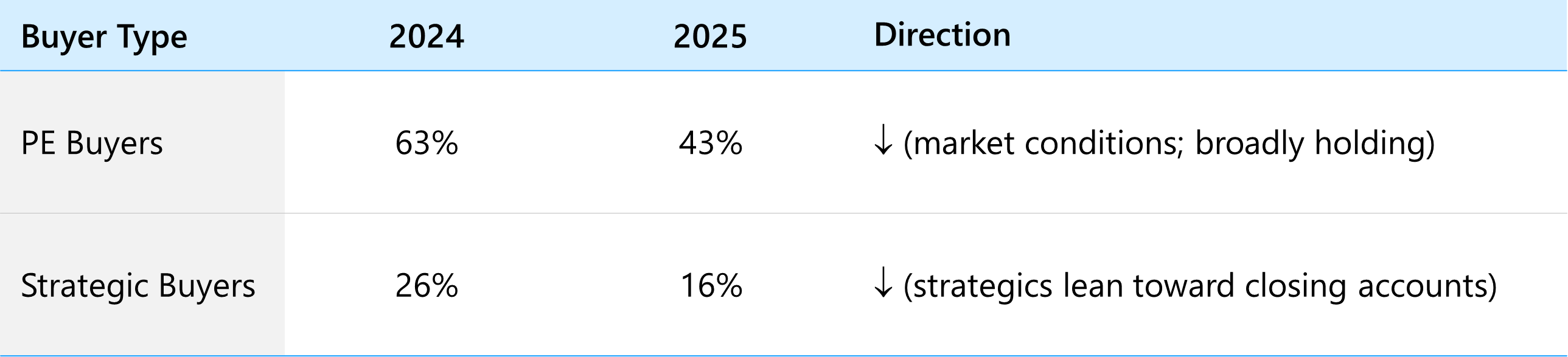

Illustrating buyer-type divergence and year-on-year trend

“PE buyers particularly like the certainty a locked box structure gives the parties, allowing management teams to look forward without the distraction and potential misalignment around a completion accounts true up. Sellers also favor locked box as it can provide certainty on the proceeds they will be receiving.” (M&A and PE Market Trends Report 2026)

The gap between PE and strategic buyers is instructive. Strategic buyers, corporates with deep operational knowledge of their target sectors, are often more comfortable with closing accounts because they understand the working capital dynamics well enough to negotiate them effectively. PE buyers, who depend on certainty of price and clean management focus, lean toward locking the box. As the US middle market becomes increasingly PE-influenced, locked box adoption is following.

