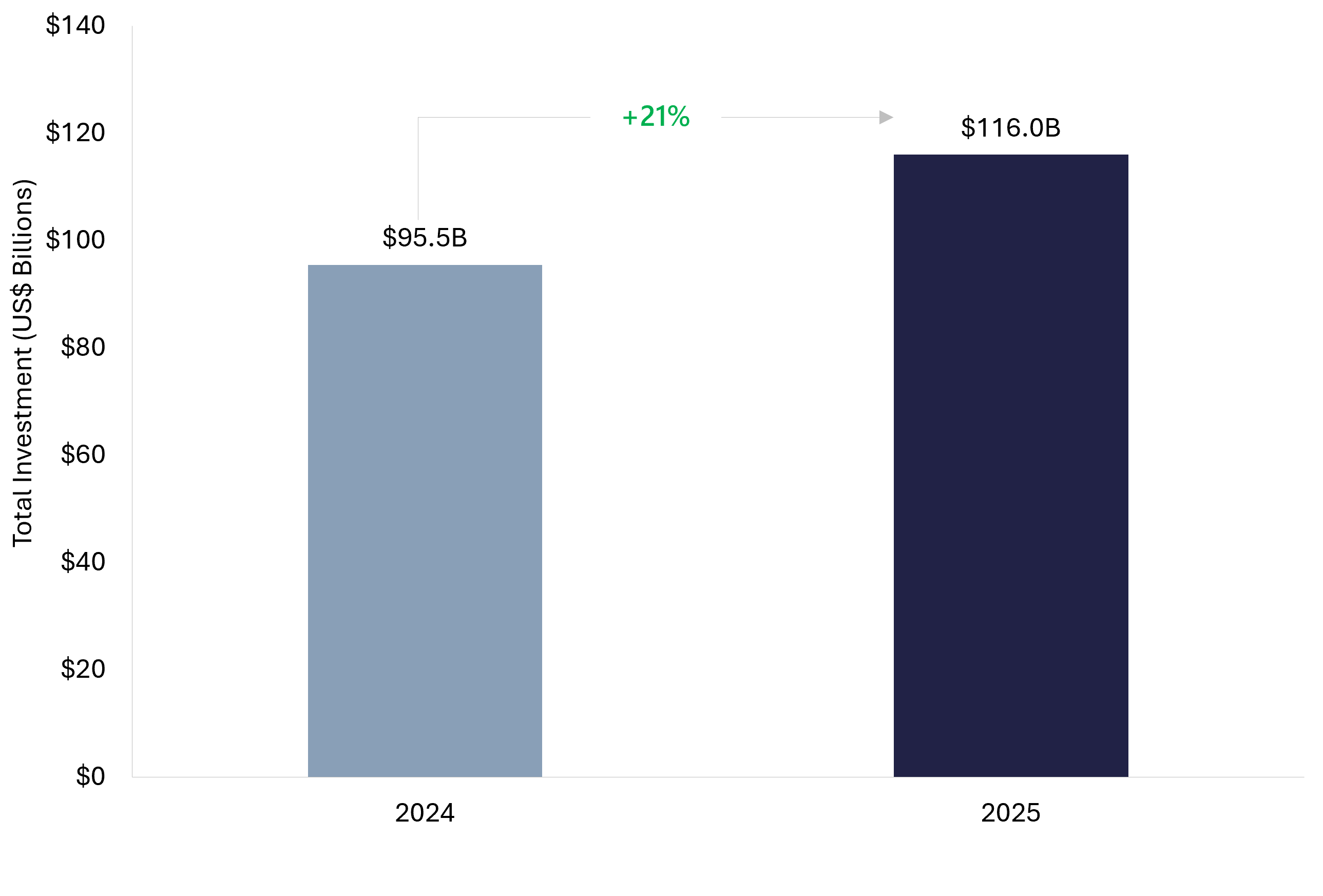

The fintech M&A outlook 2026 is the strongest it has looked in years, and the data backs it up. Global fintech investment climbed to $116 billion in 2025, up from $95.5 billion the year before. Financial services M&A reached $113 billion, a 15 percent jump over 2024. Disclosed fintech exit value hit $67.6 billion, its highest level outside of 2021. The pattern is clear: capital is back, buyers are active, and the businesses that are ready to transact are finding a deep pool of well-funded acquirers.

For founders and investors in payments, embedded finance, wealthtech, regtech, and the wider fintech ecosystem, that shift matters. The 2022 to 2023 slowdown has given way to a market defined by conviction. Acquirers are paying real premiums for businesses with durable revenue and clear strategic fit, and three forces are pulling deals forward at once: embedded finance moving from pilot to revenue line, payments consolidating into scaled platforms, and AI rewriting what a financial product can do.

This guide breaks down where deal activity is concentrated, what is driving valuations, who is buying, and how founders can position a fintech business to capture the best possible outcome. It is built for owners weighing an exit and for buyers building a thesis. FE International advises on technology M&A across the full fintech spectrum, and for smaller businesses the FE International M&A Platform offers a streamlined path to the same buyer pool. Here is what the year ahead looks like.

The 2026 Setup: Capital Is Back and Moving With Conviction

The headline story of the fintech M&A outlook 2026 is a market that has found its footing. After several years of recalibration, global fintech funding rose to $52.7 billion in 2025, a 35 percent increase over the prior year and the highest annual total since 2022. The rebound was not evenly spread, and that is the interesting part. Deal counts came down while the dollars per deal went up. The average fintech deal grew to roughly $20 million, and mega-rounds made up 63 percent of fourth-quarter funding. Investors are writing bigger checks to fewer, more proven companies.

That same discipline shows up in M&A. Financial services dealmaking grew 15 percent year over year, and consolidation is expected to continue into 2026. On the venture side, fintech deal value reached $42.8 billion, the highest since 2022, and exit value climbed to $67.6 billion as the IPO window reopened and strategic buyers returned. Six US fintechs went public early in the cycle, raising about $3.2 billion, the strongest showing in at least a decade.

What does this mean for a founder or a buyer? The "growth at any cost" era has been replaced by a focus on unit economics, profitability, and clean operations. That is good news for well-run businesses. When acquirers reward quality, the companies that have done the work, recurring revenue, healthy margins, documented compliance, stand out and command attention. The watchwords for 2026 dealmaking are smaller and more strategic, which favors operators who can show a clear path to value rather than a story about future scale.

The buyer pool is also broadening. Strategic acquirers, private equity platforms, and traditional banks are all active, each for different reasons. We see this pattern repeatedly in our own deal flow: a prepared business with a clean data room and a defensible niche attracts multiple bidders, and competition is what produces a premium outcome. For founders, the takeaway is simple. The conditions that make 2026 a strong year to sell are the same conditions that reward preparation.

Embedded Finance: The Trillion-Dollar Engine Behind Fintech Valuations

If one trend is shaping fintech dealmaking this year more than any other, it is embedded finance. The idea is straightforward: financial services such as payments, lending, and insurance are built directly into the software and platforms people already use, rather than accessed through a separate bank or app. The scale is hard to overstate. Embedded finance accounted for roughly $2.6 trillion of US financial transactions in 2021, and that figure is projected to exceed $7 trillion by 2026, more than 10 percent of all US transaction value. Revenue for the software platforms and infrastructure providers powering these services is on track to grow from about $21 billion to $51 billion over the same period.

Europe tells a similar story. Embedded finance revenue there could surpass €100 billion by the end of the decade and account for 10 to 15 percent of banking revenue pools. Over the last decade, embedded finance volumes in Europe grew three times as fast as directly distributed loans. This is a structural shift in how financial products reach customers, and it has direct consequences for M&A.

Here is why it drives deals. A software platform that wants to add payments or lending has two options: build the capability over years, or buy a company that already has the infrastructure, licenses, and compliance in place. More often than not, buying is faster and cheaper. That dynamic makes embedded-finance infrastructure businesses some of the most sought-after targets in the market. Companies that own the rails, the ledger, the licensing, or the risk models sit in a strong position.

For founders, the lesson is about positioning. A fintech that can show it makes another platform’s product stickier, that brings proprietary data, distribution, or a hard-to-replicate license, is not just selling revenue. It is selling a strategic capability, and those are the businesses that attract premium interest. Embedded finance also rewards niche specialists: a company serving a specific vertical, whether that is healthcare payments, SME lending, or insurance for a particular industry, can be exactly the piece a larger acquirer needs to enter that market.