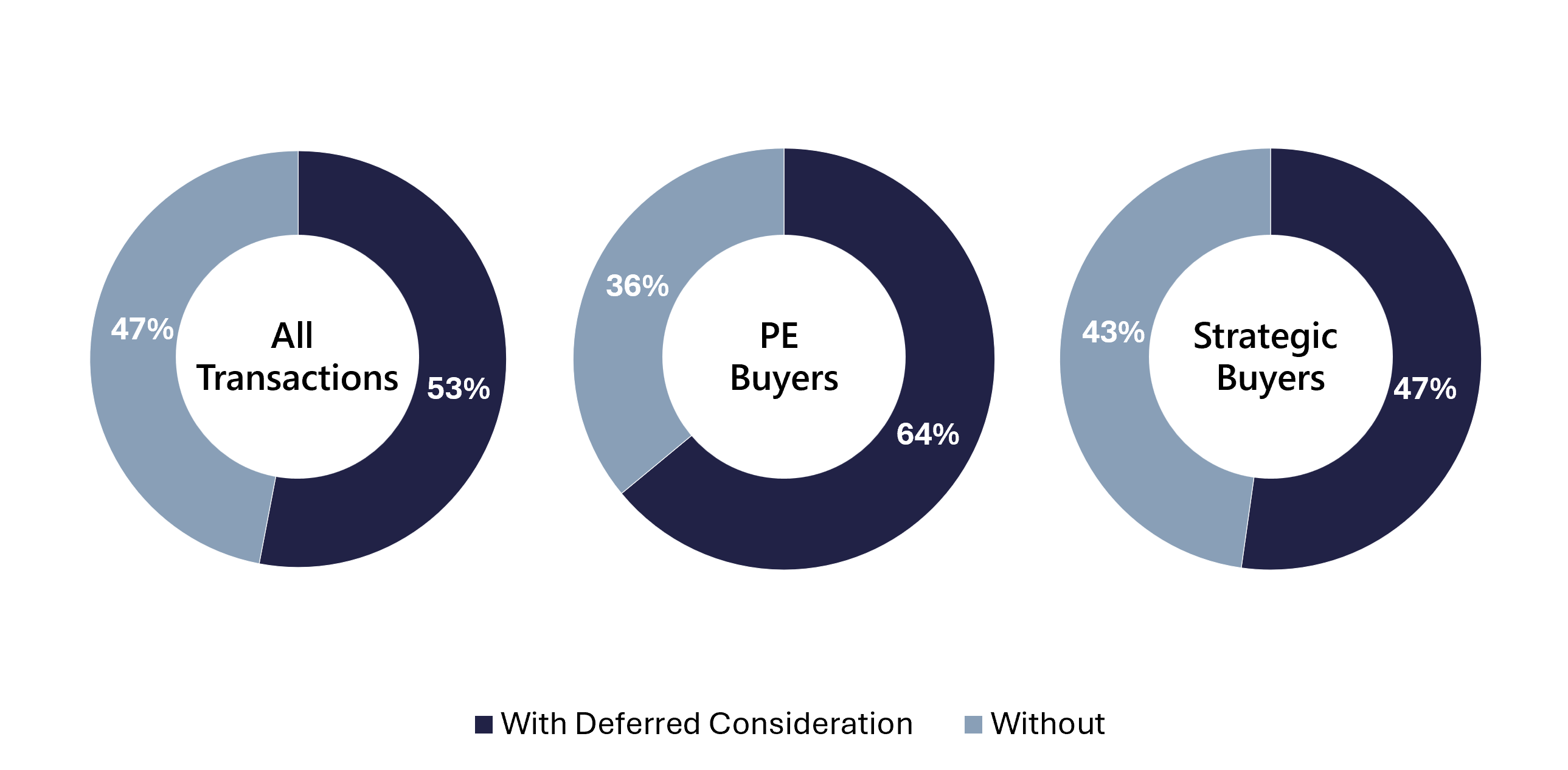

% of transactions including earn-out / deferred consideration- European market, 2025

One related trend worth noting for US sellers: deferred consideration, earn-outs and seller notes, is becoming more prevalent on both sides of the Atlantic as buyers look for ways to bridge valuation gaps. In 2025, 64% of PE transactions included some form of deferred consideration. Understanding how earn-outs interact with your pricing mechanism is an important part of structuring a deal that protects your interests at every stage.

Understanding Leakage (And Why It’s the Crux of the Negotiation)

The locked box mechanism only works if the seller genuinely can’t extract value from the business after the locked box date. If they could, they’d be incentivized to strip out cash and assets before closing, having already locked in a high price based on a healthier balance sheet.

The purchase agreement therefore contains a detailed definition of “leakage”, the categories of value transfer that are prohibited, along with a dollar-for-dollar indemnity: if the seller causes any leakage, they must repay it to the buyer in full.

Leakage typically includes:

- Dividends or distributions paid to shareholders

- Payments or loans to related parties above normal commercial rates

- Bonuses or compensation to management beyond what’s ordinary course

- Waivers of amounts owed to the company by sellers or their affiliates

- Any transaction not conducted on arm’s-length terms

Not everything is prohibited. The parties also agree a list of “permitted leakage”, items expected to occur in the normal course that have been disclosed and priced in. Salary payments, routine vendor invoices, and pre-agreed management fees would typically fall here.

Negotiating the leakage definition is often where the real complexity lies in a locked box deal. Sellers want the permitted leakage basket to be as broad as possible; buyers want it as tight as possible. Getting this right requires careful legal drafting and a clear picture of all related-party arrangements before the deal is agreed.

Case Study — SaaSGrow

A bootstrapped SaaS business with $11M ARR signed a deal with a locked box date of December 31. The deal didn’t close until March. During that period, the founder approved a $500K retention bonus for himself, reasonably assuming it fell within normal compensation. The buyer argued it constituted unauthorized leakage and sought a dollar-for-dollar deduction at closing. The dispute was ultimately resolved with the founder absorbing $300K of the adjustment , a painful outcome that clearer permitted leakage drafting could have avoided entirely.

Ticking Fees and Value Accrual: Compensating the Seller for the Gap

One apparent disadvantage of the locked box for sellers is that economic risk technically passes to the buyer from the locked box date, not from closing. If the business performs well during the gap, the buyer benefits, they’ve been enjoying the economic upside while the seller still carries the operational burden.

To address this, deals frequently include a ticking fee (also called a “value accrual”). This is a daily or monthly credit that accrues from the locked box date to closing, added on top of the headline price to compensate the seller for the time value of the equity they’re effectively holding on the buyer’s behalf.

Interest-based accrual: A daily rate applied to the equity value, effectively functioning like an interest payment. Common rates sit somewhere between a market reference rate and an agreed fixed percentage.

Cash flow accrual: The parties agree that the buyer will compensate the seller for the net cash generated by the business between the locked box date and closing, reflecting the economic upside the buyer is receiving before they’ve actually taken ownership.

For with short deal timelines (often 60–90 days from LOI to close with FE International), ticking fees are less common. In larger deals with extended financing or regulatory review periods, they can become a meaningful component of total consideration.

Closing Accounts vs. Locked Box: Which Is Better for Sellers?

There’s no universally correct answer; it depends on deal circumstances, leverage, and how confident you are in your financial position. But here’s an honest breakdown from a seller’s perspective.