Consolidation in this space tends to accelerate innovation rather than slow it. When infrastructure providers combine, the resulting platforms can fund deeper product development and reach more customers, which pulls even more software companies into offering financial services. For owners of embedded-finance businesses, that means a growing field of motivated buyers and a clear strategic story to bring to the table.

Payments: The Highest-Volume Corner of Fintech M&A

Payments remain the busiest category in fintech M&A, and the deals are getting larger. The clearest signal came when Global Payments acquired Worldpay in a transaction valued at $24.25 billion, announced in 2025 and completed in early 2026 at roughly 8.5 times EBITDA. The combined business processes around 94 billion transactions and $3.7 trillion in volume across more than 175 countries, serving merchants from small businesses to global enterprises. Deals of that size reset expectations for the whole sector and signal real confidence in the long-term economics of payments.

The activity is not limited to mega-deals. Cross-border payments remain expensive and fragmented in many corridors, which creates a steady stream of acquisitions as larger players buy local rails and compliance infrastructure in high-growth markets. Smaller, faster transactions of this kind move quickly because they often sit below regulatory review thresholds. For founders of payments businesses with strong regional positions or specialized capabilities, that is a meaningful pool of strategic buyers.

Why do payments attract so much M&A interest? The revenue is transaction-based and recurring, which makes it predictable and scalable. A processor that adds volume sees revenue grow with little additional cost. Acquirers value that operating leverage, and they value the network effects that come with scale: more merchants attract more partners, which attracts more merchants. Established payments operators with healthy margins are among the most reliably acquired businesses in fintech.

The strategic logic runs deeper than scale. Payments sit at the center of the embedded finance shift, the move toward real-time settlement, and the rise of digital-asset rails. A payments company is often the entry point for a larger institution that wants to reach a new customer segment or geography. That is why card networks, large processors, and banks keep payments acquisitions near the top of their priority lists heading into 2026.

There is also a clear pull toward business-to-business payments. Accounts-payable automation, spend management, and treasury tools have become priority targets as companies digitize their finance functions, and the recurring software revenue attached to these products makes them especially attractive. Real-time settlement is reshaping expectations on both sides of a transaction, and the operators that can move money instantly and reconcile it cleanly are well placed. For a founder, owning a specific workflow that larger players want to offer is often worth more than competing on raw processing volume.

Payments revenue is transaction-based, recurring, and scalable, which makes established payments businesses among the most reliably acquired companies in fintech.

AI and Agentic Payments: The New Premium in Fintech

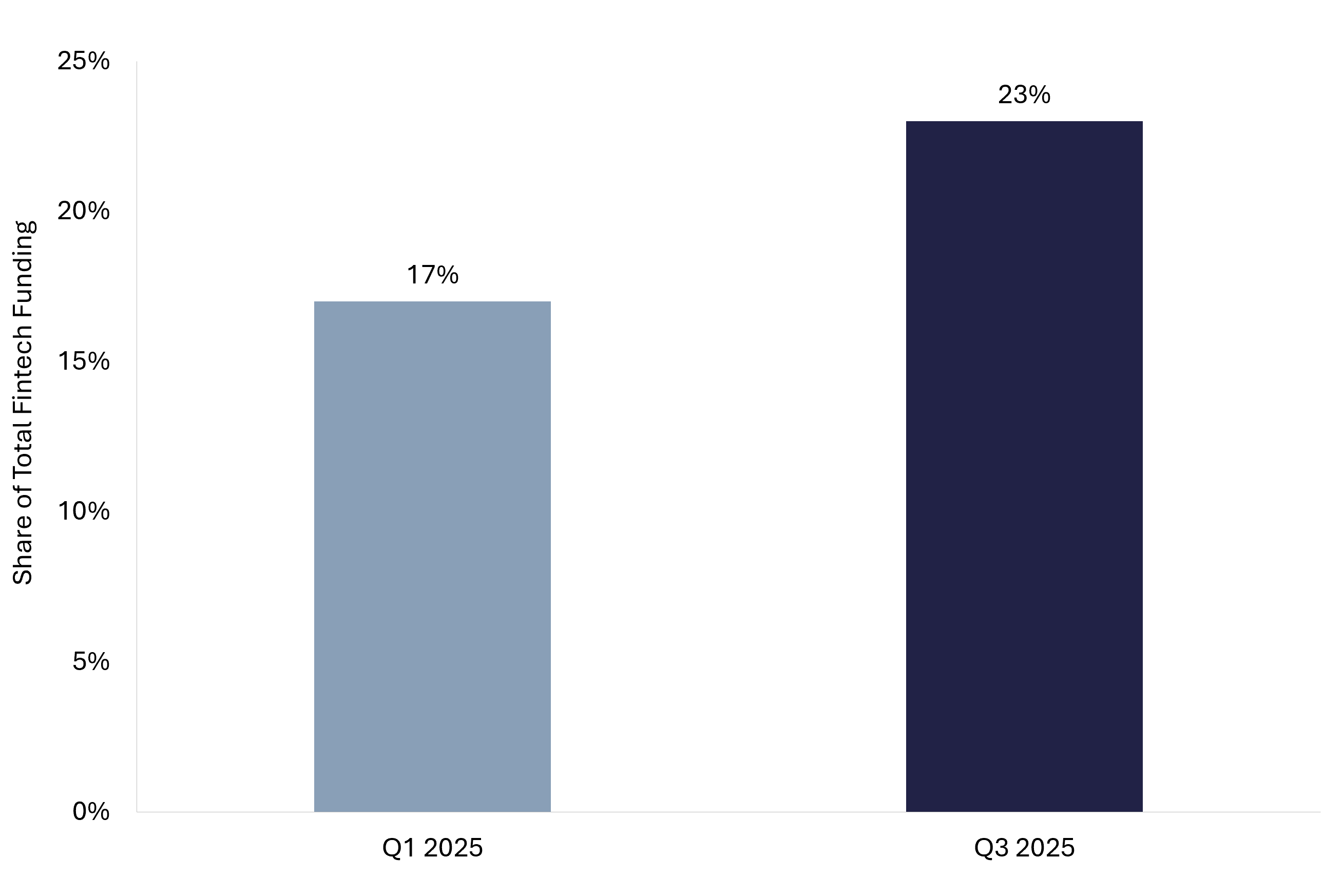

Artificial intelligence has moved from a talking point to a pricing factor in fintech deals. The clearest evidence is in the funding data: AI-enabled fintechs captured 23 percent of all fintech funding in the third quarter of 2025, the highest share in nearly two years, and five of the ten largest fintech equity deals that quarter went to companies deploying AI at their core. Median fintech valuations reached record highs during the year, driven in large part by AI premiums.

The momentum is strongest in a category that barely existed two years ago: agentic payments. These are systems where AI agents handle financial tasks end to end, from initiating a transaction to reconciling it. Early-stage companies building this infrastructure drew 80 percent more equity funding in 2025 than the year before. The shift is part of a broader move in fintech from front-end apps toward the foundation: data infrastructure, compliance automation, and payment rails.

The spending behind this trend is enormous. Worldwide AI spending is on track to reach $2.59 trillion in 2026, a 47 percent increase over the prior year, and purpose-built AI agent software alone is projected to nearly double, climbing from roughly $206 billion in 2026 toward $376 billion in 2027. When that much capital flows into a technology, financial institutions face a build-or-buy decision, and buying proven AI capability is frequently the faster route.

This is where AI reshapes valuations. A fintech that uses AI to genuinely improve its product, lower its cost to serve, or open a new revenue line is rewarded with a premium. The market increasingly distinguishes between businesses that have woven AI into their operations and those that simply describe themselves that way. For founders, that distinction is an opportunity. Demonstrable AI-driven efficiency, faster underwriting, fraud reduction, automated reconciliation, is a value driver that buyers will pay for.

It also changes what acquirers look for in diligence. Buyers want clean data, explainable models, and clear audit trails, because AI capability is only valuable if it can be integrated and trusted. A fintech that has built its AI on solid data foundations is more attractive and more defensible than one that bolted it on. We see this in practice: the businesses that present AI as a measurable part of their economics, rather than a marketing line, run more competitive sale processes.

It helps to be concrete about where the value sits. The fintechs drawing the strongest interest tend to apply AI to a specific, measurable problem: cutting fraud losses, approving good customers faster, automating support, or compressing the cost of compliance. A clear before-and-after, with numbers a buyer can verify, carries far more weight than a general claim of being AI-first. Founders who connect an AI capability directly to revenue or margin give acquirers a concrete reason to pay up.