The Case for the Locked Box

- Certainty.

You know exactly what you’re getting paid on closing day. There’s no post-closing negotiation, no accountants arguing over accruals, no waiting months for a final number. For most founders, the psychological value of a clean exit is significant.

- Speed and simplicity.

Locked box deals tend to close faster because the closing accounts process, which can take weeks and attract genuine disputes, is eliminated entirely. Fewer advisors spend fewer hours arguing about numbers.

- Seller-friendly in a competitive process.

If you’re running a competitive auction with multiple bidders, the locked box signals that you’re a clean seller with transparent financials. Buyers in competitive processes often prefer it because it removes post-closing uncertainty for them too.

- You keep the upside.

If the business performs strongly between signing and closing, strong ARR growth, a new customer win, that value is already baked into the price the buyer agreed to pay. You won’t give any of it back.

The Case for Closing Accounts

- Protection if the business is volatile.

If your business has lumpy cash flows, seasonal swings, or a key customer renewal coming up, closing accounts protect the buyer from paying a price that doesn’t reflect reality on closing day. This is a reasonable protection to offer. and most US buyers will simply expect it.

- More familiar to buyers, lenders, and counsel.

Closing accounts are the default in US M&A. Particularly at the lower end of the market (sub-$20M transactions), buyers, their lenders, and their legal teams are set up for this process. Introducing a locked box can add friction if advisors aren’t experienced with it.

- Appropriate when your reference-date financials are unreliable.

If your most recent financials are internally prepared rather than reviewed or audited, or if there have been significant changes since those financials were produced, a locked box based on those figures may actually disadvantage you.

Which Mechanism Do Buyers Prefer?

Private equity buyers are increasingly comfortable with the locked box in competitive auction processes. They’ve done the diligence, they understand the business, and they often prefer the certainty of a fixed price at closing over the administrative drag of post-closing accounts. Larger PE-backed deals, particularly those with a well-organized sell-side process, are where you’re most likely to see a locked box succeed in the US market.

Strategic buyers are more mixed. Corporates acquiring businesses to integrate into their own operations often want the protection of closing accounts, particularly if there’s meaningful integration activity between signing and closing that might affect working capital or headcount.

Individual buyers and first-time acquirers in the SMB space almost always default to closing accounts because that’s what their advisors are built for. This is one area where having an experienced sell-side advisor genuinely changes outcomes, an advisor like FE International can educate buyers who haven’t encountered a locked box before and help structure the mechanism that best serves your interests.

Practical Guidance for Online Business Founders

Get your financials in order before the locked box date is set. If you’re going down the locked box route, the quality of your balance sheet on the reference date is everything. Clean up intercompany balances, make sure deferred revenue is correctly recorded, and ensure your cash and debt positions are unambiguous. Ambiguity on the locked box balance sheet creates exactly the kind of dispute you were trying to avoid.

Model the working capital peg carefully if using closing accounts. Don’t just accept the buyer’s proposed peg without running your own analysis. Look at your trailing twelve months of working capital, identify any seasonal patterns, and make sure the peg reflects a genuinely representative level, not a high-water mark that creates a structural risk of a downward adjustment at closing.

Read the leakage definition carefully. Many sellers don’t engage with this carefully enough at the LOI stage. If you have related-party arrangements, owner-operator compensation structures, or anything that might not be obviously “ordinary course,” surface these early and get them into the permitted leakage basket before the legal process begins.

Push for a ticking fee if the deal timeline is long. If closing is expected to take more than 60 days from the locked box date, make sure you’re compensated for the gap. A ticking fee of even 6–8% per annum on the equity value can add meaningfully to total consideration if the deal runs long.

Don’t let the mechanism distract from the headline number. It’s easy to spend so much energy negotiating the mechanism that you lose sight of whether the enterprise value itself is right. The mechanism matters, but it matters less than the multiple you’re being offered. Make sure your advisor is benchmarking your deal against comparable transactions.

A Note on Dispute Resolution

One thing both mechanisms have in common: disputes happen. Working capital disagreements, leakage indemnity claims, and debates over the completeness of locked box accounts are genuinely common in M&A, even on well-run deals.

The purchase agreement will set out a dispute resolution process, typically involving submission to an independent accounting firm (often called an “expert determiner” or “neutral accountant”) whose decision is binding on both parties. This process is not cheap and not fast. Both sides engage their own accountants to prepare submissions, and the expert determination process can take months.

This is one reason why involving experienced M&A advisors from the outset, not just attorneys but financial advisors who understand how these disputes tend to play out, is worth the cost. Disputes that could have been avoided with better drafting at the LOI stage can become very expensive to resolve after signing.

Ready to discuss your exit?

Navigating pricing mechanisms is one of the areas where having the right advisory team makes a concrete, measurable difference to your outcome. The nuances of leakage definitions, working capital pegs, and ticking fee calculations are genuinely technical, and small differences in how they’re negotiated can move the final payout by hundreds of thousands of dollars.