Stablecoins and Tokenization: From Speculation to Settlement Infrastructure

One of the most consequential developments this year is the arrival of regulatory clarity for digital assets. In July 2025, the GENIUS Act was signed into law, creating the first federal framework for payment stablecoins in the United States. The law requires stablecoins to be backed one for one by US dollars or short-term Treasuries, mandates monthly public disclosure of reserves, and places issuers under federal or qualifying state supervision. By clarifying that compliant payment stablecoins are neither securities nor commodities, it removed a major source of uncertainty that had kept institutional capital on the sidelines.

The market response has been substantial. The total stablecoin market has expanded past $300 billion, with transfer volume reaching tens of trillions of dollars over the past year as stablecoins move from trading tool to settlement layer. Tokenized real-world assets, led by short-duration government debt, have climbed to fresh highs as traditional finance and blockchain infrastructure converge.

For M&A, this is a green light. Banks and large financial institutions are acquiring custody, settlement, and tokenization capabilities to prepare for tokenized deposits and real-world asset tokenization. The institutional momentum behind stablecoins, tokenization, and agentic payments is one of the defining themes investors are watching for 2026. Regulatory clarity tends to pull deal activity forward, because acquirers can finally underwrite these businesses with confidence about how they will be treated.

The opportunity for founders is real. A fintech with a money transmitter license, a banking charter, custody infrastructure, or proven compliance in the digital-asset space holds something buyers cannot easily build. Licensing and compliance take years and significant capital to obtain, which makes companies that already have them valuable acquisition targets, especially for institutions that want to enter the space quickly and cleanly.

This is a notable reframing of what compliance means. For years, regulatory overhead was seen mainly as a cost. In 2026, documented compliance, clean licensing, and a clear regulatory history are valuation multipliers, particularly in cross-border deals where buyers need assurance that a business can operate across jurisdictions without interruption. The companies that invested early in getting the regulatory foundation right are now positioned to command premium interest as digital-asset infrastructure becomes part of mainstream finance.

Regulatory clarity from the GENIUS Act has turned compliance and licensing from a cost center into a valuation multiplier for digital-asset fintechs.

Who’s Buying in 2026: Banks, Private Equity, and Strategics

Understanding the fintech M&A outlook 2026 means understanding the buyers, and the pool is unusually deep this year. Three groups are driving activity, each with a distinct motivation.

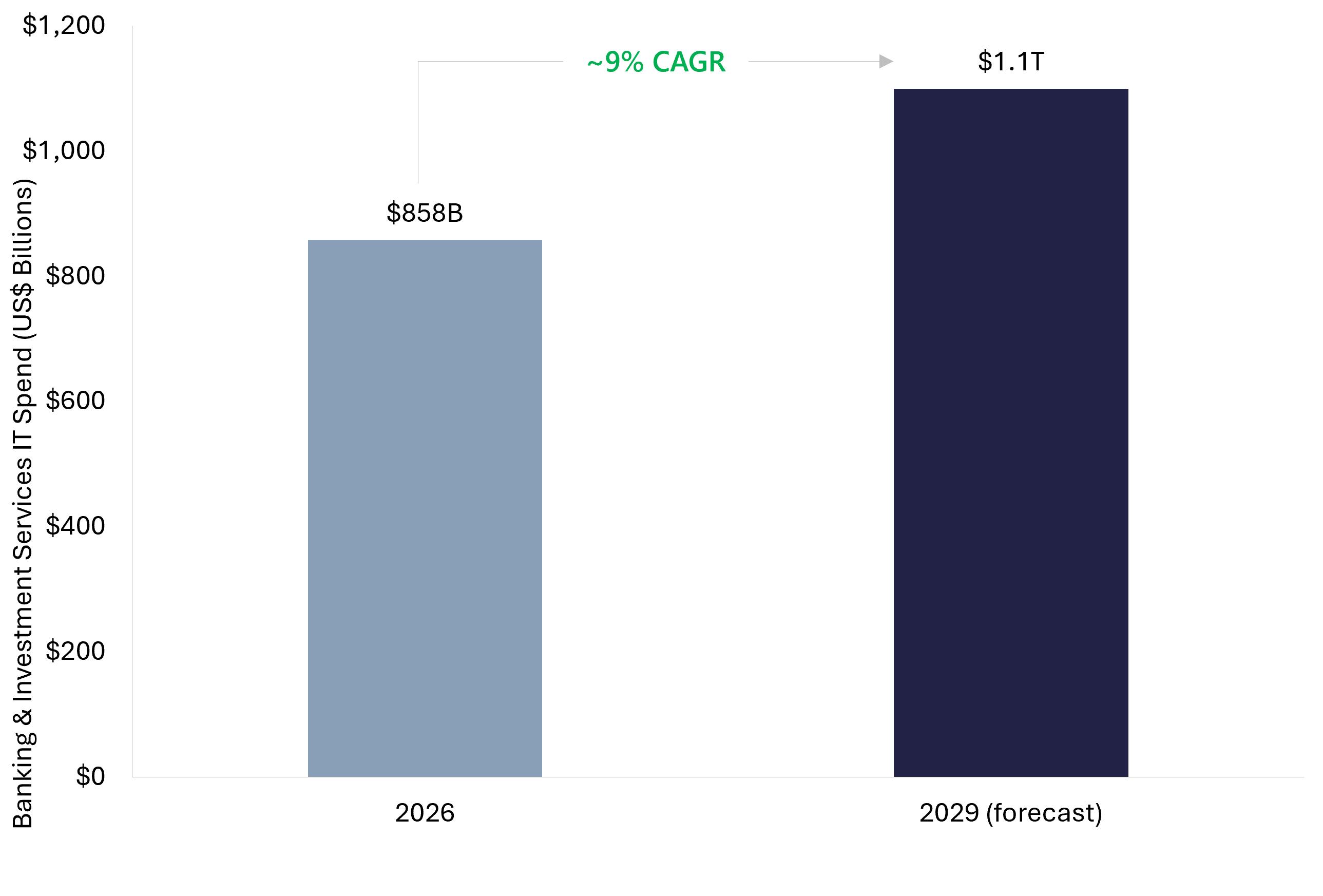

Banks and large financial institutions are using acquisitions as the fastest route to new capabilities. They are investing heavily in technology: banking and investment services IT spending is set to reach $857.5 billion in 2026 and grow at about 9 percent a year toward $1.1 trillion by 2029. When a bank needs payments technology, AI capability, or a digital platform to compete with fintech natives, buying a proven company is often faster and cheaper than building from scratch. Many banks are sitting on excess capital that makes well-targeted acquisitions attractive.

Private equity has become a dominant force in fintech M&A by transaction volume. Sponsors are running platform strategies: acquiring a foundation business and adding capabilities through follow-on deals. They evaluate fintech the way they evaluate any software investment, recurring revenue quality, margins, growth efficiency, with extra attention to regulatory positioning. With substantial dry powder to deploy and a constructive rate environment, PE firms are competing actively for quality assets, and they often pay attractive multiples because a larger portion of their offer can be funded with equity.

Strategic acquirers, including scaled fintechs themselves, round out the picture. Card networks, large processors, and category leaders are buying to enter new verticals, add adjacent products, or consolidate share. Payments, compliance infrastructure, digital identity, and embedded-finance capabilities sit high on their priority lists. Fintech-to-fintech acquisitions are an increasingly important part of the market as scaled platforms absorb smaller companies to expand their product range.

A common founder question is whether to pursue a merger or acquisition versus a partnership. Both have merit. A partnership preserves independence and can validate a relationship before a deal. An acquisition delivers liquidity, capital, and the resources of a larger organization to scale faster. The right answer depends on a founder’s goals, but in a market this active, many owners find that the competitive tension among multiple acquirer types produces terms strong enough to make a sale the clear choice.

The effect on consumer finance is positive on balance. As these buyers combine capabilities, customers gain access to faster payments, better digital tools, and more integrated financial services. That improvement in the end-customer experience is part of why acquirers are willing to pay for the right platforms, and it means the businesses solving real problems for consumers and companies are exactly the ones this deep buyer pool is competing to own.

What Fintech Companies Are Worth in 2026

Valuation is where the fintech M&A outlook 2026 gets specific, and the picture is encouraging for prepared businesses. Median fintech valuations reached record highs in 2025, supported by AI premiums and a reopened exit window. Disclosed fintech exit value of $67.6 billion, the strongest outside of 2021, tells you that buyers are not just looking, they are closing at strong prices.

The most important thing to understand is that fintech valuation is not a single number. It varies widely by subsector, business model, and the quality of the revenue. Payments and transfer businesses, which attract the most M&A activity, are valued on the predictability and scalability of transaction-based revenue; the Worldpay transaction’s roughly 8.5 times EBITDA gives a useful reference point for a scaled, profitable payments platform. Wealthtech and regtech businesses, with recurring fees and sticky client relationships, tend to command strong multiples; wealthtech funding nearly doubled in 2025 as investors backed mature, AI-augmented platforms. Lending businesses, which carry balance-sheet and credit risk, typically sit at the lower end of the range. Our breakdown of how to value a fintech business covers these subsector benchmarks in detail.

What drives a premium within any subsector? A few factors come up again and again. Recurring, high-retention revenue is the foundation. The Rule of 40, revenue growth plus profit margin reaching at least 40 percent, is one of the strongest predictors of a premium valuation. Healthy unit economics, a sensible ratio of customer lifetime value to acquisition cost, and clean margins signal a business that can scale profitably. Regulatory licenses and documented compliance add real value because they are expensive and slow to replicate. And reduced founder dependency, a business that runs on systems and a team rather than one person, gives buyers confidence that value will survive the transition.

The shift toward profitability is the throughline. In the previous cycle, growth alone could justify a high multiple. In 2026, the market rewards companies that pair growth with demonstrated cash generation. Many fintechs once valued purely on revenue are now assessed on EBITDA as their growth matures, and the businesses that have built real profitability are being rewarded for it.

This creates a healthy spread of outcomes. Profitable, well-documented businesses are seeing competitive interest and firm pricing, while companies that grew quickly without a path to profit are taking longer to clear. For a founder, the implication is practical: the months spent tightening margins and cleaning up reporting tend to pay back several times over in the final number. Value in this market follows evidence, and evidence is something an owner can build.

For founders, this is the most actionable part of the outlook. The factors that drive a premium are largely within your control, and most can be strengthened in the 12 to 24 months before a sale. A business that understands its numbers, knows its subsector benchmarks, and presents a clean, well-documented story will capture the upper end of its range. That preparation is the single biggest lever on outcome, and it is exactly the work an experienced advisor does alongside a founder.

In 2026, the market rewards fintechs that pair growth with profitability, clean compliance, and reduced founder dependency.

A Global Market: Regional Hotspots in 2026

Fintech M&A in 2026 is genuinely global, with strong activity across every major region. The Americas led fintech investment in 2025 with $66.5 billion, followed by EMEA at $29.2 billion and Asia-Pacific at $9.3 billion. Each region offers a distinct set of opportunities for buyers and sellers.

.png)

In the United States, a more accommodating regulatory environment and a strong dollar have encouraged dealmaking, and the Americas now account for roughly half of global financial-services deal value. The reopening IPO market and active strategic and private equity buyers make it one of the most liquid markets for fintech exits.

Europe is entering a multiyear consolidation phase as financial institutions pursue scale and modern technology. Regulatory frameworks such as MiCA have given the region clearer rules for digital assets, and embedded finance is growing at double-digit rates, which keeps a steady flow of acquisition targets in payments, lending infrastructure, and compliance technology. For founders of European fintechs, the combination of domestic consolidation and cross-border interest from US and global acquirers creates real optionality.

Asia-Pacific offers a different profile. While overall investment was more measured in 2025, specific markets show strong appetite, and the region’s scale and digital adoption make it a long-term growth story. Markets across Latin America, Southeast Asia, and Africa continue to attract acquirers buying local payment rails and compliance infrastructure to serve fast-growing populations. Emerging markets are where a great deal of the cross-border payments opportunity sits, and companies with strong local positions in these corridors are attractive to global players building out their reach.

Cross-border deals do carry added complexity, including differences in regulation, currency, and business culture. That is precisely why preparation and advisory expertise matter. A fintech that can show it operates cleanly across jurisdictions, with the licenses and compliance to match, removes friction for an international buyer and commands a stronger position. The businesses that get this right turn cross-border complexity into a competitive advantage, because they can serve markets that less-prepared competitors cannot.

Positioning Your Fintech for a Strong 2026 Outcome

A strong fintech M&A outlook 2026 rewards founders who prepare, and the good news is that preparation is largely within reach. The businesses capturing the best outcomes this year tend to do the same handful of things well.

Start with clean, audit-ready financials. Buyers move faster and renegotiate less when the numbers are clear and verifiable. FE International’s in-house audit preparation reduces the time buyers spend on diligence by around 28 percent compared with the industry average, which keeps deals on track and protects value. Tighten the operational story next: reduce founder dependency, document key processes, and make sure the team and systems can run the business through a transition.

Get the compliance and risk foundation right. In fintech, regulatory licenses, data privacy controls, and a clean compliance history are not just risk management, they are value drivers. Strong data privacy practices and documented controls reassure buyers and remove diligence friction, especially in cross-border deals. Acquirers and sponsor banks are paying closer attention to anti-money-laundering and sanctions controls, so a business with real-time monitoring and clean procedures presents far better. Addressing these areas early turns potential diligence obstacles into selling points.

Understand the deal structures common in this market. Many fintech transactions in 2026 include a mix of cash, seller notes, and earn-outs rather than all cash at close, which lets buyers and sellers bridge expectations and share in future upside. Knowing how these structures work, and how they affect taxes and net proceeds, helps founders evaluate offers on their true value rather than the headline number. Tax treatment can meaningfully change what a deal is worth, so it is worth modeling early with the right advisors. Financing is rarely the constraint it once was: with active private equity, well-capitalized banks, and strategic buyers competing, qualified acquirers have the capital to move.

A pre-sale checklist for fintech founders

If you are planning toward a sale in the next 12 to 24 months, a short checklist helps focus the work that moves valuation the most.

- Financials: keep clean, audit-ready accounts with clear revenue recognition, and separate one-time items from recurring revenue so buyers can see the real run-rate.

- Compliance and licensing: document every license, registration, and control, and keep anti-money-laundering, sanctions, and data privacy procedures current and evidenced.

- Revenue quality: show retention, cohort behavior, and the share of revenue that is recurring, because durability is what buyers underwrite.

- Founder dependency: build a team and systems that can run the business without you, and document the processes that currently live in your head.

- AI and data: if AI is part of the product, be ready to show clean data, explainable models, and the measurable impact on cost or revenue.

- Deal readiness: organize a data room early, model the tax impact of likely deal structures, and know your subsector benchmarks before offers arrive.

Working through this list with an experienced advisor well before a process begins is the surest way to reach the top of your valuation range.

This is where the right partner makes the difference. FE International runs confidential, competitive sale processes for technology businesses, with dedicated fintech expertise and a track record of more than 1,500 completed transactions, $50 billion-plus in deal value, and a 94.1 percent success rate. The team handles valuation, buyer outreach to a network of more than 80,000 vetted investors, negotiation, legal documentation, and post-close transition, so founders can keep running the business during the process. You can learn more on the FE International fintech advisory page.

For businesses valued under $1 million, the FE International M&A Platform offers a streamlined route to the same buyer pool, covering valuation, listing creation, buyer discovery, outreach, and deal management. Larger businesses in the $1 million to $100 million-plus range are a fit for the full-service advisory practice. Either way, the path to a premium outcome runs through preparation, and the time to start is before you plan to sell.

The Bottom Line on the 2026 Fintech M&A Outlook

The fintech M&A outlook 2026 comes down to a simple idea: capital is back, buyers are active, and quality is rewarded. Embedded finance is becoming a trillion-dollar engine, payments are consolidating into scaled platforms, AI is widening the gap between good and great businesses, and regulatory clarity has opened the door for digital-asset deals. Global fintech investment of $116 billion, exit value of $67.6 billion, and a 15 percent rise in financial services M&A all point to a market that favors prepared founders and well-positioned buyers.

For owners, the opportunity is clear. The factors that drive a premium, durable revenue, clean compliance, profitability, and reduced founder dependency, are largely within your control, and the buyer pool competing for those businesses is as deep as it has been in years.

If you are considering an exit or simply want to understand what your fintech business is worth, the best next step is a free, confidential valuation. FE International offers data-backed valuations drawn from more than 1,500 completed transactions, with dedicated fintech expertise and a 94.1 percent success rate. For businesses under $1 million, the FE International M&A Platform provides a streamlined path to the same pool of vetted buyers. The window is open, and the advantage goes to those who prepare.